Indian Economy

GST 2.0-Balancing Growth and Fiscal Prudence

This editorial is based on “ GST 2.0 — short-term pain, possible long-term gain” which was published in The Hindu on 17/09/2025. The article discusses the recent GST reforms in India, highlighting changes in tax rates, their impact on consumption, revenue, and economic growth, and the associated fiscal and macroeconomic implications.

For Prelims: GST, The Goods and Services Tax Appellate Tribunal (GSTAT), Central GST (CGST), Value-added tax (VAT), GST Council, Goods and Services Tax Network (GSTN)

For Mains: Key Tax Reforms Under GST 2.0, Rationale Behind the Recent GST Reforms in India, Challenges of the GST reforms, Steps to Strengthen GST 2.0.

India’s Goods and Services Tax (GST) was introduced to enhance consumption and production efficiencies through a destination-based tax system, ensuring that taxes on inputs are rebated and the tax burden falls on final consumers. Over time, GST faced challenges such as multiple tax rates, inverted duty structures, and high compliance costs. The GST Reform Bill (GST 2.0), approved by the GST Council ushers in the largest overhaul of India’s indirect tax system since its launch in 2017, with significant rate reductions and structural simplifications.

What is the Goods and Services Tax (GST)?

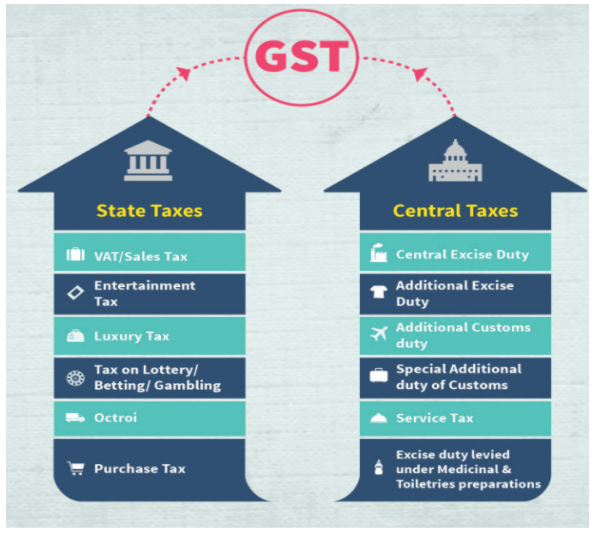

- About: Introduced by the 101st Constitutional Amendment Act, 2017, is a comprehensive indirect tax levied on the supply of goods and services in India.

- It is a value-added tax (VAT) that replaced multiple indirect taxes previously levied by the Centre and States.

- The Kelkar Task Force, constituted by the Ministry of Finance, played a pivotal role in shaping India’s Goods and Services Tax (GST) framework.

- Key Features:

- Dual GST Structure: Includes Central GST (CGST) and State GST (SGST); Integrated GST (IGST) is applicable for inter-state transactions.

- GST Council: It is the primary body for GST policymaking and rate decisions.

- It is established under Article 279A of the Constitution, is a joint forum of the Centre and States.

- It is chaired by the Union Finance Minister, the Union Minister of State in charge of Revenue or Finance as a Member, and the Minister in charge of Finance, Taxation, or any other Minister nominated by each State Government as Members.

- Goods and Services Tax Network (GSTN): Helps taxpayers in India to prepare, file returns, make payments of indirect tax liabilities and do other compliances.

- Threshold Exemption: Small businesses with turnover below a certain limit are exempt from GST. This makes compliance easier and protects microenterprises from excessive paperwork.

- Benefits of GST:

- Destination-Based Tax: Collected where goods/services are consumed, benefiting businesses with better cash flow and working capital.

- Ease of Doing Business: Technology-driven, minimal human interface, simplifies compliance, refunds, and registration.

- Boost to Make in India: Makes domestic goods competitive nationally and internationally.

- Exports: Supplies of goods or services, or both, to a Special Economic Zone (SEZ) are treated as zero-rated under GST, with quick refunds, thereby promoting international trade and improving the balance of payments.

- Revenue & Compliance: Expands tax base, increases government revenue, improves transparency, and enhances GDP by 1.5–2%.

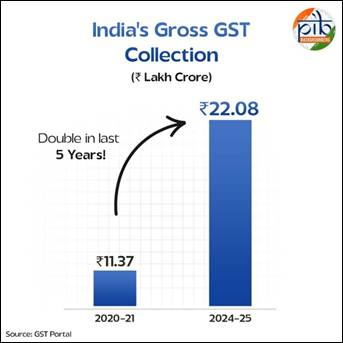

- Achievement of GST: In 2024–25, GST recorded its highest-ever gross collection of Rs 22.08 lakh crore, reflecting a year-on-year growth of 9.4%. The average monthly collection stood at Rs 1.84 lakh crore.

What are the Key Tax Reforms Under GST 2.0?

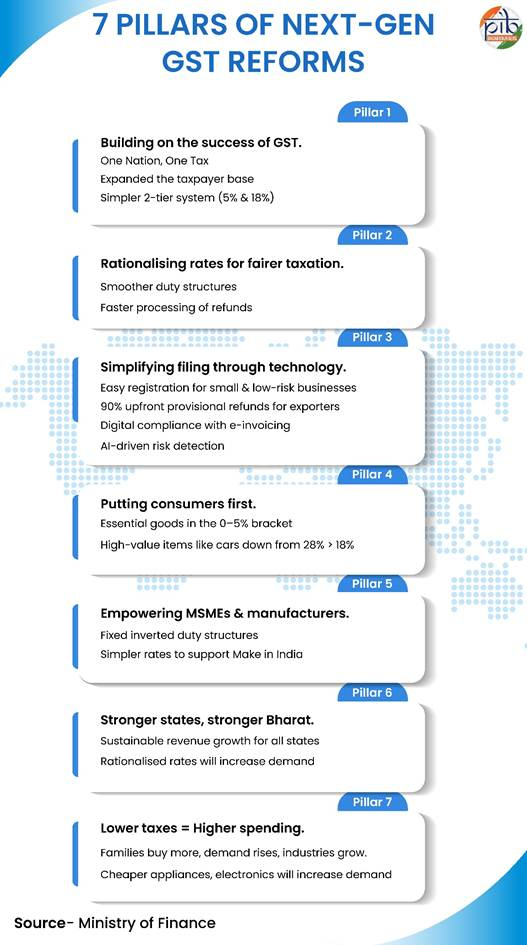

- Simplified GST Structure: GST 2.0 replaces four GST slabs (5%, 12%, 18%, and 28%) with a two-slab system (5% (merit rate) for essential items and 18% (standard rate) for others), plus a 40% demerit rate for luxury, sin, and demerit goods like tobacco and pan masala.

- Tax Relief for the Essential Goods: Full GST exemption on individual life and health insurance policies. Essential goods such as Ultra-High Temperature (UHT) milk, paneer, and Indian breads now carry nil GST.

- Consumer Goods: GST on small cars, TVs, air conditioners, cement, and auto parts has been reduced from 28% to 18%. GST on renewable energy devices has been reduced from 12% to 5%.

- These cuts are expected to stimulate manufacturing, promote green energy adoption, and boost domestic demand.

- Medical and Health Devices: GST on 33 lifesaving drugs has been reduced from 12% to nil.

- GST on three critical drugs used for cancer and rare diseases has been reduced from 5% to nil, strengthening healthcare access.

- Support for Agriculture and Rural Sectors: Machinery like tractors, harvesters, and composters: GST reduced from 12% to 5%.

- Fertilizer inputs such as sulphuric acid, nitric acid, and ammonia: GST reduced from 18% to 5%.

- Labour-intensive goods like handicrafts, marble, and leather items: GST reduced from 12% to 5%.

- Trade Facilitation and Dispute Resolution: The Goods and Services Tax Appellate Tribunal (GSTAT) will be operational by December 2025.

- Process reforms for refunds and registration will improve dispute resolution, reduce litigation, and provide predictability for businesses, especially MSMEs.

What is the Rationale Behind the Recent GST Reforms in India?

- Lower Prices, Higher Demand: Reduced GST rates make goods and services cheaper, increasing household savings and stimulating consumption, especially in essential and employment-intensive sectors.

- The reforms are expected to stimulate domestic demand, encourage formalization of the economy, and contribute to long-term fiscal stability

- Support for MSMEs: Lower input costs on items like cement, auto parts, and handicrafts make micro, small, and medium enterprises more competitive and promote entrepreneurship.

- Ease of Compliance: The simplified two-rate structure reduces tax disputes, accelerates decision-making, and lowers compliance costs for businesses.

- Evidence from past reforms suggests that lower rates combined with better compliance can increase GST collections in the medium term.

- Wider Tax Base : Simpler rates encourage voluntary compliance, broadening the tax net and potentially improving government revenues over time.

- Support for Manufacturing: Correcting inverted duty structures enhances domestic value addition, strengthens export competitiveness, and boosts the Make in India initiative.

- Social Protection: Exemptions on insurance and essential medicines strengthen household security and improve access to healthcare, addressing equity concerns.

- Consumption and Production Efficiency: By eliminating cascading taxes and rationalizing rates, GST 2.0 promotes resource allocation efficiency across sectors.

What Issues have Emerged in the Course of GST Reforms?

- Fiscal Revenue Shortfall: The reforms entail significant revenue loss, with estimates around ₹48,000 crore annually, primarily due to reduced rates and zero-rating of many goods.

- This creates fiscal pressure on both the central and state governments, forcing them to either cut expenditures or increase borrowing.

- Lower-than-budgeted nominal GDP growth (8.8% vs. 10.1% target) and contraction in direct taxes (-4%) exacerbate these challenges.

- States dependent on GST revenue transfers may curtail spending on welfare and infrastructure, potentially slowing growth.

- Input Tax Credit (ITC) and Cascading Tax Issues: Exemptions and zero-rated supplies restrict eligibility for ITC, leading to cascading taxes on inputs.

- This undermines GST’s principle of seamless credit flow and adds hidden costs to production and prices.

- For example, sectors producing exempt goods face higher effective taxes, feeding into inflationary pressures upstream.

- This undermines GST’s principle of seamless credit flow and adds hidden costs to production and prices.

- Rate Structure and Classification Ambiguities: Simplification to fewer slabs helps but classification disputes persist over which goods fall under given categories.

- Special rates and the new 40% slab for sin goods increase complexity in areas such as luxury and harmful goods taxation.

- Frequent adjustments risk instability and uncertainty for businesses, impacting investment and pricing decisions.

- Special rates and the new 40% slab for sin goods increase complexity in areas such as luxury and harmful goods taxation.

- Compliance Complexity and Technological Integration: Although slabs are rationalized, businesses face transitional compliance burdens, including recalibrating pricing, billing systems, and ERP updates.

- MSMEs may lack the capacity to swiftly adapt, facing higher compliance costs and learning curves.

- The GST Network (GSTN) and government leverage technologies like AI and data analytics to improve compliance and detect evasion, but frequent rule changes still complicate adherence.

- Enforcement and Dispute Resolution Delays: The GST Appellate Tribunal (GSTAT), essential for resolving disputes quickly, remains non-functional or delayed in several states.

- For instance, GST appellate benches are still not functional at 45 locations.

- This leads to a backlog of appeals in High Courts and prolonged litigation, increasing uncertainty and compliance risks.

- Administrative inefficiencies undermine taxpayer confidence and delay the resolution of disputes critical to smooth GST functioning.

- For instance, GST appellate benches are still not functional at 45 locations.

What Measures can be Adopted to Strengthen GST 2.0?

- Strengthen GST Administration: Enhance the GST Network (GSTN) and use AI/data analytics to improve compliance monitoring and reduce evasion.

- Resolve Classification Ambiguities and ensure clear guidelines for goods and services to reduce disputes and litigation.

- Operationalize the GST Appellate Tribunal (GSTAT) and make GSTAT functional in all states to expedite dispute resolution and restore taxpayer confidence.

- Support MSMEs: Provide capacity building, simplified compliance, and technological assistance to help small businesses adapt to new slabs.

- Align with Macro Growth Goals and ensure GST reforms complement investment-led growth, job creation, and resource allocation efficiency.

- Encourage Formalization as simplified rates and better compliance can expand the tax base, reduce informal sector dependence, and increase revenue over time.

- Monitor Fiscal Impact: Use targeted fiscal measures or liquidity management to offset revenue shortfall without compromising social and infrastructure spending.

- Follow Periodic Rate Review and reassess tax slabs and exemptions to ensure revenue sufficiency while promoting consumption and growth.

- Seamless Input Tax Credit (ITC) Mechanism: Ensuring a frictionless ITC chain prevents working capital blockages for businesses.

- Linking ITC eligibility with real-time invoice matching can reduce fraud while maintaining liquidity.

- Transparent rules for cross-utilization across states and sectors strengthen compliance. A robust ITC mechanism incentivizes formalization.

- Promote Awareness and Training: Conduct taxpayer education campaigns for businesses and consumers on new rates and compliance procedures.

- Expand digital invoicing, e-way bills, and automation to reduce administrative burden.

Conclusion:

The Next-Generation GST reforms represent a bold step towards building a simpler, fairer, and future-ready tax architecture. By reducing the tax burden on citizens and empowering farmers, MSMEs, women, youth, and middle-class families, GST 2.0 lays the foundation for inclusive prosperity, fiscal resilience, and global competitiveness.

|

Drishti Mains Question: Q. GST 2.0 represents a paradigm shift in India’s indirect tax regime. Critically analyze the rationale behind these reforms and evaluate their potential in overcoming structural challenges. |

UPSC Civil Services Examination Previous Year Question (PYQ)

Prelims

Q. Consider the following items: (2018)

- Cereal grains hulled

- Chicken eggs cooked

- Fish processed and canned

- Newspapers containing advertising material

- Which of the above items is/are exempted under GST (Goods and Services Tax)?

(a) 1 only

(b) 2 and 3 only

(c) 1, 2 and 4 only

(d) 1, 2, 3 and 4

Ans: (c)

Q.What is/are the most likely advantages of implementing the Goods and Services Tax (GST)? (2017)

- It will replace multiple taxes collected by multiple authorities and will thus create a single market in India.

- It will drastically reduce the ‘Current Account Deficit’ of India and will enable it to increase its foreign exchange reserves.

- It will enormously increase the growth and size of the economy of India and will enable it to overtake China in the near future.

Select the correct answer using the code given below:

(a) 1 only

(b) 2 and 3 only

(c) 1 and 3 only

(d) 1, 2 and 3

Ans: (a)

Mains

Q. Explain the rationale behind the Goods and Services Tax (Compensation to States) Act of 2017. How has COVID-19 impacted the GST compensation fund and created new federal tensions? (2020)

Q. Enumerate the indirect taxes which have been subsumed in the Goods and Services Tax (GST) in India. Also, comment on the revenue implications of the GST introduced in India since July 2017. (2019)