Agriculture

Farm Loan Waiver

- 11 Jun 2020

- 7 min read

This article is based on “Loan waivers are a double-edged sword” which was published in The Hindu Business line on 09/06/2020. It examines the policy of farm loan waivers and its impacts on farmers as well as the banking sector.

Recently, a case was filed in the Supreme Court seeking a directive to the Central government and the Reserve Bank of India (RBI) to waive interest on loans during the period of moratorium. Further, there have been demands from the farming community for farm loan waivers in many states.

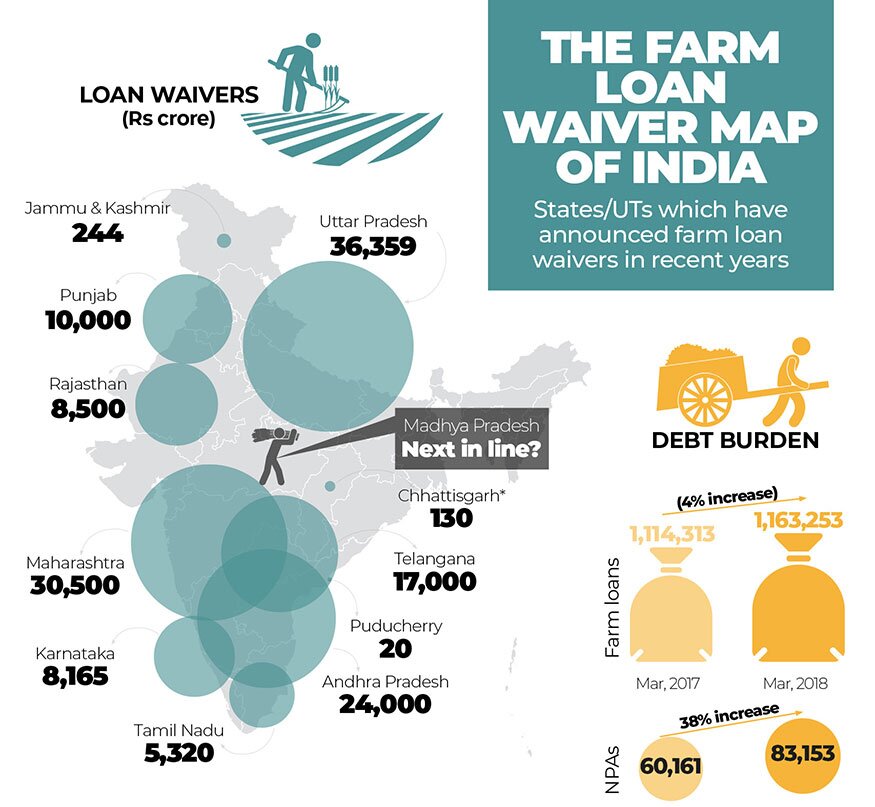

Loan waivers, originally intended for a one-time settlement. However, the past two decades have seen such schemes announced with increasing regularity, signalling the chronic distress of the agricultural sector in India.

Though these demands seem more legitimate in the wake of the loss of livelihood due to lockdown amid Covid-19, yet such loan waivers may prove detrimental to the banking system and credit culture.

History of Farm Loan Waiver

- The first recorded instance of granting loans to peasants in medieval India dates back to the regime of Muhammad-bin-Tughluq (1325-51) so as to ameliorate the distress suffered by villagers.

- However, faced with rebellion and famine, these loans were written off by Firoz Shah Tughluq, the subsequent ruler.

- There have only been two nationwide loan waiver programmes in India after Independence: in 1990 and 2008.

- The first nationwide farm-loan waiver in independent India was implemented in 1990 by the VP Singh-led government. It cost the exchequer Rs 10,000 crore.

- In 2008, the Agricultural Debt Waiver and Debt Relief Scheme, implemented by the UPA government, involved an outgo of Rs 71,680 crore.

- Since then, there has been a wave of such schemes by different State governments.

Rationale for Loan Waiver

- More than 85% of small and marginal farmers in India possess less than 1-2 hectares of holdings and lack basic inputs for farming.

- In this context, the credit is a critical resource to farming households for carrying out crop production and meeting consumption & daily-life expenses.

- However, in India, the crop yield and production are highly dependent on monsoon.

- Farmers invest heavily in crops by taking loans. If the crop fails due to lack of rains or insufficient market demand, farmers will get trapped in debt. Due to this, there has been an increase in farmer suicides.

- Thereby, waiving farm loans address this humanitarian crisis.

Issues Related to Loan Waivers

- Reputational Consequences: Loan waiver schemes will disrupt credit discipline as farm loan waivers may act as a temporary solution and can prove to be a moral hazard in future.

- This is because those farmers who can afford to pay their loans might not pay it expecting a waiver.

- Free Rider Problem: Some farmers may take loans even if there is no need, in the hope of the next loan waiver scheme. This will impact the farmers who are genuinely in need of loans.

- Decline in Formal Access to Credit: After the implementation of debt waiver schemes and subsequent losses to the banking industry, banks will be reluctant to lend further to the farm sector.

- This leads to a rise in farmer’s dependence on informal sector lenders.

- In other words, waivers lead to the shrinkage of a farmer’s future access to formal sector credit and thereby compel them to depend on varying informal sources (like local moneylenders, Sahookaar) for credit.

- Impact on Banking Sector: A report by the Indian Council for Research on International Economic Relations stated that the 2008 farm-loan waiver led to three-fold increase in non-performing assets of commercial banks between 2009–2010 and 2012–2013.

- This further affects credit-deposit ratio and risk-weighted capital adequacy ratio, return on assets and economic value of equity of banks.

- This downgrades the ratings of banks in particular and destabilizes the functioning of the credit market in general.

- Against the Interests of Depositors: Banks receive money from the depositors and lend money to borrowers under different contracts and agreements.

- Thus, the loss to the bank, due to loan waivers, is directly or indirectly against the interests of the depositors.

- Moreover, banks being custodians of depositors’ money, need to be guided primarily by the protection of depositors’ interests.

Conclusion

In the present situation, farm loan waivers act only as a temporary solution to the problems of farmers and it will not make them free from issues like decreasing farm income, debt trap or crop failures.

In this context, there is a need for creative engagement through which the surplus workers in the farming sector can be taken away to more productive sectors and farming can be made more profitable and sustainable for all the people.

|

Drishti Mains Question “Farm loan waivers are the case of good politics but bad economics.” In light of this statement critically analyse the policy of farm loan waiver. |

This editorial is based on “A three-fold test for new legislations” which was published in The Hindustan Times on June 9th, 2020. Now watch this on our Youtube channel.