Indian Economy

Voluntary Amalgamation of Co-operative Banks

- 03 Jul 2025

- 13 min read

For Prelims: Urban Co-operative Bank (UCB), Reserve Bank of India (RBI), Banking Regulation Act, 1949,, Credit Societies, Multi-State Co-operative Societies Act, 2002, Non-Performing Asset (NPA)

For Mains: Key Features of Cooperative Banks and Challenges.

Why in News?

Saraswat Co-operative Bank (SCB), the largest Urban Co-operative Bank (UCB) in India, has received in-principle approval from the RBI to acquire the fraud-hit New India Co-operative Bank (NICB) under the RBI’s Voluntary Amalgamation Scheme for UCBs.

What is RBI’s Voluntary Amalgamation Scheme for UCBs?

- About: The Voluntary Amalgamation Scheme is a regulatory framework introduced by the RBI to facilitate the voluntary merger of two or more UCBs. Its primary objective is to ensure financial stability and protect the interests of depositors.

- This scheme is governed by the Master Direction on Amalgamation of Urban Co-operative Banks, 2020, issued under:

- Section 35A of the Banking Regulation Act, 1949, which grants the RBI the authority to issue directions to banks in public interest or for proper management.

- Section 44A, which addresses the voluntary amalgamation of banking companies, including UCBs.

- Section 56, which extends the provisions of the Act to co-operative banks, with necessary modifications.

- Amalgamation is permitted only when specific conditions related to financial soundness and depositor protection are met. Approvals are required from the boards, shareholders, and the RBI.

- This scheme is governed by the Master Direction on Amalgamation of Urban Co-operative Banks, 2020, issued under:

- Legal Backing: The scheme is legally supported by the Banking Regulation (Amendment) Act, 2020, which strengthens the RBI’s authority to direct, approve, or reject UCB amalgamations to ensure financial stability and protect depositor interests.

- In these mergers, the Amalgamated Bank is the weaker UCB transferring its business, while the Amalgamating Bank is the stronger UCB acquiring it.

- Conditions for Amalgamation:

- Positive Net Worth: The merger can proceed if the amalgamated bank has a positive net worth, with the stronger bank ensuring full protection of depositors' funds.

- Without Government Support: If the amalgamated bank has a negative net worth, the stronger bank may merge while voluntarily protecting all depositors' funds, without external assistance.

- With Government Support: If the amalgamated bank has a negative net worth, the merger can proceed with full depositor protection, backed by financial support from the State Government.

- Approval Process for Amalgamation:

- Board Approval: The amalgamation requires approval from a two-thirds majority of the total board members of both the amalgamating and amalgamated UCBs, not just those present and voting.

- Shareholder Approval: Approval from two-thirds of shareholders (in number and value) of each UCB is required, with the shareholders present in person at a specially convened meeting.

- RBI Sanction: After obtaining board and shareholder approvals, the draft amalgamation scheme must be submitted to the relevant Regional or Central Office of the RBI for final approval.

- Applicability: Applicable to all Primary (Urban) Co-operative Banks, including both single-state and multi-state UCBs.

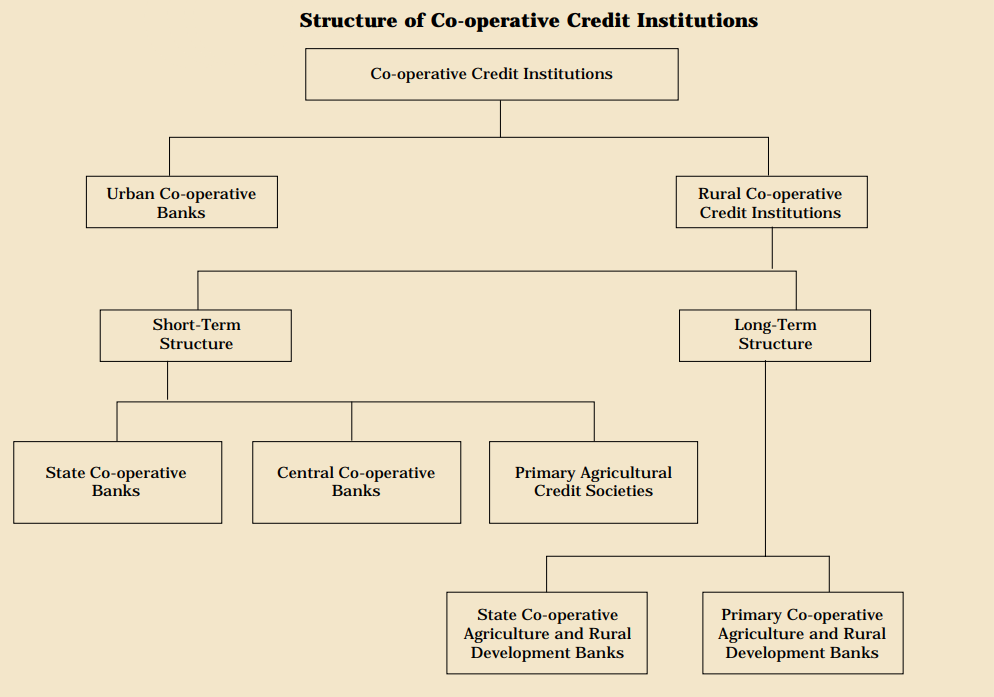

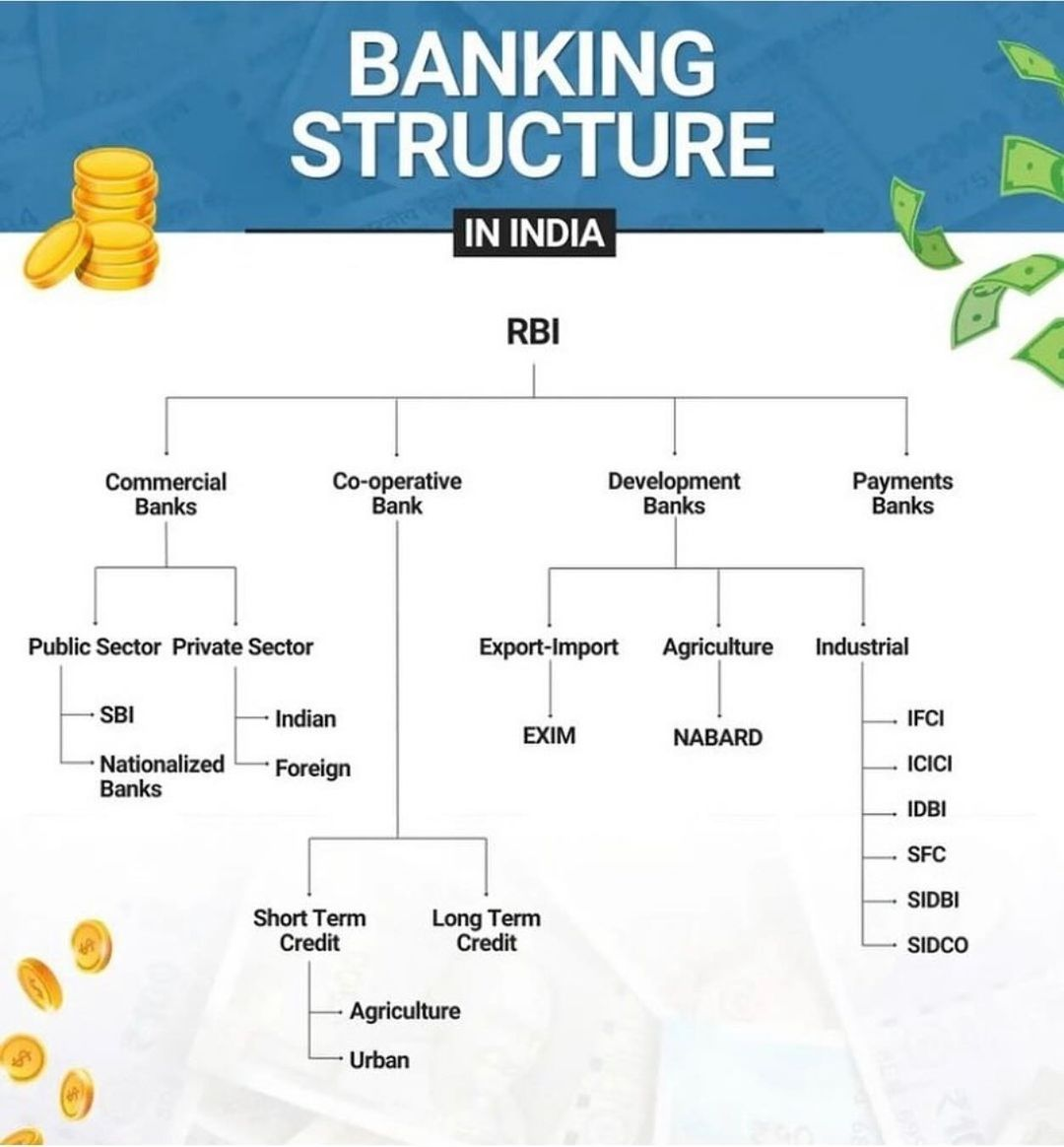

What are Co-operative Banks?

- About: Co-operative Banks are financial institutions set up as Co-operative Societies, registered under either the State Co-operative Societies Acts or the Multi-State Co-operative Societies Act, 2002, and engaged in banking business.

- Objective: To provide affordable credit to farmers, small businesses, self-employed, and low-income groups, especially in rural and semi-urban areas.

- Ownership & Governance: Owned and managed by their members, who are also the customers.

- It follows the “one person, one vote” principle, ensuring democratic control.

- Regulatory Framework: Co-operative banks operate under a dual regulatory system:

- RBI’s Role:

- The RBI regulates co-operative banks under the Banking Regulation Act, 1949, ensuring compliance with capital adequacy, lending norms, and financial supervision.

- It has the authority to cancel a bank’s license if it fails to meet regulatory norms or ceases operations.

- The Banking Regulation (Amendment) Act, 2020 has enhanced RBI’s powers to intervene in the management and governance of Urban Co-operative Banks (UCBs).

- Registrar of Co-operative Societies (RCS):

- The administrative functions are overseen by the respective state governments or the central government through the RCS).

- RBI’s Role:

What is the Significance of UCBs in India?

- Promoters of Financial Inclusion: UCBs play a crucial role in serving small borrowers, micro-businesses, and low-income groups in urban and semi-urban areas, thereby enhancing financial access.

- Community-Centric Operations: Their localised focus allows UCBs to better understand and meet community-specific credit needs with customised financial services.

- Priority Sector Lending (PSL) Obligations: UCBs are mandated to allocate 65% of their adjusted net bank credit (ANBC) to PSL in FY 2024–25, with a target to increase it to 75% by March 2026, supporting key sectors like MSMEs, housing, and education.

- Support to Non-Agricultural Urban Sectors: Historically restricted to non-agricultural lending until 1996, UCBs now play an important role in financing urban development and small-scale enterprises, complementing commercial banks in credit outreach.

Recent Developments in Co-operative Banking and Regulations

- National Co-operative Policy (2025–2045): Launched by the Union Government, the 20-year policy aims to establish one co-operative in every village and create 2 lakh new PACS by February 2026, promoting grassroots financial inclusion, rural development, and the vision of “Sahakar se Samriddhi.”

- Reforms in Priority Sector Lending (PSL) Norms: From April 2025, UCBs are required to allocate 60% of Adjusted Net Bank Credit (ANBC)/ Credit Equivalent of Off-Balance Sheet Exposures (CEOBE) to PSL, revising older benchmarks.

- For Small Finance Banks (SFBs), the PSL mandate has been reduced from 75% to 60% from FY 2025–26 to align them with universal banks and enhance operational flexibility in lending.

- Enhanced Regulatory Oversight by RBI: In FY 2024–25, the RBI intensified its supervision of UCBs by issuing 215 penalties, cancelling 7 licenses, and placing 23 UCBs under restrictions for violations including KYC breaches, high NPAs, and frauds. Key reforms included:

- Revised prudential norms for increased loan ceilings, relaxed provisioning timelines, and adjusted real estate exposure limits.

- Extension of Prompt Corrective Action (PCA) to UCBs (from April 2025).

- Master Direction on Fraud Management (2024), introduced early warning systems and accountability mechanisms for fraud risk mitigation.

- Digital & Institutional Strengthening: RBI mandated Core Banking System (CBS) adoption for all UCBs by March 2025, supported by NABARD and fintechs.

- The government launched NUCFDC to offer shared digital infrastructure and services. Policy reforms aim to streamline PACS liquidation and registration, replacing defunct units with tech-enabled, well-governed cooperatives.

What are the Challenges Faced by UCBs in India?

- Weak Governance and Fraud Risks: Many co-operative banks face issues like political interference, nepotism, and poor internal controls, leading to financial mismanagement, frauds, and erosion of depositor trust (PMC Bank scam).

- In 2023–24 alone, 24 UCB licenses were cancelled.

- Regulatory and Supervisory Constraints: The legacy of dual regulation by RBI and State Registrars created compliance issues and operational inefficiencies. Although the Banking Regulation (Amendment) Act, 2020 brought UCBs under RBI’s full oversight, overlapping functions still pose challenges.

- Financial Weakness and High NPAs: Many UCBs suffer from capital inadequacy, limited fund access, and rising NPAs—Gross NPAs stood at 8.8% in March 2024, affecting their profitability and stability.

- Limited Scale and Technological Obsolescence: UCBs often operate in small geographies with limited membership and outdated infrastructure. Their lag in digital adoption affects efficiency, competitiveness, and customer service, especially against fintechs and commercial banks.

- Declining Sectoral Relevance: The share of co-operative banks in agricultural lending dropped from 64% (1992–93) to 11.3% (2019–20).

- Similarly, their share in total banking assets declined from 3.8% (2017) to 2.5% (2024), reflecting a shrinking footprint in the financial sector.

Way Forward

- Strengthen Governance and Oversight: Mandate professionalisation of UCB boards by requiring at least 50% of directors to have expertise in banking, finance, or law, ensuring better decision-making and risk management.

- Promote Consolidation: Encourage voluntary mergers of weak UCBs with stronger ones under the RBI’s Voluntary Amalgamation Scheme to build financially stable and efficient institutions.

- Ensure Independent and Regular Audits: Institutionalise regular audits by autonomous bodies to enhance transparency, accountability, and financial discipline across co-operative banks.

- Accelerate Technology Adoption: Promote the adoption of modern banking technology (e.g., core banking, mobile banking, cybersecurity) to improve operational efficiency and customer service.

- Introduce Social Audits: Implement stakeholder-led social audits to assess the effectiveness of policy implementation, fund allocation, and community impact, thereby deepening trust and inclusivity.

UPSC Civil Services Examination, Previous Year Question (PYQ)

Q. With reference to ‘Urban Cooperative Banks’ in India, consider the following statements:

- They are supervised and regulated by local boards set up by the State Governments.

- They can issue equity shares and preference shares.

- They were brought under the purview of the Banking Regulation Act, 1949 through an Amendment in 1966.

Which of the statements given above is/are correct?

(a) 1 only

(b) 2 and 3 only

(c) 1 and 3 only

(d) 1, 2 and 3

Ans: (b)

Mains:

Q. “In the Indian governance system, the role of non-state actors has been only marginal.” Critically examine this statement. (2016)

Q. “In the villages itself no form of credit organisation will be suitable except the cooperative society.” – All India Rural Credit Survey. Discuss this statement in the background of agricultural finance in India. What constraints and challenges do financial institutions supplying agricultural finance face? How can technology be used to better reach and serve rural clients? (2014)