Indian Economy

Scaling India's MSME Growth

- 08 Apr 2026

- 25 min read

This editorial is based on “MSMEs: From survival to scale” which was published in The Business Standard on 03/04/2026. This editorial examines the strategic transition of India's MSME sector from fragmented resilience to a globally competitive scale, highlighting recent digital and financial reforms. It provides a deep dive into structural challenges like the "missing middle" and delayed payments while offering ground-level solutions for sustainable growth.

For Prelims:MSMED Act 2006, Udyam Portal,PM Vishwakarma, Samadhaan Portal, Priority Sector Lending,CBAM.

For Mains: MSMEs as a growth engine, key issues and measures needed.

India’s Micro, Small and Medium Enterprises (MSMEs) form the backbone of its growth story, contributing nearly 31% to GDP, 48% to exports, and employing over 32 crore people. Yet, the sector remains structurally skewed, with a “missing middle”, a dominance of micro firms but a thin layer of scalable medium enterprises. Persistent challenges such as delayed payments and credit misalignment continue to lock up working capital and suppress growth potential. Thus, the MSME question is no longer about survival, but about enabling a transition from fragmented resilience to globally competitive scale.

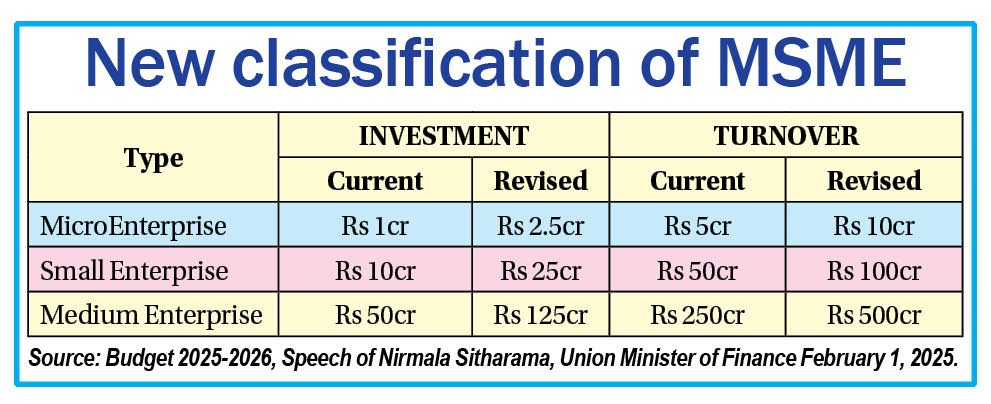

Micro, Small, and Medium Enterprises (MSME) Classification

- About: The Micro, Small, and Medium Enterprises (MSME) sector is often hailed as the "backbone of the Indian economy."

- It continues to be a massive driver of growth, employment, and exports, especially as the government pushes for the Viksit Bharat@2047 vision.

- Revised Classification (Effective April 2025): To help businesses grow without losing government benefits, the classification thresholds were significantly changed in 2025.

How is MSMEs Driving India’s Growth Story?

- Macroeconomic Engine and GDP Backbone: MSMEs serve as the primary engine for structural transformation by driving decentralized industrialization and transitioning India's workforce from agrarian dependency to productive manufacturing.

- This widespread enterprise ecosystem anchors local economies, reducing regional disparities and fostering self-reliance across multiple states.

- According to the Economic Survey 2025-26, MSMEs currently contribute a massive 31.1% to India's GDP and account for 35.4% of the country's total manufacturing output.

- With over 7.47 crore registered enterprises, this sector forms the critical bedrock required to achieve the Viksit Bharat@2047 economic vision.

- Export Powerhouse and Global Value Chains: By actively integrating into Global Value Chains (GVCs), small enterprises are elevating India's manufacturing footprint from domestic assembly to international competitiveness.

- This strategic shift into labor-intensive export markets effectively counterbalances the national trade deficit while establishing Indian goods as globally reliable assets.

- For instance, the MSME share in India’s total merchandise exports has surged to an impressive 48.55% in FY25.

- This outward momentum is heavily supported by the ₹25,060 crore Export Promotion Mission and the recent ₹20,000 crore collateral-free credit guarantee scheme specifically for exporters.

- Grassroots Employment and Socio-Economic Inclusion: Small-scale industries are the ultimate democratizers of wealth, capable of absorbing massive demographic dividends by creating localized livelihoods outside saturated urban megacities.

- By empowering first-generation entrepreneurs and marginalized communities, they function as a structural shock absorber against extreme poverty and rural unemployment.

- The sector officially employs over 32.82 crore individuals, cementing its status as the nation's second-largest employer immediately following agriculture.

- Digital Formalization via Open Networks: The mass adoption of digital public infrastructure is dismantling traditional entry barriers, allowing micro-enterprises to bypass monopolistic e-commerce aggregators and directly access national consumer bases.

- This rapid digital formalization inherently lowers transaction costs, expands market discovery, and transitions informal vendors into the mainstream, trackable economy.

- The Open Network for Digital Commerce (ONDC), operating alongside the TEAM initiative, targets the seamless onboarding of MSMEs into formal supply chains.

- Also, for instance, Namma Yatri, a mobility app on ONDC, uses a "zero-commission" subscription model.

- Cash-Flow Lending and Fintech Integration: Transitioning away from rigid, collateral-heavy banking, the adoption of cash-flow-based appraisal systems is finally solving the historical "missing middle" funding gap for growing enterprises.

- By leveraging deep technological integrations, lenders can now accurately assess true business viability in real-time, preventing operational collapse due to delayed payments.

- The Account Aggregator (AA) framework and the Open Credit Enablement Network (OCEN) are the primary engines for this transition.

- The RBI's recently introduced Unified Lending Interface (ULI) that enables seamless sharing of financial and non-financial data from various sources to lenders, thereby improving the efficiency and accuracy of the credit underwriting process.

- Driving the Industrial Green Transition: Small enterprises are rapidly emerging as pivotal players in India’s net-zero strategy by embedding sustainable practices and energy-efficient technologies into localized supply chains.

- This grassroots green transition not only reduces carbon footprints but significantly enhances the eligibility of Indian suppliers participating in eco-conscious, compliant global markets.

- The MSE-GIFT scheme directly incentivizes this shift by providing concessional finance with a 2% interest subvention for adopting renewable technologies.

- Additionally, private banks are rolling out targeted collateral-free solar loans to help micro-manufacturers cut operational energy costs and align with Atmanirbhar Bharat's climate goals.

- Scaling Innovation in Deep Tech and Defense: Moving far beyond traditional low-value manufacturing, high-potential MSMEs are increasingly operating as agile innovators supplying critical sub-assemblies for strategic sectors like aerospace and defense.

- This upward technological mobility reduces foreign import dependencies, fosters deep-tech domestic R&D, and establishes a highly resilient sovereign industrial base.

- The Union Budget 2026-27 explicitly addresses this scale-up by a dedicated ₹10,000 crore SME Growth Fund, to create future Champions, incentivizing enterprises based on select criteria.

- Furthermore, the Self-Reliant India (SRI) Fund has successfully injected ₹15,442 crore in equity funding into 682 high-growth MSMEs to sustain their risk capital needs.

- Revitalizing the Artisan Economy: Targeted interventions are systematically modernizing India's traditional artisan economy, transforming heritage craftsmanship into scalable, bankable, and digitally connected micro-businesses.

- By formalizing this unorganized segment, the government ensures that master craftsmen receive equitable market value, modern skill upgrades, and direct integration into the formal banking system.

- The PM Vishwakarma Scheme exemplifies this shift, having successfully registered 30 lakh beneficiaries and fully trained 23.09 lakh artisans by late 2025.

- In 2025 alone, ₹2,257 crore was sanctioned to 2.62 lakh craftspeople in the form of collateral-free loans, alongside massive digital enablement drives.

What are the Key Challenges Faced by MSMEs in India?

- The Formal Credit Chasm: Traditional collateral-based lending models persistently exclude micro-enterprises from formal banking, stifling their fundamental growth potential.

- This friction forces them toward expensive, unregulated informal credit markets that severely erode their already thin operational margins.

- According to a 2025 SIDBI-Crisil report, India currently faces a massive ₹30 lakh crore MSME credit gap across the ecosystem.

- This deficit disproportionately affects the 35% of small businesses that remain entirely unregistered and algorithmically invisible to formal government schemes.

- Epidemic of Delayed Payments: The systemic failure of large corporate buyers and public entities to honor timely payment cycles severely paralyzes the operational working capital of vulnerable small suppliers.

- Without predictable liquidity, these enterprises cannot sustainably reinvest in raw materials, wage distributions, or technological upgrades.

- A March 2024 report highlighted that ₹20,413 crore was locked in 82,215 pending delayed payment applications and cases filed by MSEs on the Samadhaan Portal, a figure that may have risen further since then.

- Furthermore, April 2026 industry reports indicate payment cycles have drastically stretched from an average of 30 days to over 120 days due to broader market volatility.

- Geopolitical Supply Chain Shocks: Heightened global volatility and localized geopolitical conflicts directly disrupt export-oriented MSMEs through unprecedented spikes in international shipping costs.

- These unpredictable supply chain bottlenecks completely dismantle projected delivery timelines, leading to severe order cancellations and lost international contracts.

- Following the early 2026 West Asia conflict escalations, ocean freight costs for some MSMEs surged drastically from $300 to over $8,500 on specific routes.

- Consequently, the government was forced to launch the RELIEF scheme in March 2026 to partially reimburse MSMEs (eligible non-ECGC-insured MSME exporters) facing up to 50% logistical cost escalations.

- The Equity Capital Deficit: A historical over-reliance on traditional debt-based financing inherently limits the ability of high-potential MSMEs to scale into globally competitive, deep-tech entities.

- A March 2026 Parliamentary Committee report formally flagged that six out of eight recent MSME budget announcements still remain un-operationalized, bottlenecking actual growth.

- To address this structural flaw, the 2026–27 Union Budget made a strong shift toward equity financing by introducing a mandatory ₹10,000 crore SME Growth Fund, however, its effective implementation remains a key concern.

- Asymmetric Compliance Friction: Despite ongoing national decriminalization efforts, the sheer complexity of local bureaucratic compliance and tax filings continues to impose disproportionate administrative costs on resource-constrained micro-businesses.

- Many localized provincial enterprises simply lack the specialized legal bandwidth to navigate these overlapping central and state-level regulatory frameworks without incurring heavy consultancy fees.

- A TeamLease RegTech report reveals Indian manufacturing MSMEs face hefty compliance costs, reaching Rs 13-17 lakh annually,

- While the government successfully simplified over 47,000 regulatory compliances with 2025 Jan Vishwas amendments, a severe awareness gap persists at the grassroots level.

- The Persistent Digital Lending Divide: Although grassroots digital payment adoption has reached peak saturation, the critical transition from mere transaction processing to actually securing algorithm-driven digital credit remains deeply sluggish.

- A fundamental mismatch in digital financial literacy prevents these enterprises from converting their electronic transaction footprints into tangible, cash-flow-based banking appraisals.

- Recent 2025 financial surveys indicate that while over 90% of Indian MSMEs seamlessly accept digital payments, yet only a marginal 18% have successfully availed digital loans and just 13% actively use digital marketing or e-commerce to reach customers.

- The RBI is actively combating this barrier through the Unified Lending Interface (ULI), yet mass adoption is still severely constrained by infrastructural awareness.

- Gender Disparity in Financial Access: Systemic societal biases and a distinct lack of formalized collateral or property ownership inherently penalize women entrepreneurs operating in the manufacturing and service sectors.

- This deeply entrenched financial disparity significantly restricts their ability to secure adequate institutional backing, forcing a much higher dependency on exploitative informal credit networks.

- Although 26.2% of proprietary MSMEs are now women-led, a notable sign of social progress, these businesses remain financially disadvantaged.

- The credit offtake for women-owned MSMEs stands at 76%, compared to 84% for men. Worse, they face a higher dependency on informal credit and have the highest addressable credit gap at 35%.

What Measures are Required to Further Strengthen India’s MSMEs Sector?

- Shift to Algorithmic Cash-Flow Lending: Financial institutions must pivot from asset-heavy collateral requirements to data-driven cash-flow lending by leveraging the Unified Lending Interface (ULI) and GST aggregates.

- This allows for real-time risk assessment based on actual sales velocity and digital footprints rather than stagnant physical security, unlocking credit for "asset-light" service and tech-based micro-units.

- By institutionalizing algorithmic credit scoring, banks can provide frictionless, pre-approved working capital lines that expand automatically as the business scales its turnover.

- Mandatory TReDS Onboarding for Tier-II/III Suppliers: To solve the liquidity crisis, the government should enforce mandatory participation in the Trade Receivables Discounting System (TReDS) for all companies above a specific turnover threshold, extending deep into the supply chain. Integrating this with the GSTN portal would allow for "Automatic Invoice Factoring," where an uploaded invoice is instantly converted into a tradable asset for financiers.

- This creates a self-sustaining liquidity loop that eliminates the "waiting period" for small suppliers, effectively insulating them from the credit cycles of larger buyers.

- Creation of Cluster-Specific "Common Facility Centres" (CFCs): Establishing localized, state-of-the-art Common Facility Centres through Public-Private Partnerships (PPP) can provide MSMEs with access to "Industry 4.0" infrastructure, such as 3D printing, advanced CNC machining, and testing labs.

- This "Infrastructure-as-a-Service" model allows micro-units to achieve high-precision manufacturing standards without the prohibitive capital expenditure of owning heavy machinery.

- It fosters a collaborative ecosystem where small units can aggregate orders to meet global quality benchmarks collectively.

- Implementation of "Green-Channel" Regulatory Compliance: A "Regulatory Sandbox" or "Green Channel" should be instituted for MSMEs, offering a three-year moratorium on non-critical compliance inspections for newly formalized units.

- Replacing complex, multi-layered filings with a Unified Annual Compliance Return would drastically reduce the "Compliance Tax" in terms of time and administrative costs.

- This creates a "compliance-lite" environment that encourages informal vendors to register under the Udyam portal without the fear of immediate bureaucratic harassment.

- Integration into Global Value Chains (GVCs) via ONDC: Leveraging the Open Network for Digital Commerce (ONDC) to create a specialized "Export Module" can bypass traditional intermediary monopolies and connect rural artisans directly to international B2B markets.

- This digital bridge should include integrated logistics-as-a-service and automated customs clearing, allowing a micro-enterprise to ship globally with the same ease as local delivery.

- By democratizing market access, ONDC can transform hyper-local products into global brands, ensuring equitable value distribution for the producer.

- Institutionalizing "Zero Defect Zero Effect" (ZED) Incentives: To enhance global competitiveness, the ZED Certification should be linked to preferential procurement and interest subvention schemes, rewarding units that adopt sustainable, high-quality manufacturing.

- Implementing "Green Transition Credits" can help MSMEs fund the shift to renewable energy sources and circular waste management systems, aligning them with the EU's Carbon Border Adjustment Mechanism (CBAM).

- This ensures that Indian MSMEs are not priced out of future eco-conscious global markets due to their carbon footprint.

- Equity-Linked "Patient Capital" Instruments: Beyond debt, the state must catalyze the flow of "Patient Equity Capital" through specialized SIDBI-led Fund-of-Funds that target the "Missing Middle" enterprises ready for expansion.

- Introducing Revenue-Based Financing (RBF) models (where repayments are a percentage of monthly revenue) offers a flexible alternative to rigid EMIs, particularly for seasonal or high-growth startups.

- This provides the necessary "risk-cushion" for MSMEs to invest in long-term R&D and intellectual property creation without the immediate pressure of debt servicing.

- Hyper-Localized Skill Upgradation via "Hub-and-Spoke" Labs: A decentralized "Hub-and-Spoke" vocational training model should be embedded within industrial clusters to provide just-in-time skill upgrades in emerging fields like AI, robotics, and sustainable packaging.

- By partnering with local polytechnics and industry associations, these labs can ensure the workforce is trained on the specific technologies used by the cluster's lead firms.

- This micro-credentialing approach addresses the acute "Skilling Gap," ensuring that as MSMEs modernize their machinery, they have an immediate supply of locally available, tech-savvy labor.

Conclusion:

The transformation of India's MSME sector from a state of fragmented resilience to globally competitive scale is the linchpin for achieving the "Viksit Bharat@2047" vision. By addressing structural bottlenecks like the "missing middle" through algorithmic lending and mandatory digital payment ecosystems, India can unlock the latent potential of its grassroots entrepreneurs. Ultimately, a synergistic approach involving proactive policy, digital public infrastructure, and MSME-led green innovation will ensure that these enterprises do not just survive but lead India's charge in the global value chain.

|

Drishti Mains Question "The MSME sector in India suffers from a 'hollowed-out middle' that prevents small firms from scaling into global champions." Critically analyze the structural and financial barriers contributing to this phenomenon. |

FAQs

1. What is the 'Missing Middle' in the MSME sector?

It refers to the lack of medium-sized enterprises; India has millions of micro-firms but very few scale up to the "medium" category due to credit and regulatory hurdles.

2. How does the Unified Lending Interface (ULI) help MSMEs?

It allows lenders to use digital footprints (GST/UPI data) for instant, collateral-free credit instead of traditional property-based loans.

3. What is the TReDS platform?

It is an online mechanism for discounting trade receivables, ensuring MSMEs get paid immediately by banks instead of waiting for large buyers.

4. Why is the 'ZED' certification important?

It stands for Zero Defect Zero Effect, encouraging MSMEs to produce high-quality goods with minimal environmental impact for global competitiveness.

5.What is the new MSME classification (2026)?

Micro (up to ₹1cr investment/₹5cr turnover), Small (up to ₹10cr/₹50cr), and Medium (up to ₹50cr/₹250cr).

UPSC Civil Services Examination, Previous Year Question:(PYQ)

Prelims:

Q. Consider the following statements with reference to India : (2023)

- According to the Micro, Small and Medium Enterprises Development (MSMED) Act, 2006, the ‘medium enterprises’ are those with investments in plant and machinery between 15 crore and 25 crore.

- All bank loans to the Micro, Small and Medium Enterprises qualify under the priority sector.

Which of the statements given above is/are correct?

(a) 1 only

(b) 2 only

(c) Both 1 and 2

(d) Neither 1 nor 2

Ans: (b)

Mains

Q. Faster economic growth requires increased share of the manufacturing sector in GDP, particularly of MSMEs. Comment on the present policies of the Government in this regard. (2023)