Indian Economy

Stress in Microfinance

- 12 May 2025

- 11 min read

For Prelims: Microfinance institutions, Non-performing assets, Reserve Bank of India, Self Employed Women's Association, National Bank for Agriculture and Rural Development

For Mains: Challenges and reforms in the Microfinance Sector, Financial Inclusion and its role in rural development

Why in News?

India’s microfinance institutions (MFIs) are facing a major crisis as gross non-performing assets (NPAs) surged to 16% by March 2025, nearly doubling from 8.8% in 2024. As defaults rise, lenders are pulling back, and regulatory interventions are raising concerns about the sector’s sustainability.

What are the Factors that led to Rise in NPAs in MFIs?

- Cyclical Nature of Microfinance: MFIs have traditionally followed a cyclical pattern, with crises occurring every 3-5 years, and the current situation fits this historical trend.

- However, deeper structural issues like rising loan defaults driven by economic slowdown (GDP at a 4-year low of 6.4% in 2024–25), natural disasters (heatwaves, floods), and election-related disruptions, impacted borrowers’ repayment capacity.

- Over-Leveraging of Borrowers: In an effort to expand rapidly, MFIs have increasingly sanctioned loans to borrowers with already high levels of debt. This has led to an over-leveraged customer base, unable to keep up with repayments.

- Many MFIs have been lenient in evaluating the borrowers' repayment capacity, focusing more on volume rather than assessing the financial health of individual borrowers.

- Borrowers, particularly in rural areas, often take loans from multiple MFIs and other sources, compounding their debt burden and heightening the likelihood of defaults.

- The rise in credit card outstanding, from Rs 2.30 lakh crore in 2023 to Rs 2.71 lakh crore in 2024, highlights a broader trend of rising consumer debt.

- Weakening of the Joint Liability Group (JLG) Model: The JLG model, central to microfinance operations, relies on social pressure and collective responsibility for loan repayment.

- However, it is becoming less effective due to changing borrower profiles, weakened group cohesion, and rising individual defaults.

- Rising Regulatory Pressure: The Reserve Bank of India (RBI) has imposed stricter lending norms and restrictions, such as curbing aggressive lending practices. While these actions aim to stabilize the sector, they have also led to short-term liquidity crunches for MFIs.

- State governments have started passing laws to curb coercive recovery methods by microfinance lenders, including harsh penalties for non-compliance.

- For instance, the Tamil Nadu Assembly passed the Money Lending Entities (Prevention of Coercive Actions) Act, while Karnataka proposed severe punishments for lenders causing undue hardship to borrowers.

- Additionally, Campaigns like Karja Mukti Abhiyan (loan waiver schemes) have weakened the repayment culture, as borrowers anticipate government debt forgiveness, leading to higher defaults.

- State governments have started passing laws to curb coercive recovery methods by microfinance lenders, including harsh penalties for non-compliance.

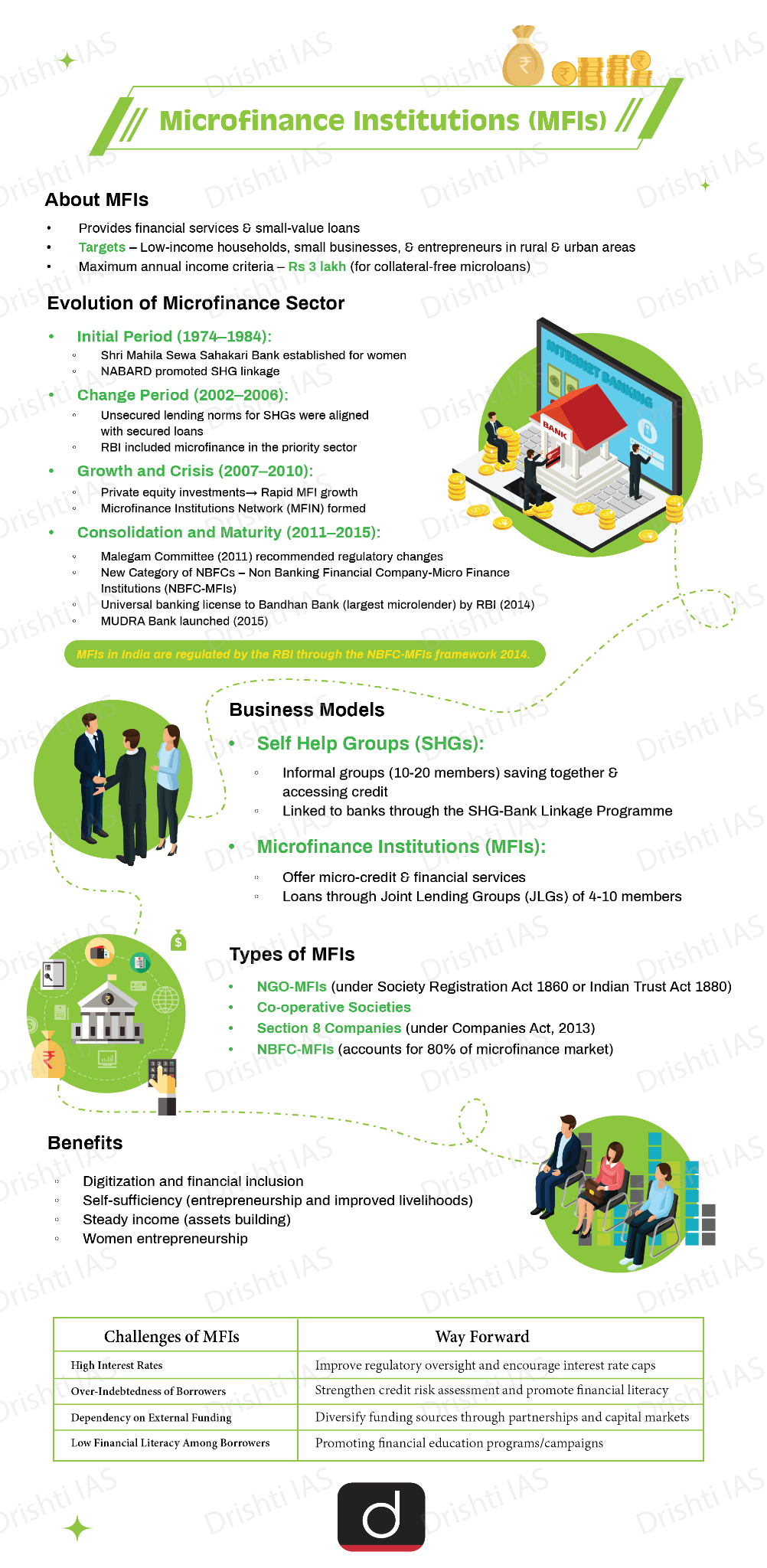

What is Microfinance?

- About: Microfinance, also known as microcredit, refers to the provision of financial services such as small loans, savings accounts, insurance, and fund transfers to underserved populations, particularly in rural and remote areas.

- It is aimed at empowering marginalized and low-income communities, particularly women, to become financially self-sufficient and contribute to socio-economic development.

- Importance of Microfinance: It is a tool for reducing poverty by providing access to financial resources for income-generating activities.

- Microfinance supports small-scale businesses, boosting local economies and employment, especially in rural areas.

- Over the past three decades, it has improved living standards for nearly 100 million rural households in India.

- Microfinance promotes gender equality by empowering women financially.

- In 2022-23, India’s microfinance sector added 80 lakh new women clients, reaching a total of 6.64 crore women with 12.96 crore active loans by 2023, as per the India Microfinance Review FY23 report.

- Microfinance supports small-scale businesses, boosting local economies and employment, especially in rural areas.

- Microfinance in India: Microfinance in India began with the establishment of the Self Employed Women's Association (SEWA) Bank in 1974 in Gujarat, which aimed to provide financial services to low-income women excluded from formal banking.

- In 1992, National Bank for Agriculture and Rural Development (NABARD) introduced the Self-Help Group (SHG)-Bank Linkage Programme, enhancing small-scale savings and access to credit for women.

- In 2011, the RBI recognized microfinance as a priority sector, granting policy support to MFIs.

- However, the Andhra Pradesh microfinance crisis in 2010, caused by aggressive lending practices, led to increased scrutiny and the formation of the Malegam Committee (2010) to regulate Non-Banking Financial Company-Microfinance Institutions (NBFC-MFIs).

- In 2015, the launch of MUDRA Bank under the Pradhan Mantri Mudra Yojana (PMMY) further strengthened the microfinance ecosystem by providing credit to small, non-corporate enterprises.

- Current Status Microfinance in India: MFIs currently operate in 28 states, 8 Union Territories and 730 districts in India.

- The microfinance industry grew 16% in FY 2023-24, compared to 21% in 2022-23. By March 2024, the sector's combined portfolio reached Rs 4.08 lakh crore.

- As of 2024, the top five states with the highest loan outstanding in the microfinance sector are Bihar, Tamil Nadu, Uttar Pradesh, Karnataka, and West Bengal. These states collectively account for approximately 58% of the industry's total portfolio.

How Can Microfinance Institutions Address the Crisis and Ensure Long-Term Sustainability?

- Adopt Holistic Triad Model: MFIs should adopt holistic models like Basix's Triad Model, which integrates livelihood promotion, financial services, and institutional development.

- It focuses on providing skills training, market linkages, and insurance, key elements missing in credit-only models.

- The Triad Model ensures microloans are used for income-generating activities, not for non-productive purposes, which can help prevent over-indebtedness and ensure financial progress.

- Improve Credit Rating: Improve credit scoring systems by prioritizing outcomes such as economic stability and household income improvement, rather than just repayment rates and portfolio growth.

- This shift will ensure that financial institutions not only remain financially sound but also contribute meaningfully to borrowers' lives.

- Shift Towards Individual Credit Appraisals: Moving away from the group-based JLG model and introducing individual credit assessments could reduce NPAs.

- Use of Technology for Risk Mitigation: Adoption of real-time data tracking, KYC (Know Your Customer) verification, and secure loan management platforms such as end-to-end Loan Origination Systems (LOS), Loan Management Systems (LMS) through open APIs will significantly improve service delivery.

- The adoption of big data analytics can enhance risk assessment and improve credit underwriting, potentially reducing defaults.

- Revamping Collection Practices: While legal measures to prevent coercive practices are necessary, MFIs must also focus on improving customer relationships and collections strategies.

- Engaging borrowers through communication and support services—rather than intimidation, can build trust and improve repayment rates.

- Providing flexible loan products, such as income-based repayments, may help borrowers manage their repayments better.

- Promoting Financial Literacy: Financial literacy programs for borrowers can help them understand the consequences of non-repayment and improve their ability to manage loans.

Conclusion

The rise in NPAs in the microfinance sector signals a challenging but cyclical phase driven by internal missteps rather than systemic shocks. With major lenders like SBI continuing to back the sector and pushing for better governance, the sector's resilience will depend on self-correction, regulatory discipline, and continued institutional support. The road to recovery may be long but remains achievable with collective effort.

|

Drishti Mains Question: “The surge in non-performing assets among Microfinance Institutions reflects deeper structural issues in India’s rural credit delivery model.” Critically examine. |

UPSC Civil Services Examination Previous Year Questions (PYQ)

Prelims:

Q. Microfinance is the provision of financial services to people of low-income groups. This includes both the consumers and the self-employed. The service/ services rendered under microfinance is/are (2011)

- Credit facilities

- Savings facilities

- Insurance facilities

- Fund Transfer facilities

Select the correct answer using the codes given below the lists:

(a) 1 only

(b) 1 and 4 only

(c) 2 and 3 only

(d) 1, 2, 3 and 4

Ans: (d)

Mains:

Q. Can the vicious cycle of gender inequality, poverty and malnutrition be broken through microfinancing of women SHGs? Explain with examples. (2021)