Governance

Unlocking Cooperatives' Potential in Empowering MSMEs

- 07 Jul 2025

- 12 min read

For Prelims: International Day of Cooperatives, Cooperatives, MSMEs, PM Vishwakarma scheme, Multi-state Cooperative Societies (MSCS), RBI, NABARD, White Revolution, IFFCO, PACS, GST, National Cooperative Policy 2023, MUDRA, CGTMSE, FPOs.

For Mains: Cooperatives and their role in the Indian economy and strengthening of MSMEs, Challenges that hinder effective use of cooperatives in empowering MSMEs in India and way forward.

Why in News?

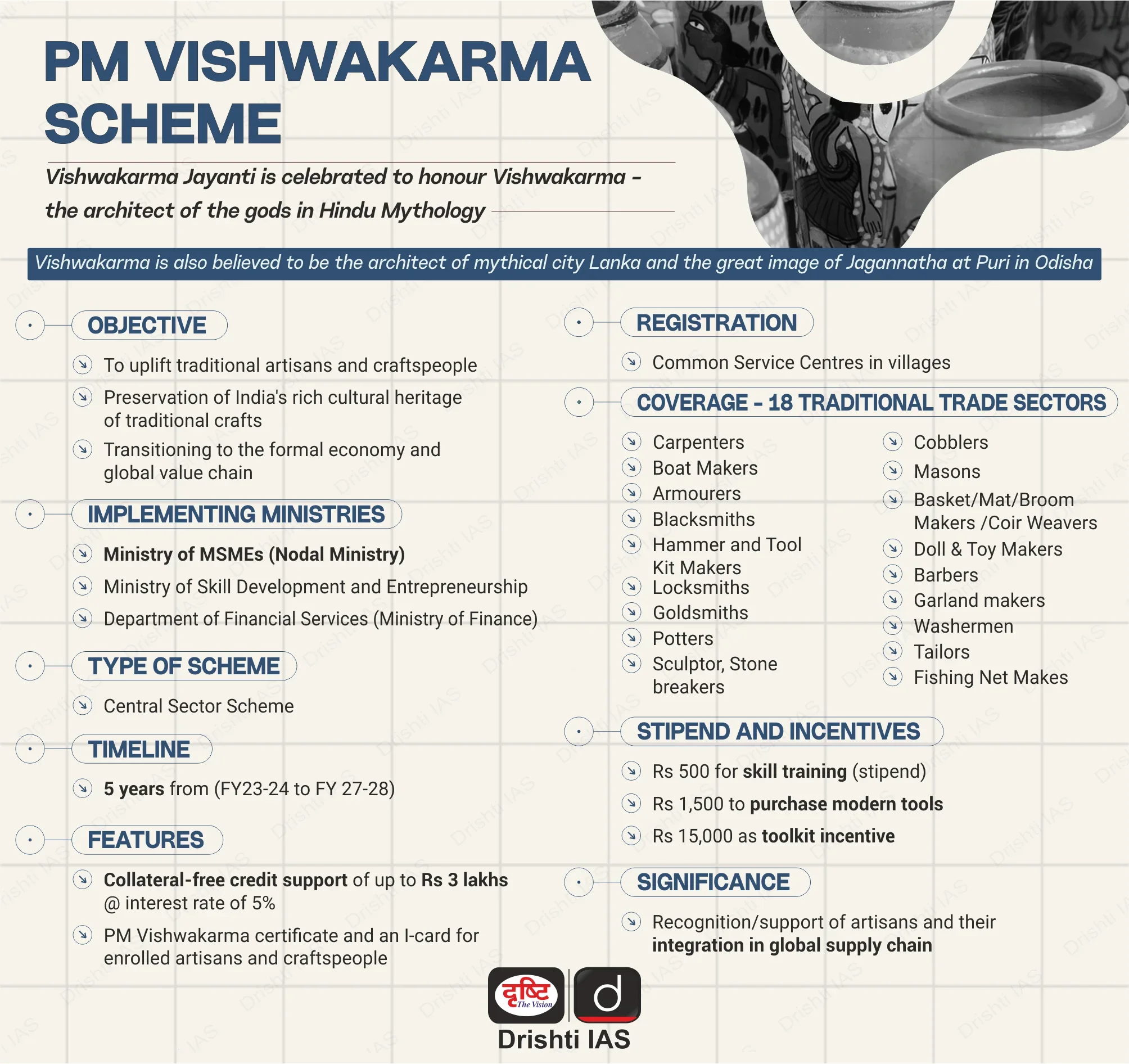

As India celebrates the International Day of Cooperatives (5th July, 2025) and marks four years of the Ministry of Cooperation, the focus is on harnessing the potential of cooperatives and MSMEs, especially through initiatives like the PM Vishwakarma scheme to empower artisans and promote inclusive economic growth.

How Can Cooperatives Contribute to Boosting the MSME Sector in India?

- Financial Empowerment & Resource Pooling: Cooperatives allow MSMEs to pool financial resources, reducing reliance on high-interest informal loans.

- For example, under the PM Vishwakarma scheme, artisan cooperatives can access credit at lower interest rates (5–7%) compared to individual borrowers.

- Additionally, cooperatives help MSMEs share resources like machinery and raw materials, lowering costs and improving operational efficiency, particularly for small-scale producers.

- Enhanced Market Access: Cooperatives can help MSMEs tap into larger markets through collective marketing, branding, and quality certifications.

- This boosts visibility and competitiveness, allowing smaller businesses to expand their reach and gain access to national and global markets.

- Technology Adoption: Cooperatives can set up cluster-level training centers for skill upgradation (e.g., carpentry, pottery, tailoring) and modern techniques like digital tools and automation.

- Synergy with Government Schemes: Cooperatives can act as an effective delivery mechanism for government schemes like the PM Vishwakarma, ensuring MSMEs, particularly artisans, receive financial, technical, and market support.

- This integration enhances the reach and impact of government initiatives aimed at MSME development.

- Sustainable & Inclusive Growth: MSME cooperatives like Lijjat Papad and SEWA empower women entrepreneurs and support rural empowerment, while waste-sharing and recycling initiatives promote the circular economy.

What are Cooperatives in India?

- About: Cooperatives are people-centred enterprises owned and run by members to fulfill their economic, social, and cultural needs.

- India hosts one of the world's largest cooperative networks, with over 800,000 cooperatives across sectors like agriculture, credit, dairy, housing, and fisheries.

- Evolution of Cooperative Sector in India:

- First Five-Year Plan (1951–56): Emphasized promotion of cooperatives for comprehensive community development.

- Multi-State Co-operative Societies Act, 2002: Provides for the formation and functioning of multi-state cooperative societies (MSCS).

- 97th Constitutional Amendment Act, 2011: Made formation of cooperatives a fundamental right (Article 19).

- Introduced a new Directive Principle (Article 43-B) on cooperative societies.

- Added Part IX-B (Articles 243-ZH to 243-ZT) titled “The Co-operative Societies”.

- Empowered Parliament to enact laws for MSCS and state legislatures for other cooperatives.

- Establishment of the Union Ministry of Cooperation (2021) provides a dedicated policy framework, and empowered grassroots governance under the vision of “Sahakar se Samriddhi”.

- The Multi-State Co-operative Societies (Amendment) Act, 2022 introduced an Election Authority, created a Rehabilitation Fund, and allowed state-level mergers.

- Key Contributions:

- Employment Generation: Cooperatives provide 13.3% of India's direct employment, engaging 29 crore members across 8.14 lakh societies, creating livelihoods in both rural and urban areas.

- Agricultural Development: Cooperatives disburse 15% of short-term agricultural credit, manage 30% of sugar production, and handle 35% of fertilizer distribution

- Financial Inclusion: With 20% of cooperatives in banking, they provide affordable credit to farmers and small businesses, enhancing financial access in remote areas.

- Food Security: Cooperatives like Amul, NAFED, and IFFCO play a pivotal role in milk production, dairy exports, and the distribution of agro-products.

- Women Empowerment: Cooperatives like SEWA and Lijjat Papad empower women, promote self-help groups (SHGs).

Notable Cooperatives in India:

- Primary Agricultural Credit Societies (PACS): Grassroot arms of the short-term cooperative credit structure, linking farmers with Scheduled Commercial Banks, RBI, and NABARD.

- AMUL (Anand Milk Union Limited): A dairy giant and White Revolution pioneer, AMUL is a federation of milk producers in Gujarat that helped make India the world's largest milk producer.

- IFFCO (Indian Farmers Fertiliser Cooperative): One of the world's largest fertiliser cooperatives, IFFCO provides quality fertilisers and agricultural inputs to farmers across India.

- HOPCOMS (Horticultural Producers' Cooperative Marketing and Processing Society): Known for its farm produce outlets, ensuring fair returns to farmers.

- Lijjat Papad (Shri Mahila Griha Udyog Lijjat Papad): A women’s cooperative empowering women through papad production.

| Click Here to Read: What are MSMEs?, Role of MSMEs in India’s Economic Growth?, Recommendations by NITI Aayog on MSMEs. |

What Challenges Limit the Effectiveness of Cooperatives in Empowering MSMEs in India?

- Misconceptions: Many MSME owners perceive cooperatives as government-controlled or political bodies, not as business enablers.

- There is a lack of awareness about various cooperative models like producer cooperatives, credit societies, and marketing federations.

- Weak Financial Support: Cooperative banks often face liquidity crises, limiting MSME lending, while traditional banks hesitate to lend to cooperatives due to perceived risk and lack of credit history.

- Regulatory Complexity: Multiple laws like the Cooperative Societies Act, State Cooperative Laws, and GST compliance create confusion, while excessive bureaucracy delays registration and operational approvals.

- Lack of Digital Adoption: Many cooperatives operate in isolation, missing economies of scale, and low tech adoption (e.g., digital accounting, e-commerce) limits their market reach.

- Governance Deficits: Many cooperatives suffer from poor transparency, accountability, and internal audits, weakening their role as reliable intermediaries for MSMEs.

What Measures are Needed to Strengthen Cooperatives for Empowering MSMEs in India?

- Policy & Regulatory Reforms: Provide tax benefits to MSMEs in cooperatives (e.g., lower GST), prioritize them in public procurement, reduce compliance burdens (e.g., simplified GST filing), and align state laws with the National Cooperative Policy 2023.

- Financial & Credit Support: Expand cooperative banking access by strengthening PACS for non-farm MSMEs, linking cooperatives to MUDRA, CGTMSE, and NABARD, and promote cooperative fintech platforms and digital banking training.

- Infrastructure Upgradation: Adopt digital tools like e-commerce integration (ONDC, GeM), build Common Facility Centers for production, testing, and packaging and logistics cooperatives to to reduce transport costs.

- Market Linkages & Branding: Promote collective branding and certification through “CoopMade” labels and boost e-commerce by linking cooperatives to platforms like Amazon Karigar, and develop export clusters.

- Awareness & Advocacy: Launch national campaigns like “Cooperatives for Atmanirbhar MSMEs” to showcase success stories through media, and drive grassroots mobilization by engaging SHGs, FPOs, and industry associations.

Conclusion

Cooperatives, strengthened by policy reforms, digital adoption, and financial inclusion, can revolutionize MSME empowerment in India. By addressing governance gaps and enhancing market linkages, they can drive inclusive growth, particularly for artisans and women entrepreneurs. The synergy between cooperatives and schemes like PM Vishwakarma can fuel India’s Atmanirbhar Bharat vision.

|

Drishti Mains Question Discuss how cooperatives can play a transformative role in empowering MSMEs in India. |

UPSC Civil Services Examination, Previous Year Question (PYQ)

Prelims

Q. Consider the following statements with reference to India : (2023)

- According to the Micro, Small and Medium Enterprises Development (MSMED) Act, 2006, the ‘medium enterprises’ are those with investments in plant and machinery between `15 crore and `25 crore.

- All bank loans to the Micro, Small and Medium Enterprises qualify under the priority sector.

Which of the statements given above is/are correct?

(a) 1 only

(b) 2 only

(c) Both 1 and 2

(d) Neither 1 nor 2

Ans: (b)

Q. With reference to ‘Urban Cooperative Banks’ in India, consider the following statements: (2021)

- They are supervised and regulated by local boards set up by the State Governments.

- They can issue equity shares and preference shares.

- They were brought under the purview of the Banking Regulation Act, 1949 through an Amendment in 1966.

Which of the statements given above is/are correct?

(a) 1 only

(b) 2 and 3 only

(c) 1 and 3 only

(d) 1, 2 and 3

Ans: (b)

Mains

Q. “In the Indian governance system, the role of non-state actors has been only marginal.” Critically examine this statement. (2016)

Q. “In the villages itself no form of credit organisation will be suitable except the cooperative society.” – All India Rural Credit Survey. Discuss this statement in the background of agricultural finance in India. What constraints and challenges do financial institutions supplying agricultural finance face? How can technology be used to better reach and serve rural clients? (2014)