Important Facts For Prelims

Supreme Court Verdict on DTAA

- 23 Jan 2026

- 11 min read

Why in News?

The Supreme Court (SC) has ruled that Tiger Global’s USD 1.6-billion stake sale in Flipkart to Walmart (2018) is taxable in India, denying the benefits of the India–Mauritius Double Taxation Avoidance Agreement (DTAA) and enforcing the General Anti-Avoidance Rule (GAAR).

What are the Key Facts of the Tiger Global Case?

- Key Legal Dispute: Tiger Global, a prominent venture capital investor, sold its Flipkart stake for USD 1.6 billion to Walmart in 2018, leading to a legal tussle with Indian tax authorities over capital gains tax liability.

- India's SC overturned the August 2024 Delhi High Court (HC) judgment, which had quashed an Authority for Advance Rulings (AAR) order denying DTAA benefits.

- AAR is a quasi-judicial body that provides binding rulings on specific tax questions, offering taxpayers clarity before transactions to reduce uncertainty and potential litigation.

- India's SC overturned the August 2024 Delhi High Court (HC) judgment, which had quashed an Authority for Advance Rulings (AAR) order denying DTAA benefits.

- Supreme Court’s Legal Reasoning: The SC held that DTAA benefits cannot be claimed mechanically and rejected reliance on Tax Residency Certificates (TRCs) alone, as the India-Mauritius DTAA applies only where assets are directly owned by a Mauritian entity. It emphasized economic substance, control, and management, concluding the entities’ “head and brain” lay outside Mauritius, particularly in the USA.

- A TRC is issued by a country’s tax authority to confirm an entity’s tax residency for a specific period. It is essential for claiming DTAA benefits, such as avoiding double taxation.

- Role of AAR and High Court: The AAR’s 2020 order denied DTAA grandfathering benefits, ruling the investment structure was prima facie for tax avoidance, a finding later struck down by the Delhi HC as arbitrary. The SC reversed the Delhi HC, restoring the AAR’s substance-over-form approach.

- Grandfathering in tax is a legal provision that protects existing investments from new tax laws by allowing them to be taxed under older, more favorable rules. Under the India–Mauritius DTAA, it protected capital gains from investments made before 1st April, 2017, which were taxed only in Mauritius—that is, 0% tax in India—even after the treaty was amended.

- Implications: The ruling signals a major shift, ending automatic DTAA claims based solely on residency certificates. Investors must demonstrate genuine economic substance, autonomous decision-making, and commercial rationale for DTAA benefits.

- Investors face elevated tax litigation risk, with tools like tax insurance expected to become scarcer and costlier.

- The decision arrives amid a broader slowdown in Indian startup funding, which fell to USD 10.5 billion in 2025, a 17% decline from 2024, with notable drops in seed-stage (down 30%) and late-stage funding (down 26%).

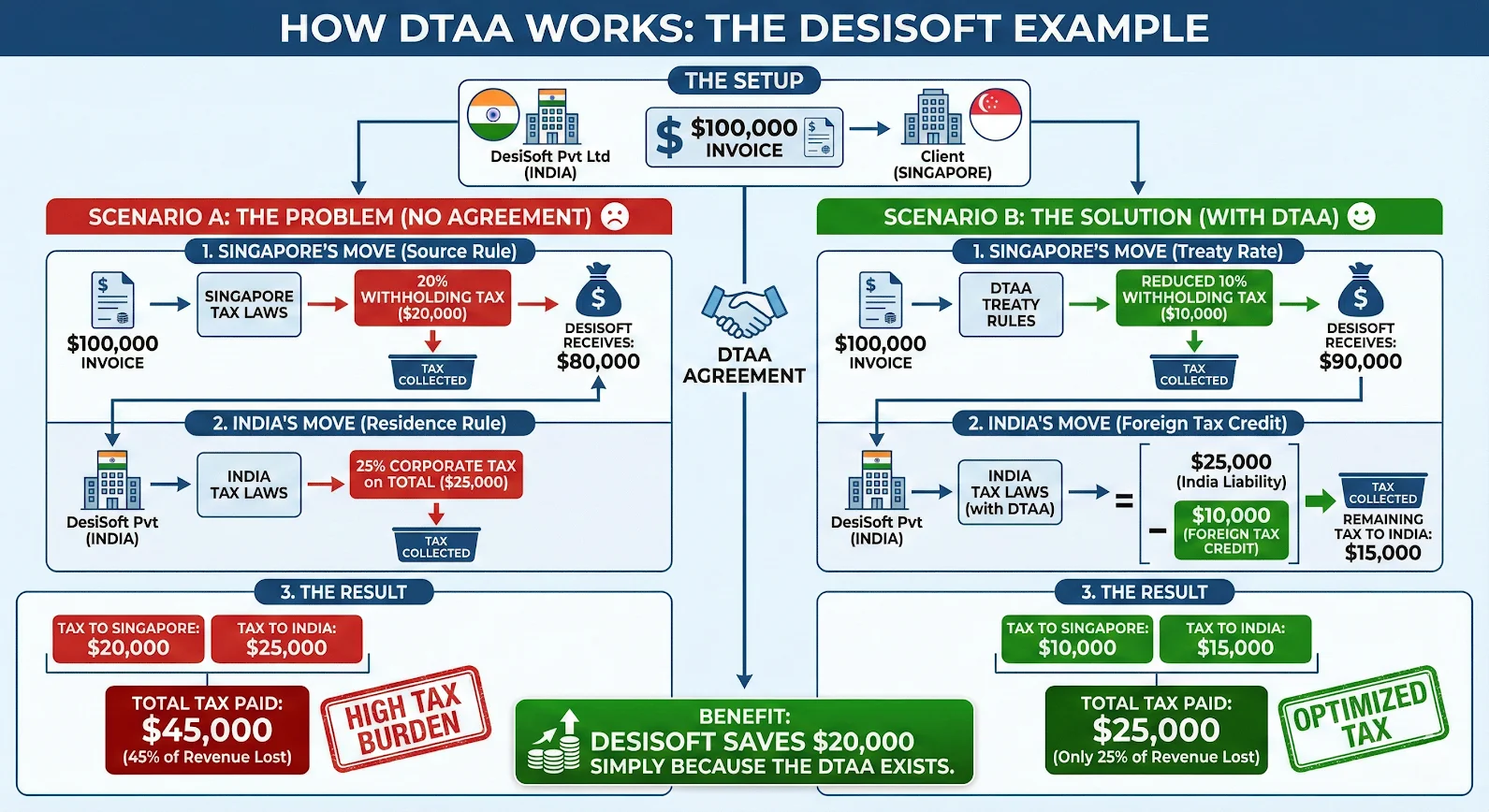

Double Taxation Avoidance Agreement (DTAA)

- About: A DTAA is a bilateral (or occasionally multilateral) agreement entered into between two sovereign countries to prevent or mitigate double taxation on income or capital gains arising from cross-border activities, where an individual or entity could be taxed both in their country of residence and the country where the income is sourced.

- Key Relief Mechanisms: DTAAs provide relief primarily through two methods: the Exemption Method (income taxed in only one country) and the Credit Method (resident country grants a credit for taxes paid in the source country).

- Indian Context & Procedure: India has an extensive network of over 90 DTAAs. To claim benefits, a taxpayer must furnish a TRC from their country of residence, along with other required declarations.

- DTAA Misuse and Redressal: India has faced DTAA misuse through treaty shopping, round-tripping, and shell companies in jurisdictions like Mauritius, Singapore, and Cyprus.

- To counter this, the government amended key DTAA treaties, introducing source-based taxation and Limitation of Benefits (LOB) clauses to require substantive economic presence.

- Domestically, the GAAR was implemented in 2017 to deny treaty benefits for arrangements primarily aimed at tax avoidance.

General Anti-Avoidance Rule (GAAR)

- About: GAAR is an anti-tax evasion measure that empowers Indian authorities to deny tax benefits for arrangements whose primary purpose is tax avoidance, prioritizing the economic substance of transactions over their legal form.

- Objective: India's GAAR came into effect on 1st April 2017, with the objective of curbing aggressive tax planning and treaty shopping.

- Triggering Conditions: GAAR applies where the main purpose is to obtain a tax benefit and meets any one test:

- Commercial Substance Test: Absence of real operations, personnel, or decision-making authority

- Rights and Obligations Test: Artificial creation of rights or obligations to secure tax benefits

- Misuse or Abuse of Law: Exploitation of loopholes in treaties or domestic law

- Non-arm’s-length test: Deviation from normal commercial practices.

- Consequences of Invocation: If applied, authorities can deny treaty benefits (like capital gains exemptions), disregard intermediary entities, recharacterize transactions, reallocate income to India, and levy tax, interest, and penalties.

- Supremacy over Treaties: A critical feature is that under Indian law, GAAR overrides tax treaties, meaning treaty benefits can be denied if GAAR is triggered—a position now firmly upheld by the Supreme Court.

Frequently Asked Questions (FAQs)

1. What did the Supreme Court decide in the Tiger Global–Flipkart case?

The SC held that Tiger Global’s USD 1.6-billion Flipkart stake sale (2018) is taxable in India, denying India–Mauritius DTAA benefits.

2. What is ‘grandfathering’ under the India–Mauritius DTAA?

It protected capital gains from investments made before April 1, 2017, taxing them only in Mauritius (0% in India), subject to anti-abuse scrutiny.

3. How does GAAR affect tax treaties in India?

GAAR overrides tax treaties, allowing authorities to deny DTAA benefits if an arrangement’s primary purpose is tax avoidance.

UPSC Civil Services Examination, Previous Year Questions (PYQs)

Q. Which one of the following effects of creation of black money in India has been the main cause of worry to the Government of India? (2021)

(a) Diversion of resources to the purchase of real estate and investment in luxury housing.

(b) Investment in unproductive activities and purchase of precious stones, jewellery, gold, etc.

(c) Large donations to political parties and growth of regionalism.

(d) Loss of revenue to the State Exchequer due to tax evasion.

Ans: (d)

Q. With reference to India’s decision to levy an equalization tax of 6% on online advertisement services offered by non-resident entities, which of the following statements is/are correct? (2018)

- It is introduced as a part of the Income Tax Act.

- Non-resident entities that offer advertisement services in India can claim a tax credit in their home country under the “Double Taxation Avoidance Agreements”.

Select the correct answer using the code given below:

(a) 1 only

(b) 2 only

(c) Both 1 and 2

(d) Neither 1 nor 2

Ans: (d)