.jpg)

.png)

.jpg)

PCS Parikshan

PCS ParikshanChhattisgarh Switch to Hindi

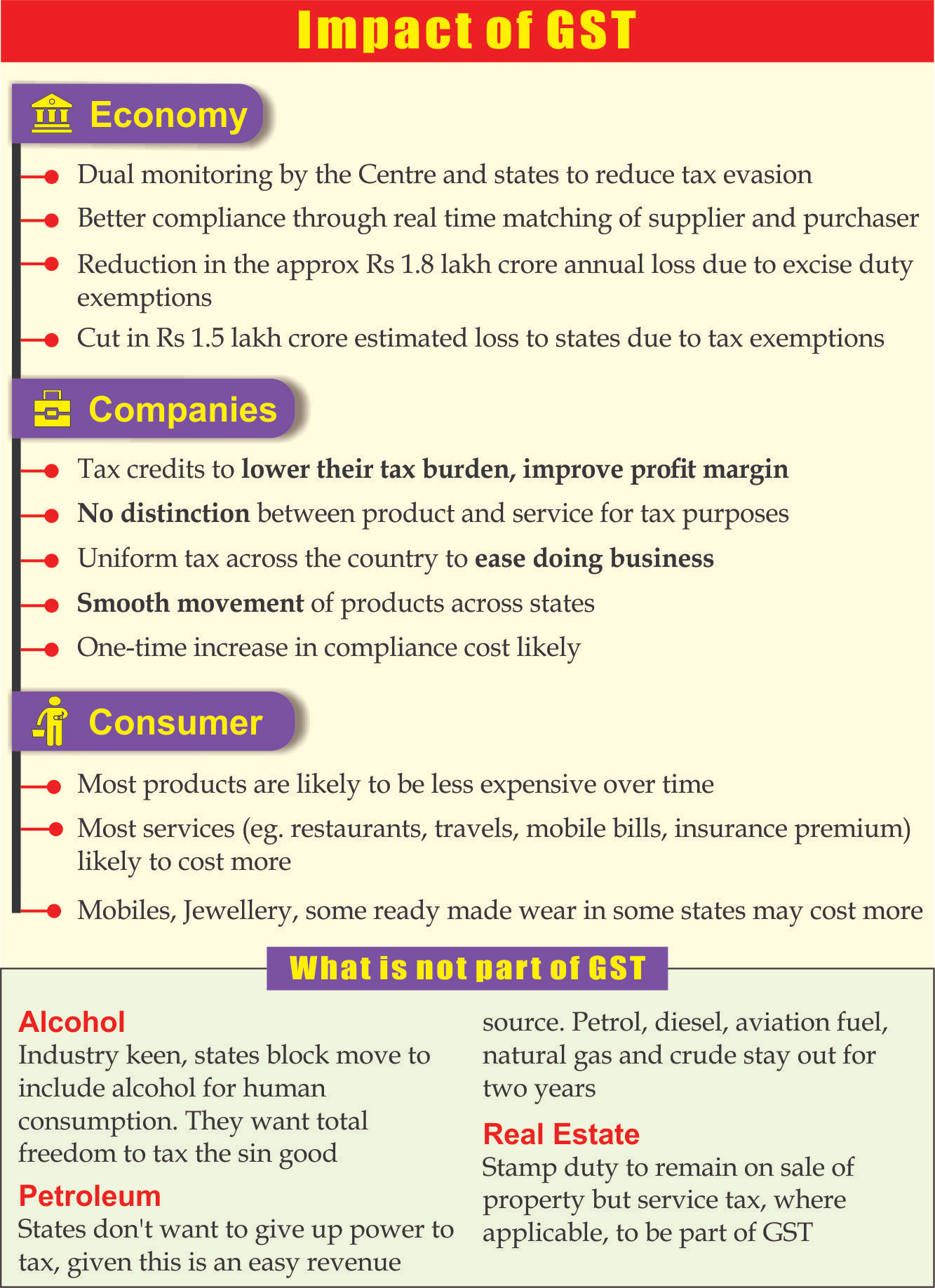

Chhattisgarh Recorded the Highest GST Growth Rate

Why in News?

Chhattisgarh topped the country in Goods and Services Tax (GST) collection growth, posting an 18% increase over the previous fiscal year 2024-25.

Key Points

- Factors Behind Chhattisgarh’s GST Growth:

- Growth in GST Collections:

- Chhattisgarh's total GST and VAT (Value Added Tax) revenue for FY 2024–25 reached Rs 23,448 crore, accounting for nearly 38% of the state’s own tax collections.

- VAT: Tax on goods sold, applied at each stage of the supply chain. It is imposed on goods that are excluded from the GST regime like alcoholic beverages, petroleum products etc.

- This sharp increase in tax revenues highlights the effectiveness of its policy measures and enforcement strategies.

- Chhattisgarh's total GST and VAT (Value Added Tax) revenue for FY 2024–25 reached Rs 23,448 crore, accounting for nearly 38% of the state’s own tax collections.

- Streamlined GST Registration Process:

- One of the key reforms that contributed to this success is the reduction of GST registration time from 13 days to just 2 days, significantly improving the ease of doing business in Chhattisgarh

- Technology-Led Monitoring and Enforcement:

- The state has employed advanced technology to monitor and recover evaded taxes.

- Targeted drives and enhanced enforcement actions, such as the establishment of GST offices across all 33 districts, have ensured transparency and better taxpayer services.

- Growth in GST Collections:

Goods and Services Tax (GST)

- About:

- GST is a value-added tax system that is levied on the supply of goods and services in India.

- It is a comprehensive indirect tax that was introduced in India on 1st July 2017, through the 101st Constitution Amendment Act, 2016, with the slogan of ‘One Nation One Tax’.

- GST Council:

- About: The GST Council, a constitutional body under Article 279-A (101st Amendment, 2016), makes recommendations on GST implementation.

- GST is a value-added (Ad Valorem) and indirect tax system that is levied on the supply of goods and services in India.

- Members: The Council includes the Union Finance Minister (Chairperson), Union Minister of State (Finance), and a finance or any other minister from each state.

- Nature of Decisions: In the Mohit Minerals case, 2022, the Supreme Court ruled GST Council recommendations are not binding, as Parliament and states have simultaneous legislative powers on GST.

- About: The GST Council, a constitutional body under Article 279-A (101st Amendment, 2016), makes recommendations on GST implementation.

Chhattisgarh Switch to Hindi

Chhattisgarh Forest Department Withdraws Community Forest Rights Directive

Why in News?

The Chhattisgarh forest department has recently withdrawn its directive, which had barred government departments, NGOs, and private entities from undertaking any work related to Community Forest Resource Rights (CFRR).

Key Points

- Withdrawal of Advisory:

- The forest department initially claimed control over CFRR lands granted under the Forest Rights Act (FRA) 2006, pending the release of model management plans by the central government.

- The advisory designated the forest department as the nodal agency for CFRR implementation, which led to protests from tribal communities who viewed this as a violation of their rights to manage forest resources.

- To address the concerns, the forest department has requested the Ministries of Tribal Affairs and Environment to urgently release detailed CFRR plans, implementation guidelines, and training modules for all stakeholders.

- Forest Rights Act (FRA), 2006

- About: It was enacted to officially recognize and grant forest rights and tenure to forest-dwelling Scheduled Tribes (STs) and Other Traditional Forest Dwellers (OTFDs) who have lived in these forests for generations without formal documentation of their rights.

- Aim: It seeks to correct historical injustices faced by these communities due to colonial and post-colonial forest management policies that overlooked their deep, symbiotic relationship with the land.

- To empower these communities by enabling sustainable access to land and utilization of forest resources, promoting biodiversity and ecological balance, and protecting them from illegal evictions and displacement.

- Provision:

- Ownership Rights: Grants ownership over Minor Forest Produce (MFP). Allows collection, use, and disposal of forest produce.

- MFP refers to all non-timber forest products of plant origin, including bamboo, brushwood, stumps, and canes.

- Community Rights: Includes traditional usage rights such as Nistar (a type of Community Forest Resource).

- Habitat Rights: Protects the rights of primitive tribal groups and pre-agricultural communities to their traditional habitats.

- Community Forest Resource (CFR): Enables communities to protect, regenerate, and sustainably manage forest resources they have traditionally conserved.

- The Act facilitates the diversion of forest land for public welfare projects managed by the government, subject to Gram Sabha approval.

- Ownership Rights: Grants ownership over Minor Forest Produce (MFP). Allows collection, use, and disposal of forest produce.

- Community Forest Resource Rights (CFRR)

- The Community Forest Resource rights under Section 3(1)(i) of the Scheduled Tribes and Other Traditional Forest Dwellers (Recognition of Forest Rights) Act, 2006 (commonly referred to as the Forest Rights Act) provides for recognition of the right to “protect, regenerate or conserve or manage” the community forest resource.

- These rights allow the community to formulate rules for forest use by itself and others and thereby discharge its responsibilities under Section 5 of the FRA.

- The Community Forest Resource rights under Section 3(1)(i) of the Scheduled Tribes and Other Traditional Forest Dwellers (Recognition of Forest Rights) Act, 2006 (commonly referred to as the Forest Rights Act) provides for recognition of the right to “protect, regenerate or conserve or manage” the community forest resource.