Indian Economy

India’s Logistics Transformation for a Sustainable Future

- 25 Aug 2025

- 22 min read

The editorial, titled "How India’s Transport Future is Being Rewritten," was published in Hindustan Times on 25/08/2025. It highlights the government’s policy push for stricter fuel-efficiency standards and the Maritime Amrit Kaal Vision 2047 as game-changers for sustainable mobility and logistics efficiency. However, challenges such as high costs, infrastructure gaps, and the need for industry readiness persist.

For Prelims: National Logistics Policy (NLP), PM Gati Shakti, Economic Survey 2023-24, Multimodal Logistics Parks (MMLPs), World Bank’s Logistics Performance Index, Corporate Average Fuel Efficiency (CAFE).

For Mains: India’s Logistics Sector: Related Challenges & Way Forward

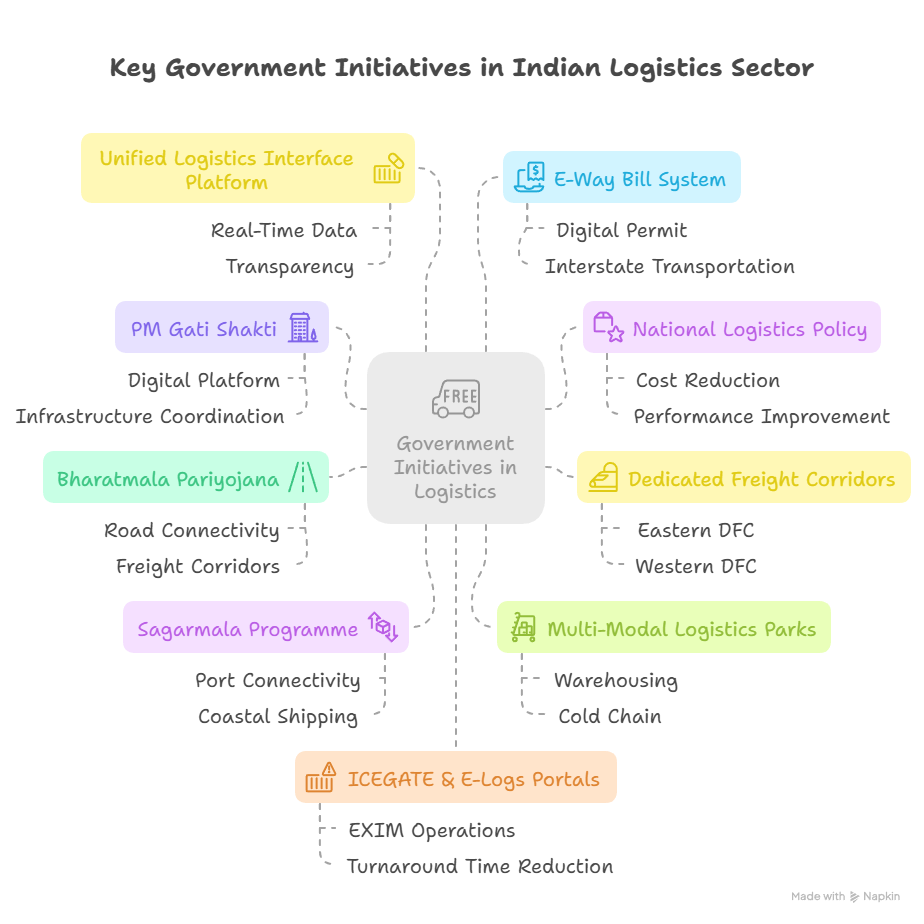

India’s logistics sector is at the cusp of transformation. Once synonymous with congestion, high logistics costs, and fragmented supply chains, it is now being reshaped through bold policy pushes such as the PM Gati Shakti National Master Plan, Dedicated Freight Corridors, and the development of multimodal logistics parks. These initiatives promise to lower transportation costs, improve efficiency, and build a more competitive backbone for trade and mobility. Yet, challenges persist, from high costs and infrastructure gaps to a shortage of skilled manpower. How India addresses these hurdles will determine whether logistics becomes a bottleneck or a backbone in its journey to Viksit Bharat@2047 and net-zero by 2070.

How is India Transforming Its Logistics Sector?

- Government Reforms: The government has been instrumental in accelerating the growth of the logistics sector.

- The PM Gati Shakti National Master Plan stands out as a transformative initiative, designed to build an integrated multi-modal transport network that seamlessly links rail, road, ports, and airways.

- This framework is expected to cut down transportation time and costs, while significantly boosting supply chain efficiency.

- The rollout of the Goods and Services Tax (GST) has further reshaped the sector by removing interstate tax barriers, ensuring quicker and more efficient movement of goods nationwide.

- The PM Gati Shakti National Master Plan stands out as a transformative initiative, designed to build an integrated multi-modal transport network that seamlessly links rail, road, ports, and airways.

- Infrastructure Push: Large-scale infrastructure projects such as the Dedicated Freight Corridors (DFC), the development of industrial corridors, and the establishment of logistics parks are reinforcing the sector’s backbone and paving the way for robust and sustainable growth.

- In FY 2023–24, India completed and commissioned over 1,000 km of DFC track, boosting daily train operations by 42%.

- A total of 35 Multimodal Logistics Parks (MMLPs) are being developed under the Bharatmala Pariyojana, with an estimated outlay of ₹50,000 crore.

- E-commerce Boom and Last-mile Connectivity: India’s e-commerce boom has fundamentally transformed the logistics landscape.

- The demand for faster and more dependable delivery solutions has surged, making last-mile delivery a critical focus.

- Companies are investing heavily to expand their networks into Tier 2 and Tier 3 cities, while hyperlocal delivery models are also gaining momentum, ensuring quicker turnaround times.

- India’s last-mile delivery market is projected to expand to USD 10.55 billion by 2032.

- Digital Transformation and Automation: Technology is reshaping India’s logistics sector through a paradigm shift in operations. AI-driven route optimization and IoT-enabled fleet management are making supply chains smarter, faster, and more data-centric.

- For instance, Delhivery has developed an AI-powered "RTO(Return to Origin) Predictor" that assesses the risk of a shipment being returned.

- At the same time, warehouse automation, robotics, and predictive analytics are streamlining processes, reducing errors, cutting turnaround times, and boosting overall efficiency.

- Blockchain technology is steadily gaining traction, strengthening transparency, traceability, and security across the supply chain.

- Together, these innovations are not only reducing costs but also elevating service quality, thereby enhancing the global competitiveness of Indian logistics.

- In India, the emergence of logistics start-ups backing this technology is gradually transforming the unorganized transportation sector.

- Growing Demand for 3PL and 4PL Services: As companies seek to optimize their supply chains, third-party logistics (3PL) and fourth-party logistics (4PL) providers are gaining prominence.

- These providers offer end-to-end logistics solutions, enabling businesses to focus on core operations while ensuring seamless warehousing, transportation, and distribution.

- The growing reliance on 3PL and 4PL services is expected to further drive efficiency and cost savings in the sector.

- 3PL accounts for the largest share of India’s overall logistics market in 2024.

- Workforce and Formalisation Drive: A systematic transition from informal to formal logistics has driven improvements in skilling, job creation, and overall workforce productivity.

- Government-supported initiatives such as Employee-Linked Incentive (ELI) schemes and targeted training programmes for logistics and warehousing are reshaping this traditionally unorganised sector.

- These efforts are also strengthening India’s demographic dividend by unlocking new employment opportunities and enhancing human capital.

- The sector currently employs 22 million people and is expected to create 10 million more jobs by 2027.

- Organised players, who hold 5.5–6% of the logistics market in FY22, are projected to grow at 32% CAGR till FY27.

- Sustainability and Green Transition: Growing environmental awareness and global ESG standards are driving a transformation in Indian logistics.

- The PM e-Drive scheme is promoting electric vehicles in logistics to reduce fossil fuel reliance and curb emissions, while ethanol blending is encouraged to reduce carbon emissions and support cleaner energy solutions.

- The sector is increasingly adopting electric vehicle fleets, coastal shipping, energy-efficient ports, and carbon-tracked supply chains to reduce its ecological footprint.

- India is also aligning with international benchmarks such as the Carbon Intensity Rating and the Energy Efficiency Existing Ship Index (EEXI) to promote sustainable shipping practices, while simultaneously attracting ESG-sensitive investments.

- Furthermore, initiatives like freight villages and coastal shipping corridors, supported by platforms such as the Sagar Sethu portal, are being scaled up to lower both emissions and logistics costs.

- 10 major highway segments in India have been designated for exclusive use of zero-emission trucks (ZETs) to decarbonize logistics, reduce air pollution, and enhance energy security on routes critical for freight transport.

What Factors Constrain the Efficiency of India’s Logistics Sector?

- High Logistics Cost: India’s logistics cost remains significantly higher than global benchmarks, impacting the competitiveness of exports and domestic production.

- India’s logistics costs have declined to around 7.8–8.9% of GDP in 2021–22, marking a significant improvement, yet they remain marginally higher than the global average.

- The fragmented supply chain, over-reliance on roads (70% of freight movement), and lack of modal integration inflate costs.

- This affects MSMEs the most, reducing their margins and limiting global competitiveness.

- Infrastructure Bottlenecks & Project Delays: Despite programs like Bharatmala and DFCs, gaps in road quality, port congestion, and rail connectivity persist, leading directly to increased delays and elevated logistics costs.

- For example, though the average turnaround time at major ports has fallen from 127 hours in 2010-11 to 53 hours as of 2021-22.

- The World Bank's Logistics Performance Index 2023 ranked India 38th out of 139 countries, with infrastructure quality being a key area of concern.

- Furthermore, delays in land acquisition and regulatory clearances continue to be a critical challenge for infrastructure projects.

- Lack of time bound land acquisition and clearances resulted in a delay of approximately 850 government run projects (till December 2022).

- For example, though the average turnaround time at major ports has fallen from 127 hours in 2010-11 to 53 hours as of 2021-22.

- Regulatory Fragmentation and Compliance Burden: The logistics ecosystem is governed by multiple ministries and departments, resulting in regulatory overlap and inefficiencies.

- Although the GST regime streamlined many interstate tax barriers, such policy fragmentation continues to inflate costs and hinder seamless operations.

- Moreover, even with the launch of PM Gati Shakti, coordination between the Centre and states remains inconsistent.

- Enterprises have to comply with several hundred acts and rules, depending on the size and geographical footprint of the business. These include the Carriage by Road Act, 2007 & Carriage by Road Rules, 2011 and the Warehousing (Development and Regulation) Act, 2007.

- Furthermore, some types of logistics companies also need to balance additional compliances contained in the Foreign Trade (Development & Regulation) Act, 1992 and Foreign Trade (Regulation) Rules, 1993.

- Although the GST regime streamlined many interstate tax barriers, such policy fragmentation continues to inflate costs and hinder seamless operations.

- Gaps in Multimodal Connectivity: Despite efforts to promote multimodal transportation, integration between different modes remains a challenge.

- As per NITI Aayog report (2021), road transport dominates with a 71 % modal share of freight movement, while rail accounts for just 18 %, and inland waterways a negligible 2%.

- This disproportion underscores the difficulty of shifting cargo onto more efficient, sustainable modes.

- Furthermore, the Dedicated Freight Corridor (DFC) project has experienced significant delays, and the persisting gaps in multimodal integration continue to hinder logistics efficiency while driving up overall costs.

- As per NITI Aayog report (2021), road transport dominates with a 71 % modal share of freight movement, while rail accounts for just 18 %, and inland waterways a negligible 2%.

- Skill Gap and Workforce Challenges: The logistics sector faces a significant skill gap, with a shortage of trained professionals across various levels.

- The logistics sector, growing at a compound annual growth rate of 12%, is expected to add 10 million jobs by 2027, but there's a severe shortage of skilled workers.

- This skill gap is particularly acute in areas like supply chain management, warehouse operations, and technology adoption.

- Also, over 90% of the logistics industry is unorganized, leading to low productivity, unsafe work conditions, and limited career mobility.

- The logistics sector, growing at a compound annual growth rate of 12%, is expected to add 10 million jobs by 2027, but there's a severe shortage of skilled workers.

- Technology Gap in Logistics: Despite rapid growth, India’s logistics sector suffers from a significant digital divide. The absence of a centralized database to map goods movement hampers evidence-based policymaking and limits effective monitoring of freight flows.

- Existing digital solutions such as e-way bills, FASTag, and port community systems are fragmented and fail to provide end-to-end visibility across the supply chain.

- Moreover, poor adoption of advanced digital technologies like AI, IoT, and blockchain means that route optimization, fleet management, and predictive planning remain underutilized.

- As a result, many operators continue to rely on manual processes, leading to inefficient route selection, uninformed decisions, and rising logistics costs.

- Environmental Concerns and Sustainability: The logistics sector faces increasing pressure to reduce its environmental impact, particularly in terms of carbon emissions.

- In India, transport contributes nearly 14% of India’s CO₂ emissions, with 90% from road transport.

- Fuel economy and emission standards like phases 3 and 4 of Corporate Average Fuel Efficiency (CAFE) norms are still under finalisation.

- While the government has set ambitious targets, including reducing carbon intensity by 45% by 2030, the logistics sector lags in the adoption of sustainable practices.

- In India, transport contributes nearly 14% of India’s CO₂ emissions, with 90% from road transport.

- Cold Chain Deficit & Agri-Supply Chain Leakages: India's cold chain logistics infrastructure is significantly underdeveloped, leading to substantial post-harvest losses.

- Despite being the world's largest producer of milk and the second-largest producer of fruits and vegetables, the country faces a severe cold storage deficit.

- The cold chain sector is highly fragmented, with over 90% of facilities being privately owned.

- Due to this, approximately 40% to 50% of perishable agricultural produce is lost annually due to inadequate cold storage facilities and inefficient supply chain management.

What Reforms are Required to Boost India’s Logistics Sector?

- Streamline Regulatory Processes: Establish a single-window clearance system for logistics approvals across states and harmonise state-level regulations to create a truly unified national market.

- Expedite the rollout of faceless customs assessment to minimise physical interfaces and speed up clearances, building on the success of e-SANCHIT, which has already digitised customs documentation.

- By leveraging technology, fostering innovation, and simplifying regulatory processes, India can significantly reduce logistics costs and improve the overall ease of doing business.

- Expedite the rollout of faceless customs assessment to minimise physical interfaces and speed up clearances, building on the success of e-SANCHIT, which has already digitised customs documentation.

- Fast-tracking Infrastructure Development: Prioritise and accelerate the completion of critical infrastructure projects, with a special emphasis on enhancing multimodal connectivity.

- Strengthen last-mile connectivity to major economic centres and ports by expediting projects such as the Dedicated Freight Corridors (DFCs).

- Introduce a robust project monitoring framework, similar to the PM Gati Shakti National Master Plan, to track progress and ensure timely delivery of major logistics infrastructure initiatives, including canal development.

- Introducing clear Key Performance Indicators (KPIs) can track the impact of multimodal and last-mile projects, ensuring accountability and measurable efficiency gains.

- Promote Multimodal Transportation: Develop Integrated Multimodal Logistics Parks (IMLPs) at strategic hubs to enable smooth transfer across transport modes.

- Provide targeted incentives to shift cargo from road to more efficient alternatives such as rail and inland waterways.

- For instance, fast-track the implementation of the 35 logistics parks proposed under the Bharatmala Pariyojana.

- Encourage private sector participation in developing multimodal infrastructure through public-private partnerships (PPPs).

- In 2020, PPP accounted for 51% of cargo handling at major ports, and the Maritime India Vision 2030 aims to raise this share to over 75% by 2030.

- Provide targeted incentives to shift cargo from road to more efficient alternatives such as rail and inland waterways.

- Adopting Advanced Technologies: India must accelerate the adoption of technology-enabled solutions such as blockchain, big data, cloud computing, and digital twins to strengthen its logistics sector.

- Recent global trends show that these tools are critical for tackling supply chain disruptions and advancing sustainability.

- Although India’s current adoption levels remain modest, the government’s digital initiatives like ICEGATE (Indian Customs Electronic Gateway) and E-Logs have already demonstrated the benefits of reducing inefficiencies, improving transparency, and speeding up goods movement.

- Scaling up such technology-driven measures is essential for creating a resilient, transparent, and globally competitive logistics ecosystem.

- Building a Skilled Logistics Workforce: A dedicated skilling mission, under Skill India and the Logistics Sector Skill Council, should focus on building expertise in warehouse operations, multimodal handling, and digital technologies.

- Introducing modular training programmes linked to certification and employability incentives can enhance sectoral productivity.

- Special attention must be given to upskilling informal workers in areas such as emerging technologies and ESG compliance to align the workforce with future industry needs.

- Sustainability and “green skills” have become a global priority for corporations, nations, and individuals, making it essential for India’s logistics workforce to be trained in eco-friendly practices and energy-efficient technologies.

- Introducing modular training programmes linked to certification and employability incentives can enhance sectoral productivity.

- Formalising the Unorganised Logistics Sector: India must simplify compliance procedures and build an enabling framework that allows small fleet operators, local warehousing agents, and truckers to register, upgrade, and formalise their businesses.

- A unified logistics registration portal, access to affordable finance, and simplified GST processes can ease this shift.

- Additionally, logistics providers can utilize the ONDC platform to streamline operations, optimize routes, and consolidate shipments from multiple sellers.

- Promoting Green Logistics: The transition to sustainable logistics is no longer optional, but a necessity for maintaining global competitiveness and meeting climate commitments.

- Moreover, India should promote EV adoption in logistics through subsidies, charging infrastructure, and battery support, while also encouraging alternate fuels like CNG and biofuels

- A NITI Aayog report estimated that fleet electrification alone represents a USD 200 billion opportunity for India as the country moves toward achieving a 30% EV sales share by 2030.

- Agri-Centric Cold Supply Chain Networks: India needs farm-gate integrated cold chains linked directly with processing units, mandis, and export hubs.

- This requires solar-powered pack houses, reefer trucks, and AI-driven demand forecasting to minimize food wastage.

- Farmer Producer Organizations (FPOs) should be incentivized to co-own cold infrastructure. Such networks will not only reduce post-harvest losses but also boost farmers’ incomes and agri-exports.

- Geo-Strategic Logistics Diplomacy: India should pursue logistics diplomacy with neighbors and global partners by securing cross-border transport agreements, transit rights, and port access.

- Linking BIMSTEC, INSTC, IMEC, and Indo-Pacific supply chains strengthens India’s strategic influence.

- This makes logistics a tool of both economic growth and foreign policy leverage.

Conclusion

India’s logistics sector is poised to become a driver of sustainable growth if reforms are matched with decisive execution. By embracing technology, green mobility, and workforce skilling, the sector can strengthen competitiveness while advancing SDG 8 (Decent Work), SDG 9 (Infrastructure & Innovation), and SDG 13 (Climate Action). A future-ready logistics backbone will be central to India’s journey toward Viksit Bharat 2047.

|

Drishti Mains Question India’s logistics sector is undergoing rapid transformation through reforms and infrastructure push, yet inefficiencies remain. Examine the major constraints to the sector’s growth and suggest significant measures. |

UPSC Civil Services Examination Previous Year Question (PYQ)

Q. The Gati-Shakti Yojana needs meticulous coordination between the government and the private sector to achieve the goal of connectivity. Discuss. (2022)