Indian Economy

India’s New GDP Series With Base Year 2022-23

For Prelims: Gross Domestic Product, Gross Fixed Capital Formation, Private Final Consumption Expenditure, National Statistical Office, System of National Accounts 2008, Fiscal deficit

For Mains: Base Year Revision and Its Significance in National Income Accounting, Fiscal Consolidation and Nominal GDP Dynamics, Measuring Informal, Gig and Digital Economy

Source:IE

Why in News?

The Ministry of Statistics and Programme Implementation (MoSPI) released the New Series of Annual and Quarterly National Accounts Estimates with base year 2022–23 replacing the earlier 2011-12, marking a major update in the way the Gross Domestic Product (GDP) is measured.

Summary

- India has shifted the GDP base year to 2022–23, integrating improved data sources and refined methods such as double deflation and the SUT framework. Real GDP is projected at 7.6% in FY 2025–26, reflecting sustained growth and better sectoral coverage.

- The revised series lowers nominal GDP by 3–4%, tightening fiscal deficit and debt-to-GDP targets and making the $4-trillion goal more growth- and exchange-rate sensitive, while highlighting the need for reforms like PPI introduction and WPI revision.

What are the Key Highlights of the New GDP Series (Base Year 2022–23)?

- Real GDP Growth: Estimated to grow by 7.6% in Financial Year 2025-26 (revised upward from the 2011-12 base estimates).

- The economy showed sustained performance with 7.2% and 7.1% growth in Financial Years 2023-24 and 2024-25, respectively.

- Nominal GDP Growth: Witnessed a growth of 8.6% in Financial Year 2025-26.

- Nominal GDP previously registered at 11.0% and 9.7% growth rates during Financial Years 2023-24 and 2024-25.

- Quarterly Performance Drivers: The overall economic performance in Financial Year 2025-26 is primarily driven by robust real growth in the Second Quarter (8.4%) and Third Quarter (7.8%).

- Manufacturing Sector: Emerged as the major driver contributing to economic resilience for three consecutive financial years after rebasing, achieving double-digit growth rates in Financial Years 2023-24 and 2025-26.

- Secondary and Tertiary Sectors: Significantly boosted the economy by registering growth rates above 9.0% in the Financial Year 2025-26.

- Specific Services Sub-Sector: The ‘Trade, Repair, Hotels, Transport, Communication and Services related to Broadcasting, Storage’ sector attained a notable growth rate of 10.1% at constant prices in Financial Year 2025-26.

- Consumption and Investment: On the demand side, both Private Final Consumption Expenditure and Gross Fixed Capital Formation exhibited growth rates exceeding 7.0% in Financial Year 2025-26.

Why was the GDP Base Year Revised to 2022-23?

- Reflect a “Normal” Post-Pandemic Year: The year 2022–23 was chosen because it represents the most recent normal year after the disruptions caused by Covid-19.

- The years 2019–20 and 2020–21 were heavily distorted due to lockdowns, supply chain disruptions, and abnormal consumption and production patterns.

- Using 2022–23 as the base ensures that growth comparisons are anchored in a stable economic environment.

- Sectoral Coverage: Over the past decade, India’s economy has changed significantly.

- Renewable energy has expanded, digital and platform-based services have grown rapidly, the number of hired domestic workers has increased, and the gig economy has become more prominent.

- Consumption and investment patterns have evolved, while greater use of technology has boosted productivity across sectors.

- Rebasing allows GDP estimates to better capture the contribution of these emerging sectors and shifts in relative prices.

- Renewable energy has expanded, digital and platform-based services have grown rapidly, the number of hired domestic workers has increased, and the gig economy has become more prominent.

- Improved and High-Frequency Data Sources: The revised series incorporates several new and richer data sources, reducing reliance on proxies and outdated benchmarks.

- Earlier, household sector estimates were largely based on proxy indicators and growth rates between benchmark surveys.

- In the revised series, actual levels are derived from regular annual surveys such as Annual Survey of Unincorporated Sector Enterprises (ASUSE) and Periodic Labour Force Survey (PLFS) allowing for more accurate and timely measurement of the sector’s performance.

- Wider use of GST data for manufacturing and services, including state-level allocation and quarterly estimates.

- Data from the e-Vahan portal is used to estimate Private Final Consumption Expenditure (PFCE) on road transport services, improving the measurement of household consumption.

- Public Financial Management System (PFMS) data is used to compile and distribute central government accounts across states, allowing actual expenditure figures to be used at the First Revised Estimates stage instead of relying on Revised Estimates.

- Updated sector-specific studies in agriculture, fisheries, dairy, and transport. These additions improve granularity, timeliness, and reliability.

- Earlier, household sector estimates were largely based on proxy indicators and growth rates between benchmark surveys.

- Strengthen Methodological Rigor: The new base year accompanies important methodological upgrades:

- Refined Deflation Techniques: Double deflation (separate adjustment of output and input prices) is now applied in manufacturing and agriculture, while single extrapolation (estimating growth using a single output indicator) is used in other sectors.

- Single deflation has been discontinued. Deflators are applied at a more granular level, with over 260 item-level CPI indices incorporated.

- Supply and Use Table (SUT) Framework: Following System of National Accounts 2008 (SNA 2008) guidelines, the new GDP series systematically integrates the SUT framework and applies the product-balancing principle (total supply equals total use).

- This reduces statistical discrepancies and ensures more consistent and reliable GDP estimates.

- Segregation of Multi-Activity Corporations: Value added of multi-activity corporations is now distributed across activities using detailed corporate filings.

- Improved Estimation of PFCE: Estimation of Private Final Consumption Expenditure (PFCE) has also been strengthened through a mixed approach that combines household survey data, administrative records, the commodity flow method, and the updated Classification of Individual Consumption According to Purpose (COICOP) 2018.

- Refined Deflation Techniques: Double deflation (separate adjustment of output and input prices) is now applied in manufacturing and agriculture, while single extrapolation (estimating growth using a single output indicator) is used in other sectors.

- Strengthened GSDP Estimation: The revision of the GDP base year to 2022–23 also strengthens GSDP estimation.

- The National Statistical Office (NSO) under MoSPI ensures states follow uniform national accounting standards.

- With the new base, states will shift toward greater direct estimation, reduce reliance on fixed ratios and proxies, and better use state-level data, improving accuracy and comparability across states.

What are the Implications of the New GDP Series (Base Year 2022–23)?

- Contraction in Nominal GDP: The new statistical framework has reduced India's nominal GDP by roughly 3% to 4% for the 2025–26 financial year and the preceding three years.

- Pressure on Fiscal Deficit Targets: The fiscal deficit is calculated as a percentage of nominal GDP, a smaller nominal GDP mathematically inflates the deficit ratio for past and present years.

- The 2025–26 fiscal deficit target was initially set at 4.4% based on the old series. Applying the new, lowered nominal GDP pushes this ratio up to 4.5%.

- To achieve the targeted 4.3% fiscal deficit for the 2026-27 financial year, the economy will now require a massive nominal growth rate of 13% to 14%.

- This is notably higher than the 10% assumption outlined in the Union Budget 2026–27, indicating the government may need to aggressively recalibrate its borrowing strategies.

- Rising Debt-to-GDP Ratios: Reduced size of the economy negatively impacts the national debt-to-GDP ratio.

- The Centre’s debt ratio is estimated to rise from 56.2% to 58.1% for 2025–26 under the new series.

- Current calculations suggest that even if nominal growth successfully hits 10% in 2026–27, the ratio will hover around 57.5%, missing the government's target of 55.6%.

- Hurdles for the USD 4-Trillion Economy Goal: In 2025–26, India’s GDP stood at about USD 3.8 trillion.

- Crossing the USD 4-trillion mark in 2026–27 is still possible, but it leaves little room for error and requires at least 10% nominal growth.

- The target is also highly sensitive to the exchange rate, as any further rupee depreciation would make achieving it more difficult despite strong domestic growth.

- Sectoral Realignments: The agricultural sector is now estimated to be about 5% larger due to better capture of high-value crops and lower input costs, including increased use of solar power under schemes like PM KUSUM.

What Measures are Needed to Further Advance India’s Economic Measurement Framework?

- Introduce a Producer Price Index (PPI): India currently relies heavily on the Consumer Price Index (CPI) and Wholesale Price Index (WPI).

- As recommended by the Working Group chaired by Prof. B.N. Goldar (2014), introducing PPI will provide a much more accurate measure of the average change in selling prices received by domestic producers for their output, aligning India with global standards.

- Expedite the WPI Base Revision: While the CPI and IIP base years are being updated, the WPI base year revision must be completed swiftly to ensure that the deflators used across all sectors represent current market realities.

- Global Alignment: The UN Statistical Division is transitioning to SNA 2025 (expected to be adopted globally by 2029–30).

- India must proactively build the data infrastructure to adopt SNA 2025, which includes specialized guidelines for measuring the digital economy, crypto assets, and environmental/green accounting.

- Mitigating Large Firm Bias: Heavy reliance on Ministry of Corporate Affairs data may overstate large firms’ performance while underestimating MSMEs that do not file timely returns.

- Improved methods are needed to better capture the value added by smaller enterprises.

Glossary of Economic Terms

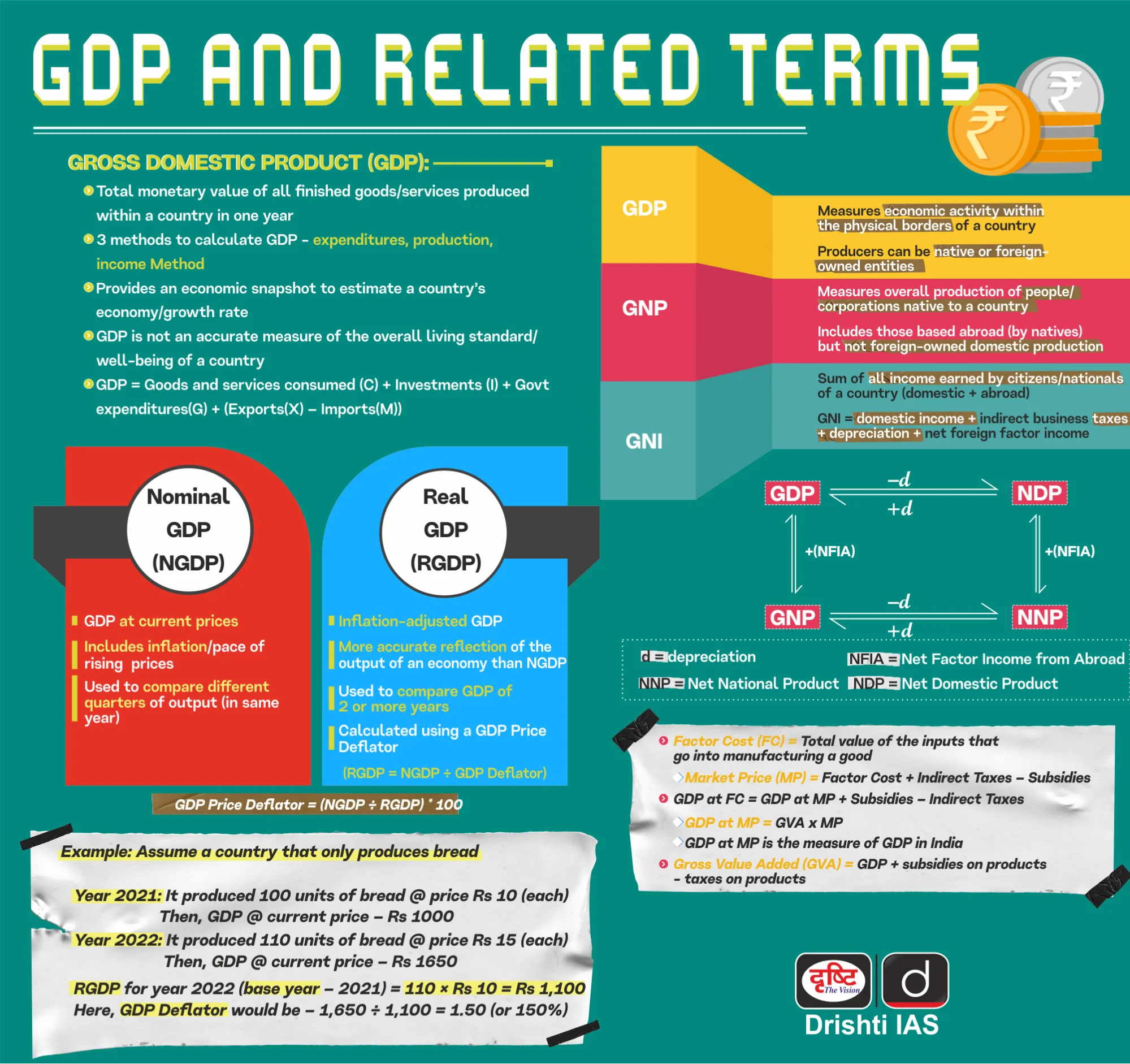

- GDP: It is the value of final goods and services produced within a country in an accounting period.

- By tracking changes in GDP over time, one can assess whether an economy is expanding or contracting and draw broad inferences about improvements in living standards.

- India compiles GDP in line with the System of National Accounts (SNA 2008) and plans to align with SNA 2025 in the next base year revision.

- As a subscriber to the IMF’s Special Data Dissemination Standard (SDDS), India follows global standards of statistical quality and transparency, and the revised GDP series remains internationally consistent.

- Quarterly GDP Estimates: National Statistical Office (NSO) & MoSPI calculate the quarterly GDP estimates using Benchmark-Indicator- a standard method used worldwide following the System of National Accounts (SNA) 2008 and IMF’s Quarterly National Accounts Manual 2017.

- The method works as follows:

- Annual GDP estimates act as a reference point/ benchmark.

- High-frequency data, like monthly or quarterly indicators, are applied to these benchmark estimates to estimate quarterly GDP.

- The method works as follows:

- Base Year: The base year, as defined in National Accounts Statistics, is the reference year whose prices are used to calculate real GDP growth and measure changes in economic performance over time.

- Rebasing: It is the process of updating the base year using improved data to reflect the current structure of the economy.

- The new base year becomes the reference point for estimating GDP and key indicators like CPI and IIP.

- GSDP: It is the value of all the goods and services produced within the boundaries of the State during a year.

- The NSO under MoSPI issues guidelines and provides technical support for estimating GSDP, while the Directorates of Economics and Statistics in each State and UT compile GSDP using state-level data drawn largely from common sources.

- COICOP: It is the United Nations-endorsed international reference classification of household expenditure.

- Supply and Use Tables (SUTs): The SUTs framework tracks how goods and services enter the economy through production or imports and how they are used for consumption, investment, or exports.

- By linking total supply with total use for each product, the SUT framework balances production, income, and expenditure approaches to GDP.

Conclusion

Real GDP growth of 7.6% in FY 2025–26 reflects strong economic momentum toward the vision of Viksit Bharat. The shift to the 2022–23 base year modernizes GDP measurement with better data and methods. Together, these reforms strengthen accuracy, transparency, and global credibility of India’s statistics.

|

Drishti Mains Question: Q. The revision of GDP base year is a technical exercise with significant fiscal consequences. Discuss in the context of India’s 2022–23 rebasing. |

Frequently Asked Questions (FAQs)

1. Why was the GDP base year revised to 2022–23?

To reflect a post-pandemic normal year, capture structural economic changes, integrate improved data sources, and align with global statistical standards under SNA 2008.

2. How does a lower nominal GDP affect fiscal deficit targets?

Since fiscal deficit is measured as a percentage of GDP, a lower nominal GDP mechanically increases the deficit ratio, tightening fiscal consolidation targets.

3. What is the significance of the Supply and Use Table (SUT) framework?

SUT ensures total supply equals total use, reconciling production and expenditure estimates and reducing statistical discrepancies in GDP.

4. What is Double Deflation and why is it important?

Double Deflation adjusts output and input prices separately, providing more accurate real value-added estimates, especially in manufacturing and agriculture.

5. How does the new GDP series impact India’s USD 4-trillion goal?

With GDP at $3.8 trillion in 2025–26, crossing USD 4 trillion is achievable but highly dependent on nominal growth and exchange rate stability.

UPSC Civil Services Examination, Previous Year Questions (PYQs)

Prelims

Q1. With reference to Indian economy, consider the following statements: (2015)

- The rate of growth of Real Gross Domestic Product has steadily increased in the last decade.

- The Gross Domestic Product at market prices (in rupees) has steadily increased in the last decade.

Which of the statements given above is/are correct?

(a) 1 only

(b) 2 only

(c) Both 1 and 2

(d) Neither 1 nor 2

Ans: (b)

Q2. A decrease in tax to GDP ratio of a country indicates which of the following? (2015)

- Slowing economic growth rate

- Less equitable distribution of national income

Select the correct answer using the code given below:

(a) 1 only

(b) 2 only

(c) Both 1 and 2

(d) Neither 1 nor 2

Ans: (a)

Mains

Q1. Define potential GDP and explain its determinants. What are the factors that have been inhibiting India from realizing its potential GDP? (2020)

Q2. Explain the difference between computing methodology of India’s Gross Domestic Product (GDP) before the year 2015 and after the year 2015. (2021)

Indian Polity

16th Finance Commission on Centre-State Fiscal Relations

For Prelims: 16th Finance Commission, Cess, Surcharge, State Finance Commission, Off-budget Borrowings, Article 279, Revenue Deficit Grant, Article 275, Inter-State Council, JAM Trinity.

For Mains: Key recommendations of the 16th Finance Commission, Key issues with the 16th Finance Commission recommendations and steps needed to bolster fiscal federalism in India.

Why in News?

The 16th Finance Commission has retained the States' share of tax devolution at 41%, imparting it a "semi-permanence," while introducing significant changes to the horizontal distribution formula and proposing a 'grand bargain' to merge cesses and surcharges into the divisible pool.

Summary

- The 16th Finance Commission retained 41% tax devolution while shifting toward performance-based horizontal distribution.

- Its proposals on cesses, fiscal discipline, and grant rationalisation have sparked debate over equity and state autonomy.

- The recommendations underscore evolving tensions between fiscal consolidation and cooperative federalism in India.

What are the Key Recommendations of the 16th Finance Commission (2026–31)?

- Vertical Devolution and a 'Grand Bargain': The Commission retained States' share in the divisible pool at 41%, unchanged from the 15th Finance Commission.

- To address the states’ concern over fiscal space eroded by rising cesses and surcharges (which are outside the divisible pool), the 16th FC proposed a 'grand bargain', i.e., states accept a smaller share of a larger divisible pool if the Centre merges most levies into shareable taxes.

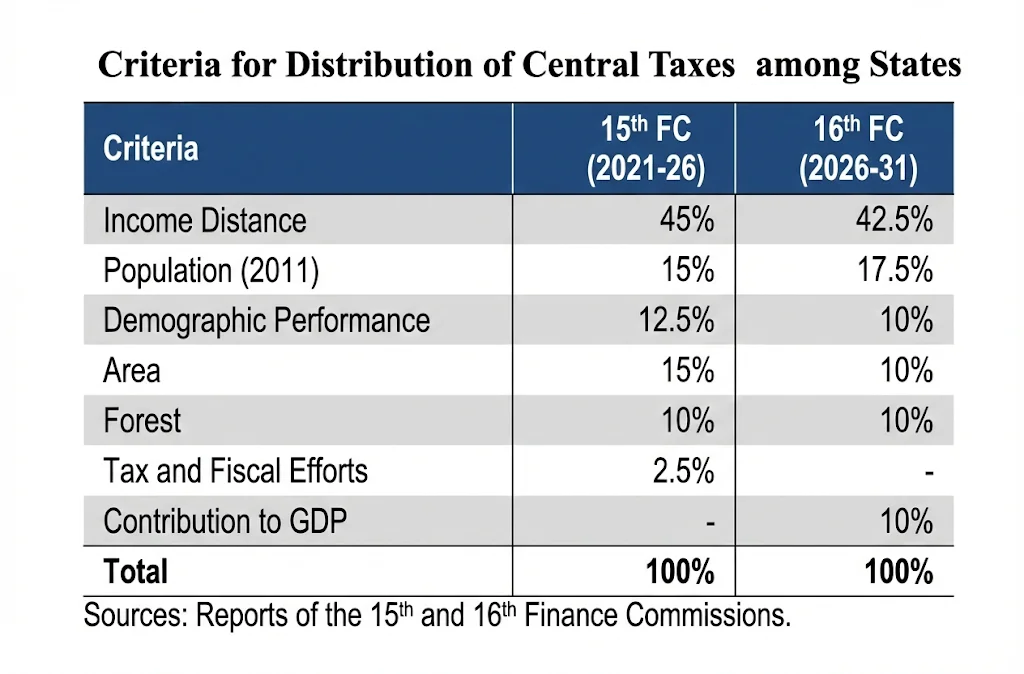

- Horizontal Devolution: The Commission introduced a major shift toward rewarding economic performance with a revised formula:

- Income Distance (42.5%): Based on the gap from the average of the top three states, ensuring equity.

- Population (2011 Census) (17.5%): Reflects expenditure needs.

- Demographic Performance (10%): Rewards lower population growth (1971–2011).

- Forest & Ecology (10%): Now includes open forests, not just dense forests.

- Area (10%): Remains unchanged at 10% (as per 15th FC).

- Contribution to GDP (10%): A new criterion measured by share in all-State GSDP (using its square root to moderate impact), replacing the tax effort/fiscal discipline criterion.

- Grants-in-Aid (Rs 9.47 Lakh Crore):

- Local Bodies (Rs 8 Lakh Cr): Split into rural (Rs 4.4 Lakh Cr) and urban (Rs 3.6 Lakh Cr). Grants are subject to entry conditions (constitution of local bodies, audited accounts, and timely constitution of State Finance Commissions).

- New initiatives include an Urbanisation Premium Grant (Rs 10,000 Cr) for rural-urban transition and Special Infrastructure Grants (Rs 56,100 Cr) for wastewater management.

- Disaster Management (Rs 2.04 Lakh Cr): For State Disaster Relief and Management Funds, with cost-sharing of 90:10 for northeastern/Himalayan states and 75:25 for others.

- Local Bodies (Rs 8 Lakh Cr): Split into rural (Rs 4.4 Lakh Cr) and urban (Rs 3.6 Lakh Cr). Grants are subject to entry conditions (constitution of local bodies, audited accounts, and timely constitution of State Finance Commissions).

- Fiscal Roadmap and Reforms:

- Fiscal Deficit: Recommended Centre reduce the deficit to 3.5% of GDP by 2030–31; States to maintain 3% of GSDP.

- Off-Budget Borrowings: Recommended ending off-budget borrowings and including all such liabilities in fiscal deficit/debt calculations.

- Power Sector: Encouraged privatisation of DISCOMs.

- Subsidies: Recommended rationalisation of subsidies, especially unconditional cash transfers, noting they now account for 20.2% of total subsidy spending (up from 3% in 2018–19), partly enabled by the JAM trinity.

- Public Sector Enterprise (PSEs) Reforms: Recommended closure of 308 inactive State PSEs and a review mechanism for consistently loss-making enterprises.

- Transparency Measures: Recommended annual disclosure of CAG-certified data on net tax proceeds under Article 279 to clarify the size of the divisible pool.

- Article 279 of the Constitution defines "net proceeds" of a tax as gross revenue minus collection costs, with the CAG's certification of these proceeds being final.

What are the Key Issues with the 16th Finance Commission Recommendations?

- Status Quo vs. Growing Imbalances: The Commission retained states' share in the divisible pool at 41%, rejecting states' demand for an increase to ~50%. Critics argue this prioritizes the Centre's fiscal needs (defence, infrastructure) over states' requirements, limiting their untied revenue and failing to address growing vertical fiscal imbalances.

- Unchecked Cesses and Surcharges: The Commission failed to recommend curbs on non-shareable cesses and surcharges, which have grown significantly, effectively shrinking the shareable tax base. This practice is seen as undermining fiscal federalism by centralizing resources.

- Rewarding Contribution over Need: The introduction of a new 10% weight for 'contribution to GDP' (replacing the tax effort criterion) rewards industrialized states (e.g., Tamil Nadu, Karnataka, Maharashtra). This dilutes progressive redistribution by reducing the weight of income distance (from 45% to 42.5%) and area (from 15% to 10%), tilting the formula toward richer states amid widening regional disparities.

- Discontinuation of Revenue Deficit Grants: The elimination of revenue deficit grants has drawn sharp criticism, particularly from hill states, northeastern states, and others with structural deficits and geographical constraints.

- Conditional Fiscal Discipline: Recommendations capping state deficits at 3% of GSDP, ending off-budget borrowings, rationalizing subsidies, and pursuing DISCOM privatisation are seen as imposing stringent conditions that limit state flexibility.

- The Equity Gap: Major losing states compared to the 15th Finance Commission include Uttar Pradesh, Bihar, West Bengal, Madhya Pradesh, Odisha, and several northeastern states (Arunachal Pradesh, Meghalaya, Manipur, Nagaland, Tripura, Sikkim, and Goa). Gains by richer states have not been uniform.

- This fiscal contraction risks trapping populous northern and eastern states in a vicious cycle where they receive fewer resources precisely when they need the most investment, potentially widening India's regional economic divide.

- Missed Opportunity Under Article 275: The Commission could have mitigated these losses through Article 275 grants, which are designed for State-specific 'needs' (like health and education) separate from revenue deficits. By dropping all such grants, it missed a chance to balance efficiency with the equalisation objective for India's highly differentiated states.

What Steps can be Taken to Bolster Fiscal Federalism in India?

- Enhance Vertical Transfers: Increase states' share beyond 41% and cap cesses/surcharges (e.g., at 10% of gross tax revenue (GTR), (currently, nearly 20% of GTR)) through legislation, restoring predictability and expanding untied resources.

- Ensure Phased Transition: Provide a "Floor Guarantee" ensuring no state's absolute share drops below 15th Finance Commission levels during the shift toward performance-based transfers.

- Balance Equity with Efficiency: Retain progressive criteria (income distance, forest cover) while introducing elasticity-linked transfers rewarding revenue buoyancy and performance in social indicators/climate action.

- Empower Local Bodies: Strengthen PRIs/ULBs through matching grants for states implementing State Finance Commission (SFC) recommendations and grant genuine taxation powers (e.g., property taxes).

- Strengthen Federal Dialogue: Reactivate Inter-State Council (Article 263) meetings for "Real-time Federalism" to resolve fiscal disputes without litigation.

Conclusion

The 16th Finance Commission navigated a complex federal landscape by retaining the 41% vertical share and introducing efficiency incentives. However, its failure to curb cesses, discontinuation of revenue deficit grants, and tilt toward richer states have raised concerns about fiscal equity. Balancing performance with equalisation remains the core challenge for India's fiscal federalism.

|

Drishti Mains Question: Q. "Critically analyze the recommendations of the Sixteenth Finance Commission regarding vertical and horizontal devolution. How do they balance the dual objectives of equity and efficiency?" |

Frequently Asked Questions (FAQs)

1. What is the vertical devolution recommended by the 16th Finance Commission?

The 16th FC retained the States' share in the divisible pool of central taxes at 41% , unchanged from the 15th FC, imparting it a "semi-permanence."

2. What is the 'grand bargain' proposed by the 16th Finance Commission?

It proposed that States accept a smaller share of a larger divisible pool if the Centre merges a large part of the cesses and surcharges into the regular tax base, ensuring no revenue loss to either side.

3. What is the new criterion introduced in the horizontal devolution formula?

The Commission introduced a 10% weight for 'contribution to GDP' (measured by share in all-State GSDP), replacing the tax effort/fiscal discipline criterion, to reward economic performance.

UPSC Civil Services Examination, Previous Year Questions (PYQs)

Prelims

Q. Consider the following:

- Demographic performance

- Forest and ecology

- Governance reforms

- Stable government

- Tax and fiscal efforts

For the horizontal tax devolution, the Fifteenth Finance Commission used how many of the above as criteria other than population area and income distance (2023)

- Only two

- Only three

- Only four

- All five Ans: B

Q. With reference to the Fourteenth Finance Commission, which of the following statements is/ are correct? (2015)

- It has increased the share of States in the central divisible pool from 32 percent to 42 percent.

- It has made recommendations concerning sector-specific grants.

Select the correct answer using the code given below.

(a) 1 only

(b) 2 only

(c) Both 1 and 2

(d) Neither 1 nor 2

Ans: (a)

Mains

Q. How have the recommendations of the 14thFinance Commission of India enabled the states to improve their fiscal position?(2021).

Q. How is the Finance Commission of India constituted? What do you about the terms of reference of the recently constituted Finance Commission? Discuss.(2018)

Q. Discuss the recommendations of the 13th Finance Commission which have been a departure from the previous commissions for strengthening the local government finances.(2013)

Important Facts For Prelims

PSB Reforms under EASE 9.0

Why in News?

Under the EASE 9.0 reforms agenda, public sector banks (PSBs) will pursue important reforms to prepare PSBs to leverage technology and improve productivity and scale through new business models.

What Reforms will be Pursued under the EASE 9.0 Reforms Agenda?

- GCC Strategy and Leadership: Public sector banks will implement a global capability centre (GCC) strategy in FY 2026-27 and prepare a capacity-building roadmap. State Bank of India (SBI), which established the first GCC among state-run lenders earlier this year (in Karnataka), will take the lead.

- GCCs are offshore units of multinational corporations that perform strategic functions like IT, R&D, and business support.

- Technology Infrastructure Plans: Banks are expected to assess active-active data centre models for inclusion in their five-year business plans to ensure business continuity and resilience.

- Develop core AI stacks, including LLM (Large Language Model) licensing, GPU strategies, and private cloud model deployment.

- Build enterprise-wide consent management capabilities.

- Implement at-scale data tokenisation and anonymisation to enable continuity of data usage for business and strategic purposes.

- Collaborative Solutions: Banks will combine strengths to offer complete banking solutions, including blockchain technology, advanced risk assessment, and fraud detection models.

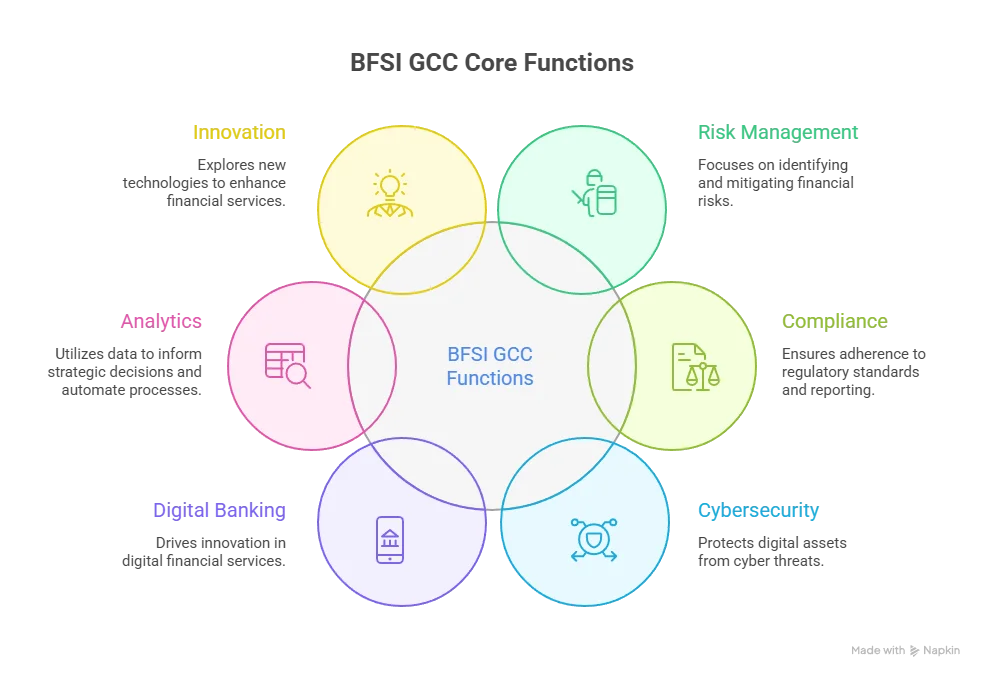

What are Banking, Financial Services, and Insurance (BFSI) GCC?

- About: A BFSI GCC is a 100% owned and operated subsidiary of a global BFSI institution in talent-rich locations like India, serving as strategic extensions that centralize high-value functions, drive innovation, and achieve operational efficiency.

- Unlike general GCCs, BFSI GCCs specifically serve the Banking, Financial Services, and Insurance sector in areas such as risk management, compliance, fintech, and cybersecurity.

- Strategic Evolution: GCCs have evolved significantly from initial cost arbitrage (achieving 50–60% savings compared to home markets) to advanced hubs for proprietary capabilities including artificial intelligence (AI), machine learning (ML), cybersecurity, regulatory technology (RegTech), data analytics, and core platform development.

- Core Functions in BFSI GCCs:

- India's Position in BFSI GCC Ecosystem: India's BFSI GCCs are projected to grow to USD 125 billion by 2032 (from USD 40-41 billion in 2023). Currently, 185-190 BFSI GCCs operate across India, employing approximately 540,000 professionals, representing 25% of all GCC employees in the country.

- Major hubs include Bengaluru (analytics and engineering), Hyderabad (fintech), Mumbai (financial services core), Pune, Chennai, and Gurugram/NCR.

- Examples of BFSI GCCs in India: JPMorgan Chase, HSBC, Wells Fargo, Citigroup, Standard Chartered, Deutsche Bank, Barclays, Bank of America, Goldman Sachs, and Morgan Stanley.

EASE 9.0 Reforms

- About: The EASE 9.0 reforms, launched in February 2026 by the Department of Financial Services, aim to transform PSBs into globally competitive institutions aligned with the national vision of Viksit Bharat @2047.

- It emphasizes technology-led modernization, resilience, and operational excellence through four foundational pillars abbreviated as R.I.S.E.

- Core Structure - Four Foundational Pillars (R.I.S.E.):

- Risk & Resilience: Strengthening financial and credit risk management, operational resilience, and frameworks for enterprise-wide risk oversight.

- Innovation: Driving deep integration of advanced technologies, including AI, generative AI (GenAI), machine learning (ML), cloud architectures, and microservices.

- Socio-economic Impact: Promoting inclusive banking, financial access for underserved segments (including gig and platform workers), and contributions to broader economic goals.

- Excellence: Enhancing operational efficiency, customer-centric processes, governance, and cost-effective next-generation operating models.

Frequently Asked Questions (FAQs)

1. What is EASE 9.0?

EASE 9.0 is a banking reform agenda launched in February 2026 by the Department of Financial Services (DFS) to modernize Public Sector Banks through technology integration and institutional strengthening.

2. What does the R.I.S.E. framework under EASE 9.0 stand for?

It stands for Risk & Resilience, Innovation, Socio-economic Impact, and Excellence, forming the four foundational pillars of banking reforms.

3. What is a BFSI Global Capability Centre (GCC)?

A BFSI GCC is a wholly owned subsidiary of a global financial institution that centralizes high-value functions like risk management, AI, cybersecurity, and regulatory compliance.

4. How significant is India in the global BFSI GCC ecosystem?

India hosts around 185–190 BFSI GCCs, employing about 540,000 professionals, and the sector is projected to reach USD 125 billion by 2032.

5. How does EASE 9.0 promote technological modernization?

It emphasizes AI stacks, LLM licensing, active-active data centres, blockchain integration, data tokenisation, and cloud architectures to enhance resilience and productivity.

UPSC Civil Services Examination, Previous Year Question (PYQ)

Q. With reference to the governance of public sector banking in India, consider the following statements: (2018)

- Capital infusion into public sector banks by the Government of India has steadily increased in the last decade.

- To put the public sector banks in order, the merger of associate banks with the parent State Bank of India has been affected.

Which of the statements given above is/are correct?

(a) 1 only

(b) 2 only

(c) Both 1 and 2

(d) Neither 1 nor 2

Ans: (b)

Rapid Fire

NITI Aayog-JICA Cooperation on SDGs

NITI Aayog and the Japan International Cooperation Agency (JICA) signed the Record of Discussions (RoD) for the "Project for Promotion of the Program for Japan-India Cooperative Actions Towards Sustainable Development Goals (SDGs) – Phase II".

- Objective and Scope: The project aims to strengthen policy frameworks and implementation systems across six key themes, i.e., Global Partnership, Health & Nutrition, Education, Agriculture & Water Resources, Financial Inclusion & Skill Development, and Basic Infrastructure.

- Key Focus Areas: It focuses on institutional capacity building, improved monitoring and evaluation, and effective localisation of SDGs in Aspirational Districts and Aspirational Blocks.

- Activities: Key activities include people-to-people exchanges, capacity-building programs, Japan–India knowledge forums, and identification and dissemination of Best Practices.

India-Japan Development Partnership

- Historic Scale of Assistance: Japan has been India's largest bilateral donor since 1958, with cumulative Official Development Assistance (ODA) exceeding Rs 4.4 lakh crore, supporting over 84 ongoing projects in sectors like transportation, energy, and water.

- Guiding Framework for the Decade: The India-Japan Joint Vision for the Next Decade (August 2025) outlines 8 strategic directions for cooperation, including enhanced economic ties, technology partnerships, and clean energy initiatives.

- Both countries set a new target of USD 68 billion in private investment from Japan to India over the next decade.

- Recent Financial Commitments: In March 2025, 6 loan agreements were signed under Japan's ODA, totalling Rs 11,181 crores to fund infrastructure and sustainable development projects.

- Strengthening Financial Stability: To enhance economic resilience, the Bilateral Swap Arrangement was renewed at USD 75 billion (effective February 2026).

| Read More: Revisiting India-Japan Relations |

Rapid Fire

Nucleic Acid Amplification Testing

The Supreme Court of India has sought comprehensive details regarding the cost, feasibility, and infrastructure required to implement Nucleic Acid Amplification Testing (NAT) in government hospitals, responding to a Public Interest Litigation (PIL) that advocates for the prevention of transfusion-transmitted infections.

- Constitutional Angle: The PIL, urges the Court to declare the "Right to Safe Blood" as an intrinsic facet of the Right to Life under Article 21 of the Indian Constitution.

- The petition seeks directions to make NAT mandatory across all Indian blood banks.

- This aims to accurately detect Transfusion Transmissible Infections (TTIs), including HIV, Hepatitis B (HBV), Hepatitis C (HCV), malaria, and syphilis, before the blood is transfused.

- Regulatory Framework: Currently, under the Drugs and Cosmetics Act of 1940, mandatory blood screening in India only requires serological testing (such as Enzyme-Linked Immunosorbent Assays).

- Nucleic Acid Testing is not legally mandatory across the country.

- The Thalassemia Crisis: The plea highlights the systemic failure to protect highly vulnerable patients, noting that India is considered the "Thalassemia capital of the world."

- Thalassemia is an inherited (genetic) blood disorder characterized by the body's inability to produce sufficient haemoglobin (the protein in red blood cells that carries oxygen).

- Thalassemia patients require life-saving blood transfusions every 15 to 20 days, making them highly susceptible to TTIs if blood is improperly screened.

- The petition highlighted preventable cases in Madhya Pradesh, Jharkhand, and Uttar Pradesh where children contracted HIV and Hepatitis due to unsafe blood transfusions.

- Thalassemia is an inherited (genetic) blood disorder characterized by the body's inability to produce sufficient haemoglobin (the protein in red blood cells that carries oxygen).

Nucleic Acid Amplification Testing (NAT)

- It is a highly sensitive molecular technique that screens blood donations by amplifying targeted regions of viral Ribonucleic Acid or Deoxyribonucleic Acid.

- Traditional serological tests must wait for the human body to produce an immune response (antibodies) before an infection can be detected.

- Nucleic Acid Testing directly detects the virus, drastically narrowing the "window period" (the time between initial infection and detectability) for Human Immunodeficiency Virus, Hepatitis B Virus, and Hepatitis C Virus.

- This advanced testing helps identify "false reactive" blood donations that standard serology methods incorrectly flag as infected.

- This ensures safe blood is not unnecessarily discarded and aids in accurate donor counselling.

| Read more: Bombay Blood Group |

Rapid Fire

Innovators Business Environment Index (IBEI) 2026

StartupBlink released the Innovators Business Environment Index (IBEI) 2026, which measures foundational business conditions like regulation, capital, and infrastructure using a 0–100 score.

Innovators Business Environment Index (IBEI)

- About: The IBEI evaluates national business environments based on their accessibility, predictability, and low-friction systems for innovators. It focuses on inputs and enabling conditions for starting and scaling businesses, differentiating itself from outcome-based metrics like startup success rates.

- Methodology and Indicators: The index aggregates scores from over 30 measurable indicators across key pillars:

- Regulation and Government: Ease of starting and operating a business, and regulatory friction.

- Access to Capital & Financial Infrastructure: Funding availability and credit conditions.

- Taxation: Incentives and tax conditions for businesses.

- Digital Infrastructure: Internet speed, freedom, and connectivity.

- Global Mobility & Openness: International accessibility, market perception, and governance stability.

- IBEI Rankings 2026: The United States ranked 1st with a perfect score of 100, while Singapore ranked 2nd and the United Kingdom ranked 3rd.

- India's Performance: India is ranked 54th globally with a score of 55.035. India is ranked ahead of China, which is placed 85th.

- The report identifies India's business environment as being marked by robust regional strengths, reliable access to capital, a large market size, and a competitive cost structure.

![]()

| Read More: Business Ready (B-READY) Report 2024 |

Rapid Fire

Meningococcal Bacterial Infection

The Meghalaya has issued a high-level health advisory following the death of two Agniveer trainees due to suspected meningococcal bacterial infection at the Assam Regimental Centre (ARC) in Shillong.

- Etiology: The disease is a severe, rapidly progressing infection caused by the bacterium Neisseria meningitidis.

- Clinical Manifestations: The meningococcal infection primarily leads to meningitis (inflammation of the brain and spinal cord lining) or meningococcemia (a life-threatening blood infection/sepsis).

- Transmission: Spreads through direct contact with nose/throat discharges from infected individuals.

- Risk Factors: More common in infants under 5, teenagers, young adults (16–23), and people in crowded settings like college dorms or military barracks.

- Treatment: Immediate treatment with antibiotics is crucial to reduce mortality, which is roughly 10%–15% even with care.

- The World Health Organization (WHO) recommended meningitis vaccine, Men5CV, is the first conjugate vaccine to protect against the five main causes of meningococcal meningitis.

| Read more: Nigeria Leads with New Meningitis Vaccine |