Indian Economy

Bad Bank

- 19 Jan 2021

- 6 min read

Why in News

Recently, the Reserve Bank of India (RBI) Governor has agreed to look at a proposal for creating a Bad Bank.

Key Points

- About:

- A bad bank conveys the impression that it will function as a bank but has bad assets to start with.

- Technically, a bad bank is an Asset Reconstruction Company (ARC) or an Asset Management Company (AMC) that takes over the bad loans of commercial banks, manages them and finally recovers the money over a period of time.

- The bad bank is not involved in lending and taking deposits, but helps commercial banks clean up their balance sheets and resolve bad loans.

- The takeover of bad loans is normally below the book value of the loan and the bad bank tries to recover as much as possible subsequently.

- US-based Mellon Bank created the first bad bank in 1988, after which the concept has been implemented in other countries including Sweden, Finland, France and Germany.

- The Troubled Asset Relief Programme (TARP) in the US.

- In Ireland, the National Asset Management Agency was established in 2009 to respond to the financial crisis.

- Need in India:

- Economic Recovery:

- With the pandemic hitting the banking sector, the RBI fears a spike in bad loans in the wake of a six-month moratorium it has announced to tackle the economic slowdown.

- Government Support:

- Professionally-run bad banks, funded by the private lenders and supported by the government, can be an effective mechanism to deal with Non-Performing Assets (NPA).

- The presence of the government is seen as a means to speed up the clean-up process.

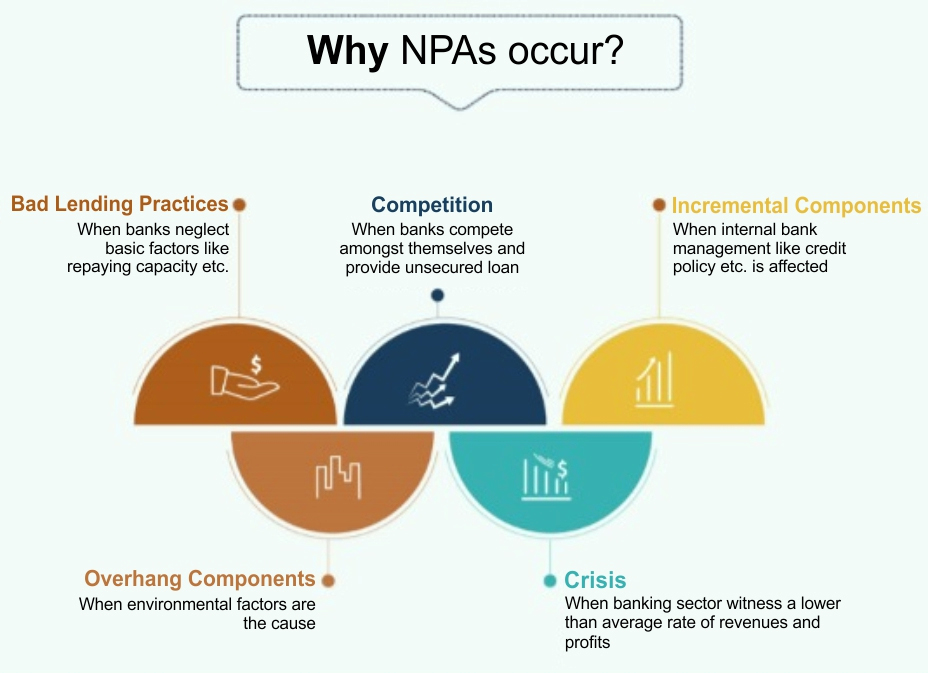

- Rising NPAs:

- Financial Stability Report (FSR): The RBI noted in its recent FSR that the gross NPAs of the banking sector are expected to shoot up to 13.5% of advances by September 2021, from 7.5% in September 2020.

- K V Kamath Committee: Noted that corporate sector debt worth Rs 15.52 lakh crore has come under stress after Covid-19 hit India, while another Rs 22.20 lakh crore was already under stress before the pandemic.

- The committee noted that companies in sectors such as retail trade, wholesale trade, roads and textiles are facing stress.

- Sectors that have been under stress pre-Covid include Non-Banking Financial Company (NBFC), power, steel, real estate and construction.

- International Precedents: Many other countries had set up institutional mechanisms to deal with a problem of stress in the financial system.

- Economic Recovery:

- Challenges :

- Mobilising Capital:

- Finding buyers for bad assets in a pandemic hit economy will be a challenge, especially when governments are facing the issue of containing the fiscal deficit.

- Not Addressing the Underlying Issue:

- Without governance reforms, the Public sector banks (accounted for 86%, of the total NPAs) may go on doing business the way they have been doing in the past and may end up piling-up of bad debts again.

- Also, the bad bank idea is like shifting loans from one government pocket (the public sector banks) to another (the bad bank).

- Provisioning Issue Tackled Through Recapitalization:

- Union Government, in the last few years, has infused nearly Rs 2.6 lakh crore in banks through recapitalisation.

- Those who oppose the concept of bad banks hold that the government has on its part recapitalised the banks to compensate for the write-offs and hence, there is no need for a bad bank.

- Market-related Issues:

- The price at which bad assets are transferred from commercial banks to the bad bank will not be market-determined and price discovery will not happen.

- Moral Hazard:

- Former RBI Governor Raghuram Rajan had said that a bad bank may create a moral hazard and enable banks to continue reckless lending practices, without any commitment to reduce NPAs.

- Mobilising Capital:

- Previous Proposals:

- In May 2020 the banking sector, led by the Indian Banks’ Association, had submitted a proposal for setting up a bad bank to resolve the NPA problem, proposing equity contribution from the government and banks.

- In 2017 the Economic Survey suggested Public Sector Asset Rehabilitation Agency or PARA, to buy out the NPAs of high value from Indian banks.

Way Forward

- Holistic Reforms:

- So long as Public sector banks managements remain beholden to politicians and bureaucrats, their deficit in professionalism will remain and subsequently, prudential norms in lending will continue to suffer. Therefore, the debate regarding setting up a bad bank must be preceded by proper implementation of holistic reforms in the banking sector, as envisaged under the Indra Dhanush plan launched in 2015.

- Tailor Made Approach:

- It’s a challenge that requires a response on multiple fronts. A bad bank cannot be the sole response. The most efficient approach would be to design solutions tailor-made for different parts of India’s bad loan problem and use Bad Bank only as a last resort once all other methods fail.