International Relations

Shift in OPEC+ Production Strategy

- 31 May 2025

- 8 min read

For Prelims: Organization of the Petroleum Exporting Countries, K-shaped recovery, International Energy Agency, World Trade Organisation

For Mains: Global oil supply dynamics and OPEC+, India’s energy security and oil import dependency

Why in News?

The Organization of the Petroleum Exporting Countries (OPEC)+ group led by Saudi Arabia decided to increase oil production by 411,000 barrels per day (bpd). This marks the third consecutive month of production hikes, gradually reversing the voluntary output cuts initiated in 2023.

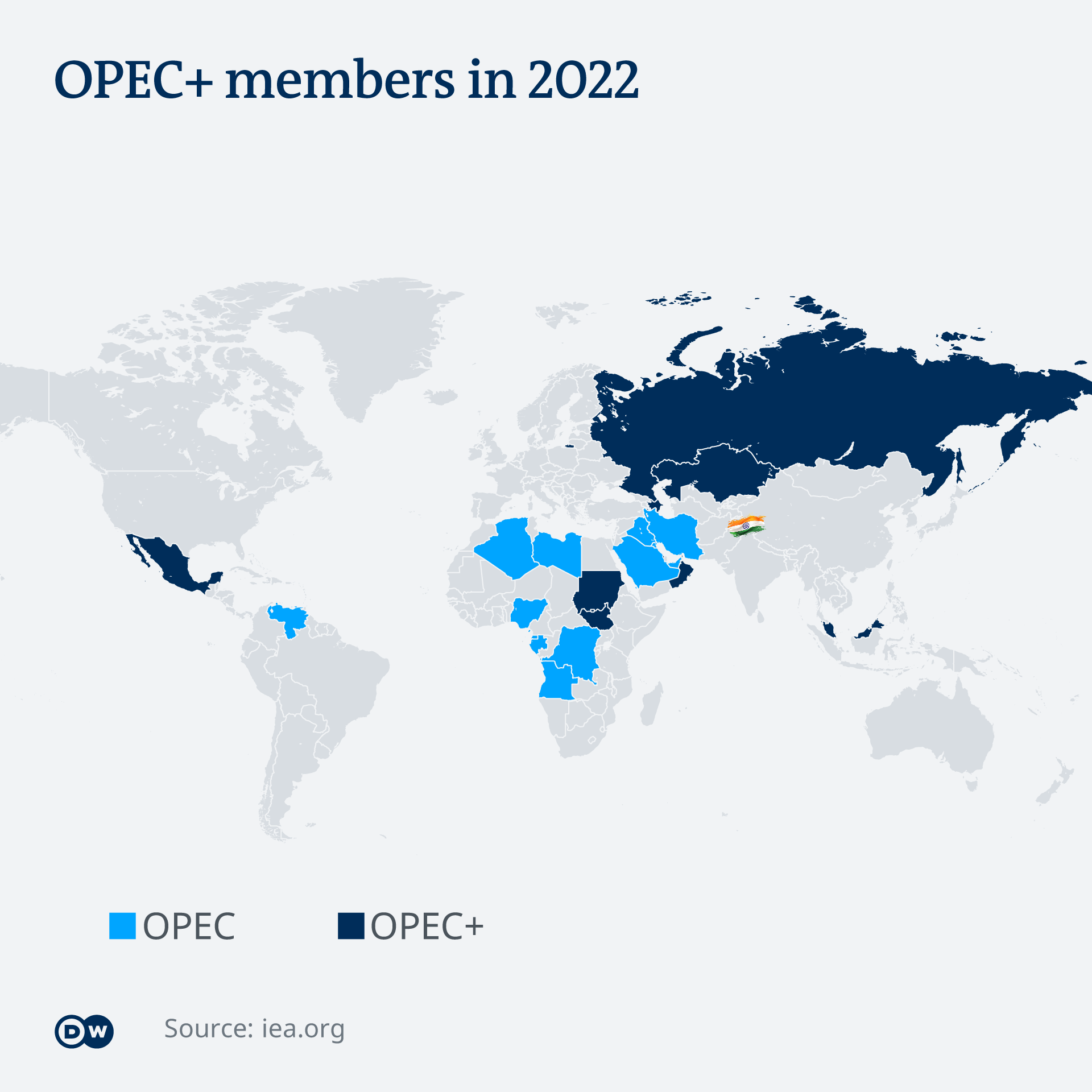

Organization of the Petroleum Exporting Countries

- The OPEC is a permanent intergovernmental organization founded at the Baghdad Conference, in 1960 by Iran, Iraq, Kuwait, Saudi Arabia, and Venezuela, headquartered in Vienna, Austria.

- OPEC currently has 12 members, including Algeria, Iran, Iraq, Kuwait, Libya, Nigeria, Saudi Arabia, UAE, and Venezuela.

- OPEC works to coordinate oil policies among member countries to ensure stable prices, steady supply to consumers, and fair returns for investors.

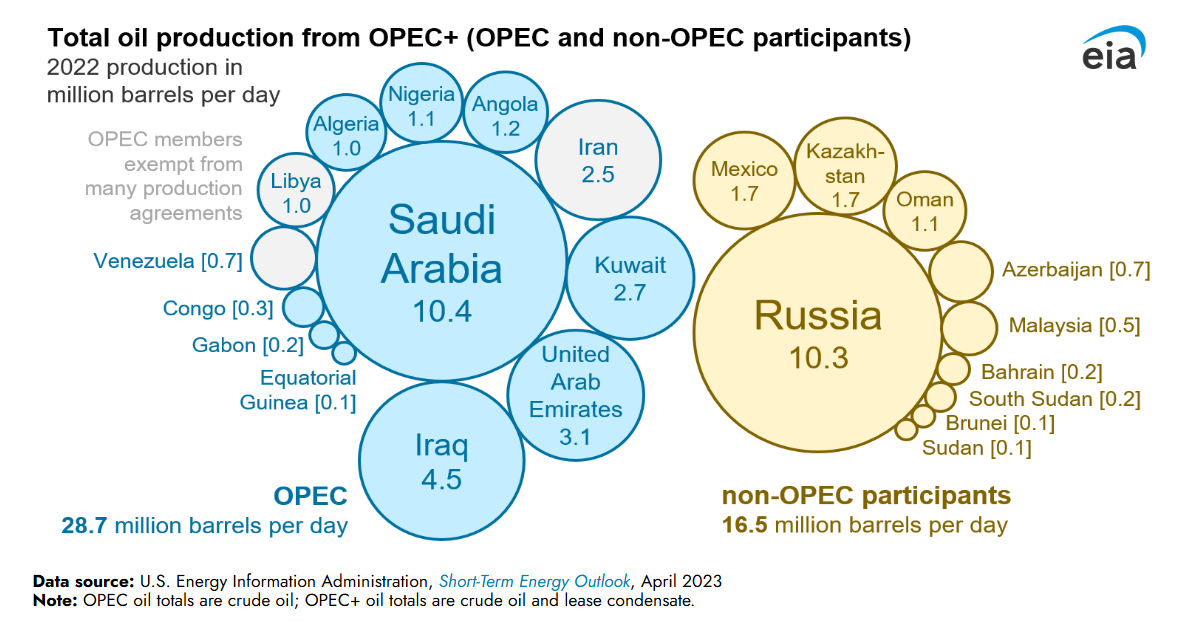

- OPEC nations produce about 30% of the world’s crude oil, hold 80% of proven reserves, and account for nearly half of global exports, with Saudi Arabia as the largest producer among the OPEC.

- OPEC+ was formed in 2016 as an alliance between OPEC and 10 other oil producers to address declining oil prices due to US shale oil growth.

- OPEC+ includes the OPEC members plus Azerbaijan, Bahrain, Brunei, Kazakhstan, Malaysia, Mexico, Oman, Russia, South Sudan, and Sudan.

- The OPEC and OPEC+ countries combined produce about 60% of global oil production.

What Factors Influenced the Rise in Oil Production by OPEC+?

- Weak Impact of Output Cuts: In 2023, eight OPEC+ members voluntarily cut oil production by 2.2 million barrels per day (bpd) to support falling prices.

- Despite these reductions, global oil prices continued to decline, indicating weak market response.

- Rise of Overproduction Within OPEC+: Countries like Kazakhstan, Iraq, UAE, and Nigeria produced more oil than their agreed limits. This concerned Saudi Arabia, which made the largest cuts of around 3 million bpd.

- Post-COVID Market Weakness: Post-pandemic recovery has been K-shaped, leading to weak and uneven oil demand. The oil market now has many freelance producers outside OPEC+, making it more complex.

- High investments have gone into expensive offshore and difficult fields that need to keep producing, even if profits are low, due to political and economic reasons.

- Big oil exporters like Russia, Iran, and Venezuela are limited by US sanctions.

- Non-OPEC+ producers like Brazil and Guyana are also ramping up production, adding to global oversupply.

- Shale producers in the US have returned stronger, making the market more competitive and less responsive to OPEC+ controls.

- Shift from Price Support to Market Share: With price stabilization efforts failing, Saudi Arabia revived its old strategy of chasing market share over price.

- Saudi Arabia is known as the “swing producer” due to its large spare oil production capacity and preference for stable, moderately high prices to maintain steady revenues.

- However, when other producers exceed their quotas, Saudi Arabia floods the market (as seen in 1985–86, 1998, 2014–16, and 2020) to pressure high-cost producers and reassert its leadership.

How is Global Oil Demand Evolving?

- Weakening Global Oil Demand: The International Energy Agency (IEA) expects global oil demand to grow only 0.73% in 2025.

- The “peak demand” theory (the idea that global oil demand will reach its highest point and then permanently decline) is gaining credibility, with indicators like a global economic slowdown, rising EV adoption, and stronger climate action.

- These trends, compounded by disruptions such as the US tariff war, have led to reduced global GDP (S&P Global forecasts global GDP growth of just 2.2% in 2025 and 2.4% in 2026 weakest since the 2008 crisis) and trade forecasts.

- As a result, oil demand may plateau, and prices may not rebound even if supply constraints ease.

- The “peak demand” theory (the idea that global oil demand will reach its highest point and then permanently decline) is gaining credibility, with indicators like a global economic slowdown, rising EV adoption, and stronger climate action.

- Trade Risks: World Trade Organisation (WTO) predicts a 0.2% annual decline in global trade in 2025. This may cause oil prices to remain subdued despite supply cuts, challenging traditional supply-demand price mechanisms.

- Sanctions and Supply-Side Constraints: Key oil producers like Russia, Iran, and Venezuela are under US sanctions, reducing their export capacity (a situation that may change if sanctions are lifted).

What are the Implications of Global Oil Price Volatility for India’s Economy?

- India’s Growing Oil Demand: India is the world’s 3rd-largest crude importer (after China and the US) with demand growth (~3.2% in 2024-25) nearly four times the global rate.

- India is expected to contribute nearly 25% of global crude demand growth in 2025 and become the primary demand driver until 2040.

- Short-Term Benefits: Lower crude prices can reduce India’s import bill, with every USD 1 drop in oil prices saving roughly USD 1.5 billion annually.

- Long-Term Risks: Lower oil revenues can weaken the economies of key Gulf trading partners, reducing bilateral trade, investments, and tourism.

- It could lead to possible job losses for over nine million Indian expatriates in the Gulf, threatening remittance inflows (approx USD 50 billion), which support India’s balance of payments.

- Tax revenues linked to oil and gas sectors also reduce, impacting government finances.

- Need for Diversification: India faces the strategic imperative to reduce hydrocarbon dependence and develop new growth drivers to mitigate risks from volatile oil markets.

|

Drishti Mains Question: OPEC+ has shifted its focus from price control to market share. Critically analyze how this change impacts global oil markets and India's energy security. |

UPSC Civil Services Examination, Previous Year Question (PYQ)

Prelims

Q. Other than Venezuela, which one among the following from South America is a member of OPEC? (2009)

(a) Argentina

(b) Bolivia

(c) Ecuador

(d) Brazil

Ans: (c)

Mains

Q. “Access to affordable, reliable, sustainable and modern energy is the sine qua non to achieve Sustainable Development Goals (SDGs)”.Comment on the progress made in India in this regard. (2018)