Important Facts For Prelims

Tier II Bonds

- 19 Nov 2025

- 9 min read

Why in News?

Several banks are actively issuing Tier II bonds to bolster their capital adequacy ratios (CAR) as required under Basel III norms, with total issuances expected to reach Rs 25,000 crore in FY 2025–26.

What are Tier II Bonds?

- About: Tier II bonds are subordinated debt instruments banks issue to boost capital and support operations. They count as Tier II (supplementary) capital under Basel-III and help improve the CAR.

- CAR indicates a bank’s financial strength, with a higher ratio providing a stronger buffer against distress. CAR = (Eligible Capital ÷ Risk-Weighted Assets) × 100%.

- Tier II Bonds are different from Tier I Bonds as they strengthen a bank’s supplementary capital, whereas Tier I (AT1) Bonds strengthen its core capital (equity and retained earnings).

- Key Features of Tier II Bonds:

- Maturity: They are typically long-term instruments with original maturities of at least 5 years.

- Subordination: Tier II bondholders are paid after all depositors, senior debt holders, and general creditors in the event of a liquidation. However, they rank above equity holders.

- Coupon Payments: They pay regular interest (coupons) and generally offer higher coupon rates than senior bonds due to higher risk.

- Call Options: Most Tier II bonds include a call option, allowing the bank to redeem the bonds after a specified period (e.g., 5 or 10 years).

- Loss Absorbency (Gone-Concern Capital): Tier I capital is considered "gone-concern" capital, meaning it is intended to absorb losses if a bank fails and is in the process of being wound up.

- This is in contrast to Tier I capital, which absorbs losses on a "going-concern" basis while the bank is still operational.

- Issued By: Both public and private banks issue Tier II bonds to meet regulatory capital requirements, support business expansion, and comply with CAR norms without issuing new equity and diluting shareholders.

- Investors in Tier II Bonds: Institutional investors such as insurance companies, pension funds, mutual funds, and hedge funds, as well as retail investors through platforms or public issues, invest in Tier II bonds.

What is the Difference Between Tier I and Tier II Bonds?

|

Feature |

Tier I Bonds (Commonly called Additional Tier 1 or AT1) |

Tier II Bonds (Subordinated Debt) |

|

Core Purpose |

To act as shock absorbers during ongoing stress. They are the first line of defense after equity. |

To act as a loss-absorbing buffer during liquidation or winding up. |

|

Nature & Seniority |

Perpetual; they have no maturity date. They are the most junior form of debt, just above equity. |

Have a fixed maturity. They are senior to Tier I but junior to regular debt. |

|

Trigger Mechanism |

Can be written down to zero or converted to equity if the bank's Common Equity Tier 1 (CET1) ratio falls below a pre-specified level. |

Loss absorption typically only happens during the point of non-viability or liquidation, after Tier I is used. |

What are Basel Norms?

- About: Basel Norms are a set of international banking regulations developed by the Basel Committee on Banking Supervision (BCBS) to strengthen the global financial system by ensuring that banks hold enough capital to absorb unexpected losses.

- Pillars of Basel Norms: The Basel framework rests on three pillars:

- Pillar 1 – Minimum Capital Requirements: Banks must hold capital proportional to their risk-weighted assets (RWA), with riskier assets requiring more capital.

- Pillar 2 – Supervisory Review: Regulators assess each bank’s internal risk processes and ensure capital stays above minimum requirements.

- Pillar 3 – Market Discipline: Banks must disclose their risk profiles and capital levels to promote transparency and encourage prudent behavior through market scrutiny.

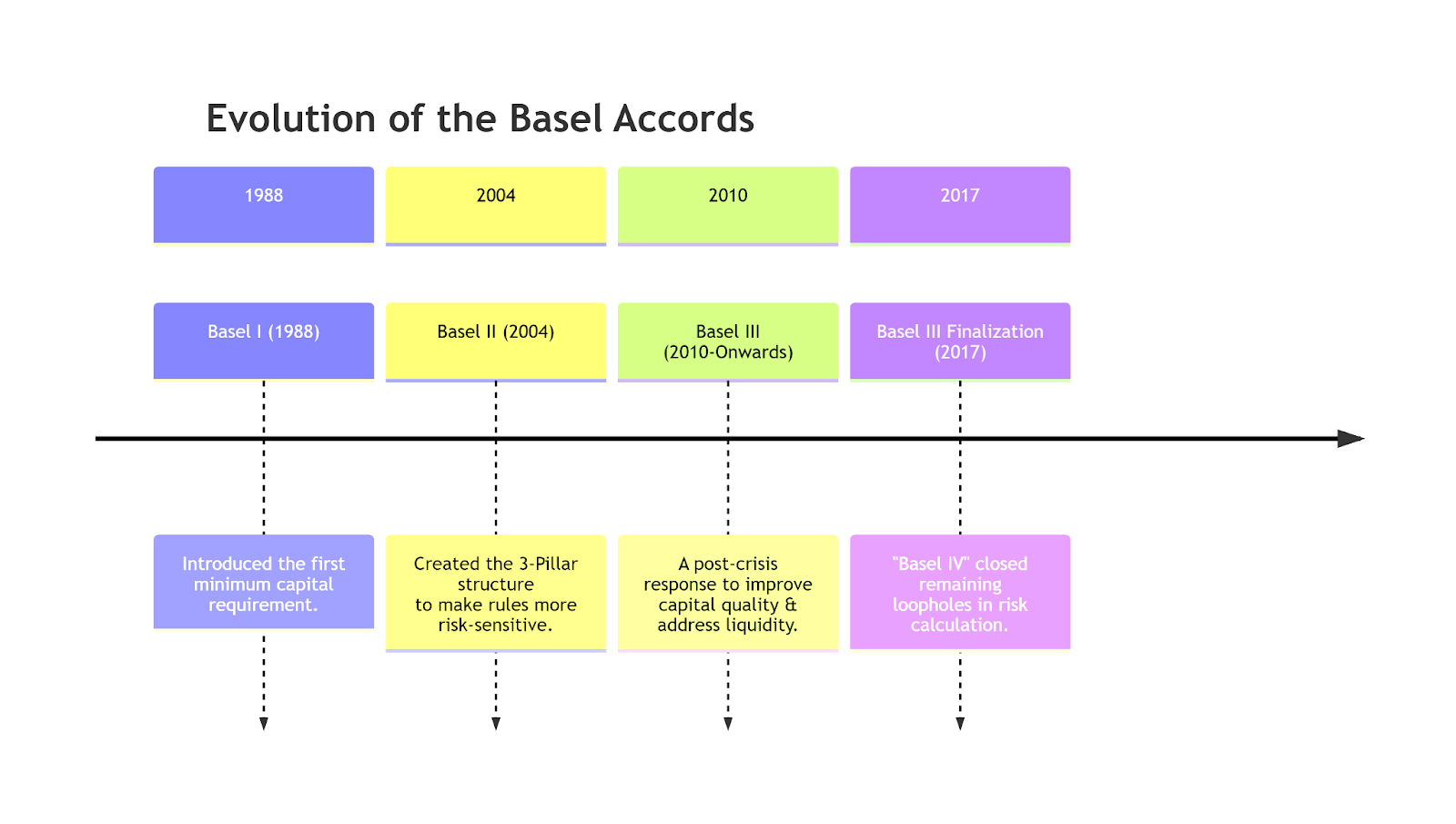

- Evolution: Basel has evolved from Basel I, II, III, and now IV to strengthen the banking system and respond to financial crises.

- Basel I (1988) introduced a capital measurement system focused on credit risk and risk-weighted assets, setting minimum capital requirements for banks.

- Basel II (2004) refined this by adding the three-pillar framework of minimum capital, supervisory review, and market discipline.

- Basel III (2010), developed after the 2007–08 crisis, strengthened banks’ capital base, liquidity, and leverage standards.

- Basel IV (2017) aims to tighten remaining gaps by making RWA calculations more consistent across banks and limiting the misuse of internal models to reduce capital requirements.

Basel Committee on Banking Supervision (BCBS)

- About: BCBS is the global standard-setter for banking regulation, creating frameworks like Basel I–III to strengthen financial stability.

- It was formed in 1974 after the Herstatt crisis, when a German bank collapsed.

- Membership: Includes 45 members from 28 jurisdictions, covering major advanced and emerging economies including India.

- Functions: Sets banking standards, promotes supervisory cooperation, monitors implementation, and identifies global financial risks.

- Governance: The BCBS operates under the guidance of the Group of Central Bank Governors and Heads of Supervision (GHOS).

Frequently Asked Questions (FAQs)

1. What are Tier II bonds?

Tier II bonds are subordinated debt instruments counted as supplementary capital under Basel-III, issued by banks to bolster the Capital Adequacy Ratio without issuing equity.

2. What is the primary objective of the Basel Committee on Banking Supervision (BCBS)?

The BCBS sets international banking standards (like Basel III) to promote financial stability by ensuring banks maintain sufficient capital, improve risk management, and enhance supervisory practices globally.

3. Name the three pillars of the Basel regulatory framework.

The three pillars are: Pillar 1 - Minimum Capital Requirements, Pillar 2 - Supervisory Review Process, and Pillar 3 - Market Discipline.

UPSC Civil Services Examination, Previous Year Questions (PYQs)

Q. Consider the following statements: (2018)

- Capital Adequacy Ratio (CAR) is the amount that banks have to maintain in the form of their own funds to offset any loss that banks incur if the account-holders fail to repay dues.

- CAR is decided by each individual bank.

Which of the statements given above is/are correct?

(a) 1 only

(b) 2 only

(c) Both 1 and 2

(d) Neither 1 nor 2

Ans: (a)

Q. ‘Basel III Accord’ or simply ‘Basel III’, often seen in the news, seeks to (2015)

(a) develop national strategies for the conservation and sustainable use of biological diversity

(b) improve banking sector’s ability to deal with financial and economic stress and improve risk management

(c) reduce the greenhouse gas emissions but places a heavier burden on developed countries

(d) transfer technology from developed countries to poor countries to enable them to replace the use of chlorofluorocarbons in refrigeration with harmless chemicals

Ans: (b)