Governance

8 Years of GST

- 03 Jul 2025

- 12 min read

For Prelims: Goods and Services Tax (GST), Indirect Tax System, E-way Bills, MSMEs, Cascading Effect, Input Tax Credit (ITC), VAT, GST Appellate Tribunal (GSTAT), GST Council, Inverted Duty Structure, GST Network (GSTN), ICEGATE, Carbon Credits.

For Mains: Performance of GST in last 8 years and associated challenges, Measures required to strengthen the existing GST framework.

Why in News?

As Goods and Services Tax (GST) completes 8 years since its launch on 1st July 2017, experts acknowledge its success in tax integration and digitisation, while emphasizing the need for simplification, rate rationalisation, and reduced compliance burden.

What are the Key Achievements of GST over the Past 8 years?

- Record Revenue Growth: GST revenues have consistently grown, with the highest ever gross collection of Rs 22.08 lakh crore in FY 2024-25, with an average monthly collection of Rs 1.84 lakh crore.

- This growth has outpaced nominal GDP, reflecting better compliance, reduced tax evasion, and increased economic formalization.

- Digital Transformation & Compliance Efficiency: GST has undergone digitization—from manual filings to e-invoicing, real-time credit matching, automated returns, and e-way bills—reducing errors and fraud.

- While MSMEs, once hesitant, now see it as a gateway to credit, government procurement, and national market access.

- Expanded Taxpayer Base: As of 30th April, 2025, India boasts over 1.51 crore active GST registrations, marking a significant increase from 65 lakh in 2017.

- This growth underscores the success of GST in formalizing the economy and enhancing tax compliance.

- Ease of Doing Business: GST has removed inter-state tax barriers, lowering logistics costs and enhancing supply chain efficiency, while the elimination of entry taxes and octroi has led to further business cost savings.

- GST’s ‘One Nation, One Tax’ framework replaced the multi-layered tax system, reducing cascading effects while the Input Tax Credit (ITC) mechanism ensured seamless credit flow, lowering business costs and boosting competitiveness.

- Efficient Refund Processing: Automated Integrated GST (IGST) refunds via the Customs ICEGATE portal have sped up processing to within a week, with ₹1.18 lakh crore disbursed in FY25, boosting exporter liquidity.

What is the Goods and Services Tax (GST)?

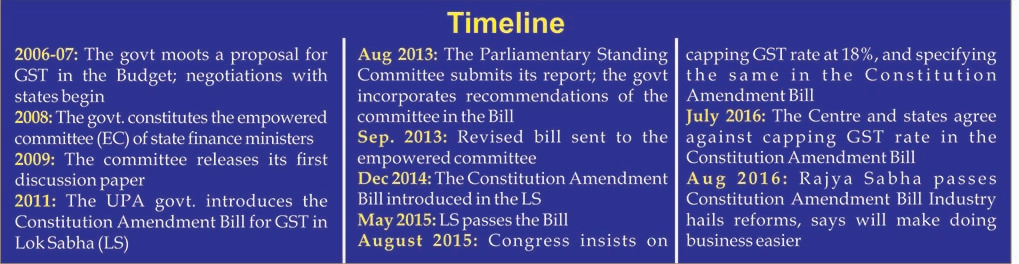

- About: The 101st Amendment Act, 2016 introduced a unified indirect tax system across India by subsuming multiple central and state taxes under GST.

- GST is a value-added tax levied on the supply of all goods and services.

- It replaced central taxes like Excise Duty, Additional Excise Duties, and Service Tax, and state taxes like VAT, Central Sales Tax, and Luxury Tax.

- Main Features:

- Supply-Based Taxation: GST is levied on the supply of goods and services, unlike earlier taxes which were imposed on manufacture, sale, or service provision.

- Destination-Based System: GST operates as a destination-based consumption tax, replacing the older origin-based taxation model.

- Multiple Tax Slabs: GST is imposed at five different rates-0%, 5%, 12%, 18%, and 28%, with product classification guided by the GST Council.

- Dual Structure: GST has a dual framework, where both the Centre (CGST) and the States (SGST) levy tax on the same transaction value.

- Imports of goods and services are considered inter-state supplies and attract IGST, in addition to applicable customs duties.

- Governance: GST Council is a key decision making body. Goods and Services Tax Network (GSTN) provides an IT system for the GST portal.

- The Centre and States decide CGST, SGST, and IGST rates based on the recommendations of the GST Council.

What are Key Challenges in the Current GST Framework?

- Exclusion of Items: Petroleum products and alcohol for human consumption remain outside GST, leading to tax cascading and cash flow issues due to ineligible ITC.

- While states levy VAT under Entry 54 of the State List and Article 366(12A), raising concerns over revenue loss and fiscal autonomy if included under GST.

- Delay in GST Appellate Tribunal (GSTAT): The long-delayed GST Appellate Tribunal (GSTAT), though recently notified, remains non-functional in several states, leading to a backlog of appeals in High Courts, prolonged adjudication, and uncertainty for taxpayers.

- Complex Rate Structure: GST currently has five main slabs along with special rates of 0.25%, 1%, and 3% (mainly for gold, silver, and diamonds), leading to classification disputes, frequent litigation, and working capital issues in inverted duty structure sectors.

- Though the original intent was to rationalise a three-rate system, there has been no significant progress despite expert recommendations and GST Council discussions.

- Procedural and Compliance Hassles: Despite progress in automation and digitalisation, procedural challenges persist, including high-value litigations on minor issues, over-regulation, and frequent rule changes with complex notifications.

- Experts note that these procedural hassles often overshadow the government’s broader efforts at simplification.

- Interpretational Ambiguities: Ambiguities in interpreting intermediary services, intra-company transactions, and employee secondment under GST persist despite circulars, causing compliance grey areas, operational hurdles, and increasing litigation risks for businesses.

What Reforms can be Implemented to Improve the Current GST Framework?

- Phased Approach: A phased approach for petroleum inclusion could begin with natural gas and Aviation Turbine Fuel (ATF), using a revenue-neutral rate and a temporary compensation mechanism for states, is a valid strategy to ensure smooth integration.

- While Article 366(12A) excludes alcohol for human consumption from GST, its inclusion can be facilitated by offering higher devolution shares,

- Launching pilot projects in states with low reliance, and providing long-term fiscal safeguards to build consensus.

- While Article 366(12A) excludes alcohol for human consumption from GST, its inclusion can be facilitated by offering higher devolution shares,

- Rationalization of GST Rate Slabs: Address the inverted duty structure by speeding up refunds, rebalancing input taxes (on man-made fiber), and revisiting the compensation cess through phasing out or merging with the highest GST slab.

- Strengthening Dispute Resolution: Operationalize GSTAT nationwide by fast-tracking tribunal appointments to clear pending appeals in High Courts and ensure standardized rulings to prevent conflicting interpretations.

- To reduce litigation on minor issues, implement an amnesty scheme waiving penalties for early procedural lapses and issue binding circulars on ambiguities.

- Digital Integration: Implement single-window compliance by integrating GST Network (GSTN) with ICEGATE, Directorate General of Foreign Trade (DGFT), RBI, and Ministry of Corporate Affairs (MCA) for real-time data sharing and auto-filled returns.

- Use AI-driven scrutiny to streamline refunds and audits with time-bound processing, like 15-day refunds for exporters.

- Expanding the Tax Base to New Sectors: Next-generation GST reform must proactively address emerging sectors like crypto-assets, carbon credits, and digital goods/services to ensure clarity, uniformity, and alignment with global standards.

Conclusion

GST has transformed India’s tax landscape, boosting revenue and formalization. However, challenges like petroleum exclusion, rate complexity, and dispute delays persist. Reforms—phased inclusion of excluded sectors, slab rationalization, faster dispute resolution, and digital integration—are vital to make GST a true "One Nation, One Tax" system and fuel India’s USD 5 trillion economy ambition.

|

Drishti Mains Question: Q. While GST has streamlined India’s indirect tax system, structural and operational challenges remain." Critically analyze this statement and suggest reforms. |

UPSC Civil Services Examination Previous Year Question (PYQ)

Prelims

Q. Consider the following items: (2018)

- Cereal grains hulled

- Chicken eggs cooked

- Fish processed and canned

- Newspapers containing advertising material

Which of the above items is/are exempted under GST (Good and Services Tax)?

(a) 1 only

(b) 2 and 3 only

(c) 1, 2 and 4 only

(d) 1, 2, 3 and 4

Ans: (c)

Q. What is/are the most likely advantages of implementing ‘Goods and Services Tax (GST)’? (2017)

- It will replace multiple taxes collected by multiple authorities and will thus create a single market in India.

- It will drastically reduce the ‘Current Account Deficit’ of India and will enable it to increase its foreign exchange reserves.

- It will enormously increase the growth and size of the economy of India and will enable it to overtake China in the near future.

Select the correct answer using the code given below:

(a) 1 only

(b) 2 and 3 only

(c) 1 and 3 only

(d) 1, 2 and 3

Ans: (a)

Mains

Q. Explain the rationale behind the Goods and Services Tax (Compensation to States) Act of 2017. How has COVID-19 impacted the GST compensation fund and created new federal tensions? (2020)

Q. Enumerate the indirect taxes which have been subsumed in the Goods and Services Tax (GST) in India. Also, comment on the revenue implications of the GST introduced in India since July 2017. (2019)