Indian Polity

16th Finance Commission on Centre-State Fiscal Relations

- 03 Mar 2026

- 12 min read

For Prelims: 16th Finance Commission, Cess, Surcharge, State Finance Commission, Off-budget Borrowings, Article 279, Revenue Deficit Grant, Article 275, Inter-State Council, JAM Trinity.

For Mains: Key recommendations of the 16th Finance Commission, Key issues with the 16th Finance Commission recommendations and steps needed to bolster fiscal federalism in India.

Why in News?

The 16th Finance Commission has retained the States' share of tax devolution at 41%, imparting it a "semi-permanence," while introducing significant changes to the horizontal distribution formula and proposing a 'grand bargain' to merge cesses and surcharges into the divisible pool.

Summary

- The 16th Finance Commission retained 41% tax devolution while shifting toward performance-based horizontal distribution.

- Its proposals on cesses, fiscal discipline, and grant rationalisation have sparked debate over equity and state autonomy.

- The recommendations underscore evolving tensions between fiscal consolidation and cooperative federalism in India.

What are the Key Recommendations of the 16th Finance Commission (2026–31)?

- Vertical Devolution and a 'Grand Bargain': The Commission retained States' share in the divisible pool at 41%, unchanged from the 15th Finance Commission.

- To address the states’ concern over fiscal space eroded by rising cesses and surcharges (which are outside the divisible pool), the 16th FC proposed a 'grand bargain', i.e., states accept a smaller share of a larger divisible pool if the Centre merges most levies into shareable taxes.

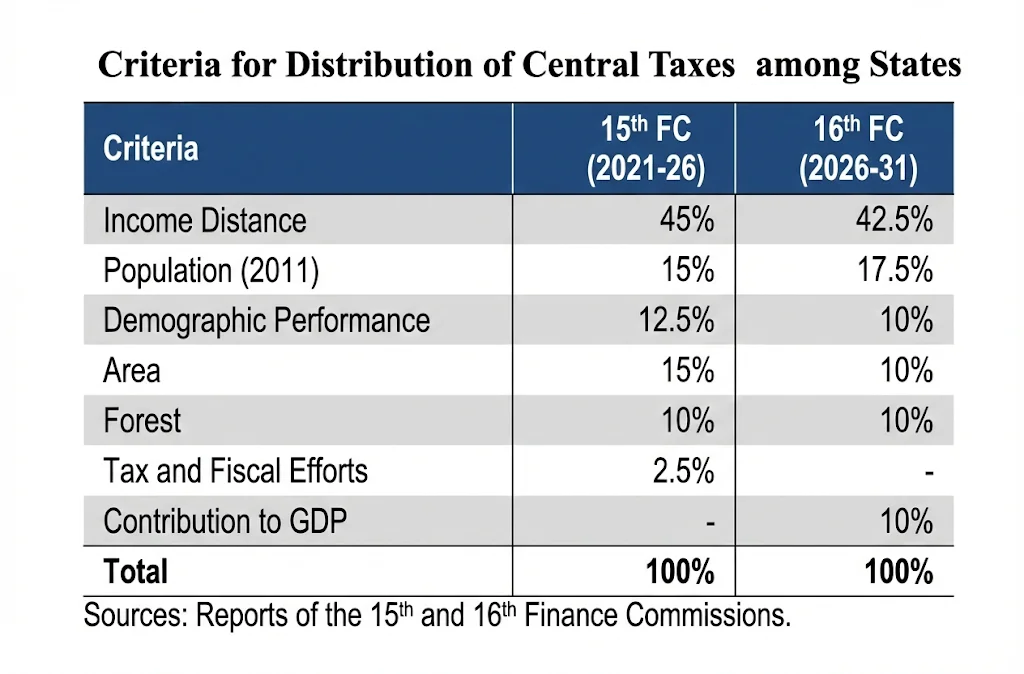

- Horizontal Devolution: The Commission introduced a major shift toward rewarding economic performance with a revised formula:

- Income Distance (42.5%): Based on the gap from the average of the top three states, ensuring equity.

- Population (2011 Census) (17.5%): Reflects expenditure needs.

- Demographic Performance (10%): Rewards lower population growth (1971–2011).

- Forest & Ecology (10%): Now includes open forests, not just dense forests.

- Area (10%): Remains unchanged at 10% (as per 15th FC).

- Contribution to GDP (10%): A new criterion measured by share in all-State GSDP (using its square root to moderate impact), replacing the tax effort/fiscal discipline criterion.

- Grants-in-Aid (Rs 9.47 Lakh Crore):

- Local Bodies (Rs 8 Lakh Cr): Split into rural (Rs 4.4 Lakh Cr) and urban (Rs 3.6 Lakh Cr). Grants are subject to entry conditions (constitution of local bodies, audited accounts, and timely constitution of State Finance Commissions).

- New initiatives include an Urbanisation Premium Grant (Rs 10,000 Cr) for rural-urban transition and Special Infrastructure Grants (Rs 56,100 Cr) for wastewater management.

- Disaster Management (Rs 2.04 Lakh Cr): For State Disaster Relief and Management Funds, with cost-sharing of 90:10 for northeastern/Himalayan states and 75:25 for others.

- Local Bodies (Rs 8 Lakh Cr): Split into rural (Rs 4.4 Lakh Cr) and urban (Rs 3.6 Lakh Cr). Grants are subject to entry conditions (constitution of local bodies, audited accounts, and timely constitution of State Finance Commissions).

- Fiscal Roadmap and Reforms:

- Fiscal Deficit: Recommended Centre reduce the deficit to 3.5% of GDP by 2030–31; States to maintain 3% of GSDP.

- Off-Budget Borrowings: Recommended ending off-budget borrowings and including all such liabilities in fiscal deficit/debt calculations.

- Power Sector: Encouraged privatisation of DISCOMs.

- Subsidies: Recommended rationalisation of subsidies, especially unconditional cash transfers, noting they now account for 20.2% of total subsidy spending (up from 3% in 2018–19), partly enabled by the JAM trinity.

- Public Sector Enterprise (PSEs) Reforms: Recommended closure of 308 inactive State PSEs and a review mechanism for consistently loss-making enterprises.

- Transparency Measures: Recommended annual disclosure of CAG-certified data on net tax proceeds under Article 279 to clarify the size of the divisible pool.

- Article 279 of the Constitution defines "net proceeds" of a tax as gross revenue minus collection costs, with the CAG's certification of these proceeds being final.

What are the Key Issues with the 16th Finance Commission Recommendations?

- Status Quo vs. Growing Imbalances: The Commission retained states' share in the divisible pool at 41%, rejecting states' demand for an increase to ~50%. Critics argue this prioritizes the Centre's fiscal needs (defence, infrastructure) over states' requirements, limiting their untied revenue and failing to address growing vertical fiscal imbalances.

- Unchecked Cesses and Surcharges: The Commission failed to recommend curbs on non-shareable cesses and surcharges, which have grown significantly, effectively shrinking the shareable tax base. This practice is seen as undermining fiscal federalism by centralizing resources.

- Rewarding Contribution over Need: The introduction of a new 10% weight for 'contribution to GDP' (replacing the tax effort criterion) rewards industrialized states (e.g., Tamil Nadu, Karnataka, Maharashtra). This dilutes progressive redistribution by reducing the weight of income distance (from 45% to 42.5%) and area (from 15% to 10%), tilting the formula toward richer states amid widening regional disparities.

- Discontinuation of Revenue Deficit Grants: The elimination of revenue deficit grants has drawn sharp criticism, particularly from hill states, northeastern states, and others with structural deficits and geographical constraints.

- Conditional Fiscal Discipline: Recommendations capping state deficits at 3% of GSDP, ending off-budget borrowings, rationalizing subsidies, and pursuing DISCOM privatisation are seen as imposing stringent conditions that limit state flexibility.

- The Equity Gap: Major losing states compared to the 15th Finance Commission include Uttar Pradesh, Bihar, West Bengal, Madhya Pradesh, Odisha, and several northeastern states (Arunachal Pradesh, Meghalaya, Manipur, Nagaland, Tripura, Sikkim, and Goa). Gains by richer states have not been uniform.

- This fiscal contraction risks trapping populous northern and eastern states in a vicious cycle where they receive fewer resources precisely when they need the most investment, potentially widening India's regional economic divide.

- Missed Opportunity Under Article 275: The Commission could have mitigated these losses through Article 275 grants, which are designed for State-specific 'needs' (like health and education) separate from revenue deficits. By dropping all such grants, it missed a chance to balance efficiency with the equalisation objective for India's highly differentiated states.

What Steps can be Taken to Bolster Fiscal Federalism in India?

- Enhance Vertical Transfers: Increase states' share beyond 41% and cap cesses/surcharges (e.g., at 10% of gross tax revenue (GTR), (currently, nearly 20% of GTR)) through legislation, restoring predictability and expanding untied resources.

- Ensure Phased Transition: Provide a "Floor Guarantee" ensuring no state's absolute share drops below 15th Finance Commission levels during the shift toward performance-based transfers.

- Balance Equity with Efficiency: Retain progressive criteria (income distance, forest cover) while introducing elasticity-linked transfers rewarding revenue buoyancy and performance in social indicators/climate action.

- Empower Local Bodies: Strengthen PRIs/ULBs through matching grants for states implementing State Finance Commission (SFC) recommendations and grant genuine taxation powers (e.g., property taxes).

- Strengthen Federal Dialogue: Reactivate Inter-State Council (Article 263) meetings for "Real-time Federalism" to resolve fiscal disputes without litigation.

Conclusion

The 16th Finance Commission navigated a complex federal landscape by retaining the 41% vertical share and introducing efficiency incentives. However, its failure to curb cesses, discontinuation of revenue deficit grants, and tilt toward richer states have raised concerns about fiscal equity. Balancing performance with equalisation remains the core challenge for India's fiscal federalism.

|

Drishti Mains Question: Q. "Critically analyze the recommendations of the Sixteenth Finance Commission regarding vertical and horizontal devolution. How do they balance the dual objectives of equity and efficiency?" |

Frequently Asked Questions (FAQs)

1. What is the vertical devolution recommended by the 16th Finance Commission?

The 16th FC retained the States' share in the divisible pool of central taxes at 41% , unchanged from the 15th FC, imparting it a "semi-permanence."

2. What is the 'grand bargain' proposed by the 16th Finance Commission?

It proposed that States accept a smaller share of a larger divisible pool if the Centre merges a large part of the cesses and surcharges into the regular tax base, ensuring no revenue loss to either side.

3. What is the new criterion introduced in the horizontal devolution formula?

The Commission introduced a 10% weight for 'contribution to GDP' (measured by share in all-State GSDP), replacing the tax effort/fiscal discipline criterion, to reward economic performance.

UPSC Civil Services Examination, Previous Year Questions (PYQs)

Prelims

Q. Consider the following:

- Demographic performance

- Forest and ecology

- Governance reforms

- Stable government

- Tax and fiscal efforts

For the horizontal tax devolution, the Fifteenth Finance Commission used how many of the above as criteria other than population area and income distance (2023)

- Only two

- Only three

- Only four

- All five Ans: B

Q. With reference to the Fourteenth Finance Commission, which of the following statements is/ are correct? (2015)

- It has increased the share of States in the central divisible pool from 32 percent to 42 percent.

- It has made recommendations concerning sector-specific grants.

Select the correct answer using the code given below.

(a) 1 only

(b) 2 only

(c) Both 1 and 2

(d) Neither 1 nor 2

Ans: (a)

Mains

Q. How have the recommendations of the 14thFinance Commission of India enabled the states to improve their fiscal position?(2021).

Q. How is the Finance Commission of India constituted? What do you about the terms of reference of the recently constituted Finance Commission? Discuss.(2018)

Q. Discuss the recommendations of the 13th Finance Commission which have been a departure from the previous commissions for strengthening the local government finances.(2013)