Indian Economy

Financial Inclusion in India

- 29 Aug 2025

- 15 min read

This article is based on the editorial "PM Jan Dhan Yojana has Removed Intermediaries to Ensure Subsidies Reach Beneficiaries," published in The Indian Express on 27/08/2025, which highlights how the flagship scheme has transformed financial inclusion by facilitating direct benefit transfers to the poor, while also pointing out enduring challenges such as limited digital literacy and underutilization of accounts.

For Prelims: Pradhan Mantri Jan Dhan Yojana (PMJDY), Pradhan Mantri Suraksha Bima Yojana (PMSBY), Atal Pension Yojana (APY), Stand-Up India Scheme (SUI), Kisan Credit Card (KCC), Financial Inclusion Index.

For Mains: Financial inclusion, Key drivers behind the growth of Financial Inclusion in India, Concerns regarding Financial Inclusion in India.

Financial inclusion is the backbone of India’s welfare state, ensuring subsidies and benefits reach the right beneficiaries without leakages. Flagship schemes like PM Jan Dhan Yojana have reduced intermediaries and enabled direct benefit transfers (DBT). Yet, gaps in usage, accessibility, and awareness show that true inclusion is still a work in progress.

What is Financial Inclusion?

- About:

- Financial Inclusion may be defined as the process of ensuring access to financial services and timely and adequate credit where needed by vulnerable groups such as weaker sections and low-income groups at an affordable cost (The Committee on Financial Inclusion, Chairman: Dr. C. Rangarajan).

- Key Components of Financial Inclusion:

- Access to Financial Services: Ensuring that financial services such as banking, insurance, and credit are available to everyone. This involves the establishment of physical banking outlets in underserved areas and the provision of digital financial services.

- Affordability: Financial products and services should be priced to be accessible for all segments of society. High costs can be a significant barrier, particularly for low-income groups.

- Financial Literacy: Educating individuals about financial products, services, and management is essential. Financial literacy empowers people to make informed decisions about their finances, including saving, investing, and managing credit.

- Usage: Beyond access, it's crucial that individuals actively use financial services to achieve financial stability and growth. This includes engaging with banking services, utilizing credit responsibly, and taking advantage of insurance products.

- Significance:

- Empowerment and Independence: Financially literate individuals are more capable of making sound financial decisions, reducing vulnerability to exploitation.

- Economic Growth: Financial inclusion boosts economic growth by mobilizing savings, generating employment, and enhancing productivity.

- Reduction of Inequality: By granting access to financial services, financial inclusion can address poverty and inequality.

- Financial Stability: A financially literate population can lead to greater financial stability, as individuals are better prepared to handle economic uncertainties.

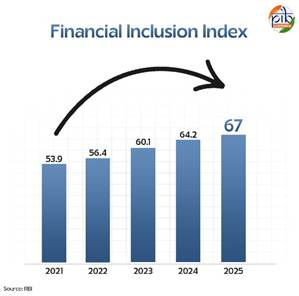

- RBI’s Financial Inclusion Index (FI-Index): It is a comprehensive measure of financial inclusion across banking, investment, insurance, pension, and postal sectors, developed with inputs from government and regulators.

- Published annually in July, scores range from 0 (exclusion) to 100 (full inclusion).

- The index has no base year, reflecting cumulative progress over time.

- Consists of three parameters: Access (35%), Usage (45%), and Quality (20%).

- The quality parameter is a unique feature that includes financial literacy, consumer protection, and service equity

- The index has steadily grown from 43.4 in March 2017 to 53.9 in March 2021, and now reaches 67 in March 2025.

What are the Key Drivers Behind the Growth of Financial Inclusion in India?

- Government Schemes and Policy Push :

- Pradhan Mantri Jan Dhan Yojana (PMJDY): A financial revolution providing savings accounts, RuPay cards, insurance, and overdraft facilities.

- As of 4 August 2025, 55.98 crore beneficiaries are enrolled, with over 55% accounts held by women.

- A network of 13.55 lakh Bank Mitras and 107 Digital Banking Units ensures last-mile delivery.

- Pradhan Mantri Suraksha Bima Yojana (PMSBY): Launched in 2015, it provides accident insurance of ₹2 lakh at an annual premium of ₹20. By March 2025, 50.54 crore enrolments were recorded.

- Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY): Offers life insurance of ₹2 lakh at an annual premium of ₹436.

- Over 23 crore people covered; more than 9 lakh families have benefited.

- Atal Pension Yojana (APY): Provides a pension of ₹1,000–₹5,000/month after 60 years.

- As of April 2025, 7.65 crore subscribers and ₹45,974 crore corpus, with 48% women participants.

- Pradhan Mantri MUDRA Yojana (PMMY): Supports micro and small enterprises with loans up to ₹20 lakh.

- By August 2025, 53.85 crore loans have been sanctioned worth ₹35.13 lakh crore, with focus on women, minorities, and first-time entrepreneurs.

- Stand-Up India Scheme (SUI): Promotes entrepreneurship among SC, ST, and women. By March 2025, ₹61,020 crore has been sanctioned.

- Mahila Samriddhi Yojana (MSY): Provides skill training and SHG loans up to ₹1.4 lakh. Till March 2025, ₹72,859 lakh disbursed to women.

- Kisan Credit Card (KCC): Offers affordable credit to farmers.

- Outstanding loan value rose from ₹4.26 lakh crore (2014) to ₹10.05 lakh crore (2024), benefiting 7.72 crore farmers.

- Nationwide Financial Inclusion Campaign (2025): A 3-month campaign covering Gram Panchayats and ULBs.

- Pradhan Mantri Jan Dhan Yojana (PMJDY): A financial revolution providing savings accounts, RuPay cards, insurance, and overdraft facilities.

- Digital Revolution:

- Unified Payments Interface (UPI): Launched in 2016, it powers 85% of digital transactions in India.

- In June 2025 alone, ₹24.03 lakh crore was transacted across 18.39 billion payments.

- Accounts for nearly 50% of global real-time transactions.

- Aadhaar-enabled Payment Systems (AePS): Aadhaar-based identity verification has brought millions into the financial mainstream.

- Digital wallets and fintech platforms (e.g., Paytm, PhonePe) are making financial access more convenient.

- Unified Payments Interface (UPI): Launched in 2016, it powers 85% of digital transactions in India.

- Microfinance Institutions and Fintech Innovation:

- Microfinance institutions (MFIs) like Bandhan Bank have empowered women borrowers.

- Fintechs leverage Artificial Intelligence (AI), Big Data, and Blockchain to provide Microloans, Instant Credit Scoring, and Peer-to-Peer Lending.

- Role of RBI and Banks:

- Priority Sector Lending (PSL) norms ensure Credit Flow to Agriculture, MSMEs, and Weaker Sections.

- Business Correspondents (BCs) and Banking Mitras bridge Last-Mile Connectivity in Rural Areas.

- National Centre for Financial Education (NCFE) (2013): Joint effort of RBI, SEBI, IRDAI, and PFRDA.

- Promotes financial education through workshops, seminars, and campaigns for all sections (children, youth, women, senior citizens).

- Reported a 17% rise in youth financial literacy (2016–2020).

- It’s National Strategy for Financial Education (NSFE) 2020-25 adopts a "5 C" approach – Content, Capacity, Community-led model, Communication, and Collaboration, and outlines a comprehensive approach to improving financial literacy.

What are the Concerns Regarding Financial Inclusion in India?

- Regional Disparities:

- Despite progress, states like Bihar, Chhattisgarh, and Odisha lag behind Kerala and Maharashtra in financial penetration.

- Bihar, with a per capita income barely above ₹68,000, underscores profound social and economic exclusion.

- Gender Disparities: Women face additional barriers to financial inclusion due to social, economic, and cultural factors.

- Only around 35% of active borrowers in India’s formal credit markets are women, highlighting a significant gender disparity in access to credit.

- The National Family Health Survey (NFHS-5) in India reveals that 33% of women use the internet, while the figure is 57% for men.

- Digital Divide:

- A joint study by the Internet and Mobile Association of India (IAMAI) and Kantar found that as of 2023, 45% of Indians—around 665 million people—do not access the internet

- Digital illiteracy and poor infrastructure hinder the adoption of online financial services.

- Informal Economy and Cash Dominance:

- About 90% of workers are engaged in informal sector jobs.

- Their heavy reliance on cash transactions, coupled with limited formal credit access, further inhibits the adoption of digital payments and financial services in this segment.

- Low Financial Literacy:

- According to the SEBI Investor Survey 2020, only 27% of Indians are financially literate.

- Lack of awareness about digital safety leads to cyber fraud and low insurance penetration.

- Poor Credit Access:

- Small and marginal farmers remain dependent on moneylenders due to rigid collateral requirements by banks.

- As per NITI Aayog’s Report on “Enhancing Competitiveness of MSMEs in India,” only 19% of MSME credit demand was met through formal sources by FY21.

- Corruption and Leakages:

- Though DBT (Direct Benefit Transfer) has reduced middlemen, ghost beneficiaries, and fake accounts, they still exist.

- Misuse of cooperative banks and scams highlight weak governance in certain financial institutions.

- India ranked 96th in the Corruption Perceptions Index (CPI) for 2024, down from 93rd in 2023, with a score of 38, a decline from 39 in 2023.

What Should be the Way Forward for Strengthening Financial Inclusion?

- Strengthening Digital Infrastructure:

- Expanding broadband connectivity in rural areas through the BharatNet project to bridge the digital divide.

- Promoting affordable smartphones and vernacular-language financial apps to enhance accessibility for rural and semi-literate populations.

- Implementing recommendations of the Nachiket Mor Committee (2013), which advocated for a Universal Electronic Bank Account and the establishment of specialized payments banks to deepen financial inclusion.

- Enhancing Financial Literacy:

- Embedding financial literacy in school curricula to build awareness from an early age.

- Leveraging Self-Help Groups (SHGs), Panchayats, and NGOs as community-based platforms to educate people about savings, insurance, and cyber safety.

- Following the recommendations of the Rangarajan Committee (2008), which stressed the importance of technology adoption and financial literacy as twin pillars for inclusive growth.

- Innovative Credit Solutions:

- Expand Kisan Credit Cards (KCCs) to all farmers.

- Encourage collateral-free loans through credit guarantee schemes for MSMEs.

- Promote fintech–bank partnerships for instant digital lending based on transaction data.

- Strengthening Regulatory Oversight:

- RBI should improve supervision of cooperative banks and NBFCs to prevent scams.

- Ensure transparency in microfinance institutions to protect borrowers from over-indebtedness.

- Inclusive Growth with Gender Lens

- Promote women-specific financial products like Mahila Shakti Kendras.

- Increase the representation of women in banking correspondents and self-help group linkages.

- Holistic Policy Coordination

- Financial inclusion should be linked with social inclusion (education, health, housing).

- India should further strengthen and build upon the National Strategy for Financial Inclusion (2019), introduced to address barriers in accessing financial services and products.

Conclusion:

The 2030 Agenda for Sustainable Development Goals identifies Financial Inclusion as a key enabler for 7 out of 17 goals. True inclusion goes beyond merely opening bank accounts—it requires building an ecosystem of accessible, affordable, and trustworthy financial services that genuinely empower citizens. The path forward lies in combining technology with trust, policy with people’s participation, and finance with fairness.

As PM Narendra Modi rightly emphasized, “Economic growth cannot only be restricted to a few cities and a few citizens. Development has to be all-round and all-inclusive.”

|

Drishti Mains Question : The 2030 Agenda for Sustainable Development identifies financial inclusion as a key enabler for multiple SDGs. In this context, analyze India’s efforts at financial inclusion and the roadblocks that hinder equitable growth. |

UPSC Civil Services Examination Previous Year Question (PYQ)

Prelims

Q. With reference to India, consider the following: (2010)

1. Nationalization of Banks

2. Formation of Regional Rural Banks

3. Adoption of village by Bank Branches

Which of the above can be considered as steps taken to achieve the “financial inclusion” in India?

(a) 1 and 2 only

(b) 2 and 3 only

(c) 3 only

(d) 1, 2, and 3

Ans: (d)

Mains

Q.Pradhan Mantri Jan Dhan Yojana (PMJDY) is necessary for bringing unbanked to the institutional finance fold. Do you agree with this for financial inclusion of the poorer section of the Indian society? Give arguments to justify your opinion. (2016)