Indian Economy

The Rise of Indian Manufacturing Sector

- 23 Sep 2025

- 22 min read

This editorial is based on “In turbulent times, India needs a reimagined ‘swadeshi’ industry,” which was published in The Indian Express on 23/09/2025. The article emphasizes revitalizing India’s swadeshi industry, highlighting that domestic manufacturing, regardless of a company’s origin or brand, advances self-reliance and strengthens global competitiveness.

For Prelims: Manufacturing, Make in India, Production Linked Incentive (PLI) schemes, PM-MITRA parks, GST Reforms, Worker Population Ratio (WPR), Labour Force Participation Rate (LFPR), National Manufacturing Mission (NMM), National Logistics Policy (NLP), National Industrial Corridor Development Programme

For Mains: Current Status of Manufacturing Sector in India, Key Growth Drivers for Manufacturing Sector in India, Key Challenges Faced By Manufacturing Sector in India.

Manufacturing is widely recognised as the backbone of economic development. For India, it offers immense potential to generate employment, boost productivity, strengthen exports, and reduce import dependence. Government initiatives such as the Make in India,Production Linked Incentive (PLI) schemes, PM-MITRA parks, and the National Manufacturing Mission have catalyzed growth, positioning India as a global manufacturing hub. However, challenges such as infrastructure gaps, skill shortages, high logistics costs, and the need for higher domestic value addition continue to constrain its full potential.

What is the Current Status of the Manufacturing Sector in India?

- Manufacturing Output Growth and Sector Resilience: India’s manufacturing sector showed robust resilience with a 4.26% growth in FY 2024-25.

- The Index of Industrial Production (IIP) highlights manufacturing contributing about 77% of industrial output, with key segments such as basic metals, electrical equipment, and machinery leading growth.

- Contribution to GDP and Ambitious Targets: Manufacturing currently accounts for nearly 17% of India’s GDP.

- The government has set an ambitious target to increase this to 25% by 2030 under initiatives like “Make in India” and “Atmanirbhar Bharat”, aiming to boost economic growth, employment, and global competitiveness.

- Export Momentum in Key Sectors: Manufacturing exports have surged by 2.52% year-on-year, reaching USD 184.13 billion in the first five months of FY 2024-25.

- Electronics, pharmaceuticals, engineering goods, and automobiles are major contributors, benefiting from rising global demand and government export incentives.

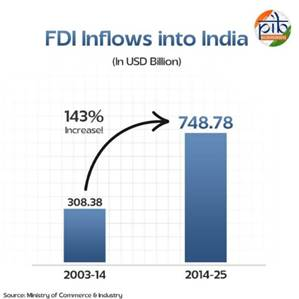

- Foreign Direct Investment: India has steadily positioned itself as a preferred destination for global investors.

- Total FDI inflows into India over the last eleven years (2014–25) stood at USD 748.78 billion, up 143% compared to USD 308.38 billion received during 2003–14.

- India clocked USD 81.04 billion in gross FDI inflows in FY 2024–25, up by 14% year-on-year growth.

- Manufacturing FDI accelerated 18% to USD 19.04 billion in FY 2024-25 (from USD 16.12 billion in FY 2023–24).

- Maharashtra led the FDI leaderboard with 39% of equity inflows, followed by Karnataka (13%) and Delhi (12%) in 2024-25.

- Total FDI inflows into India over the last eleven years (2014–25) stood at USD 748.78 billion, up 143% compared to USD 308.38 billion received during 2003–14.

What are the Recent Drivers Behind India’s Manufacturing Momentum?

- Electronics Manufacturing Transformation: Electronics production increased sixfold in the last 11 years; exports grew eightfold.

- Value addition in electronics jumped from 30% to 70%, with a target of 90% by FY27.

- India is now the second-largest mobile manufacturer globally.

- Attracted USD 4 billion in FDI in electronics since FY2020-21.

- Pharmaceutical Industry- “Pharmacy of the World”: India ranks 3rd in global pharma by volume and 14th by value.

- Supplies 50% of global vaccine demand and 40% of US generics.

- Backed by policy support for Pharmaceuticals like the PLI scheme (₹15,000 crore) and Strengthening of Pharmaceuticals Industry (SPI) scheme (₹500 crore), the industry continues to expand its global footprint.

- Automotive Industry Expansion: It contributes 7.1% to GDP and 49% to manufacturing GDP.

- FY25 production: 3.10 crore units across passenger vehicles, commercial vehicles, two- and three-wheelers, and quadricycles.

- India is the fourth-largest automobile producer globally, with potential to strengthen the automotive value chain internationally.

- Textiles Sector Growth: As per Economic Survey 2024-25, India’s textile & apparel industry is among the largest industries globally, contributing around 2.3% to GDP, 13% to industrial production, and 12% to total exports.

- The sector is set to grow to US$350 billion by 2030, further strengthening India’s position in the global market.

- It is the second largest employment generator after agriculture, with over 45 million people employed directly, including women and the rural population.

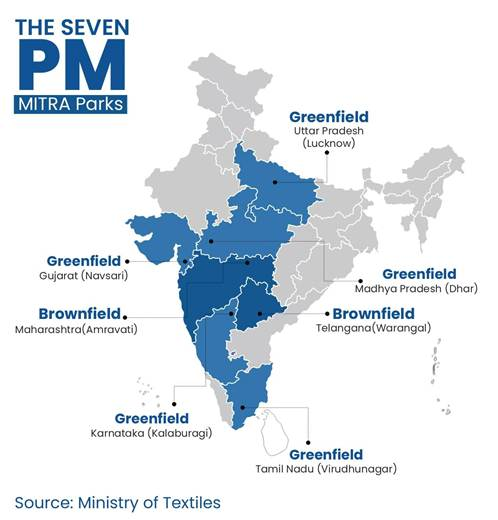

- To support the industry further, the government has approved seven PM Mega Integrated Textile Region & Apparel (PM MITRA) Parks backed by ₹4,445 crore over six years through 2027-28.

- Digital Manufacturing: Technological adoption has surged, with firms embracing automation, smart manufacturing, and big data analytics to improve productivity and quality.

- 65% of Indian manufacturers had adopted AI by 2024, up from 45% in 2022 (NASSCOM, MeitY).

- As per NASSCOM’s latest data, India ranks 6th among the world’s top 9 DeepTech ecosystems.

- Sustainability and Green Manufacturing: Regulatory pressure and global demand for eco-friendly goods foster investment in renewable energy and waste reduction.

- The government approved a ₹24,000 crore PLI package to boost solar PV module production, projected to add 65GW capacity.

- Skill Development: Workforce modernization and skilling initiatives, such as PMKVY, are preparing millions for Industry 4.0 roles in robotics, IoT, and AI.

- India’s employment surged with 17 crore jobs created in the past decade, reflecting focus on youth-centric policies and Viksit Bharat vision.

- PLFS data August 2025 indicates positive trends:

- The Worker Population Ratio (WPR) rose to 52.2%.

- The Labour Force Participation Rate (LFPR) for women improved to 33.7%.

- Unemployment rate (UR) eased to 5.1% overall; male UR fell to 5.0%, highlighting broad-based employment creation and inclusivity across sectors, including manufacturing.

- In manufacturing, job creation rose from 6% (2004–2014) to 15% in the last decade.

What are the Policy Catalysts Powering the Surge in India’s Manufacturing Sector?

- National Manufacturing Mission (NMM): Launched in Union Budget 2025–26, NMM integrates policy, execution, and governance across ministries and states.

- Focuses on sustainable manufacturing, promoting solar PV modules, EV batteries, green hydrogen, and wind turbines.

- Guides India’s transition from incremental growth to global manufacturing leadership, aligning with net-zero 2070 commitments.

- GST Reforms:

- Simplified Structure: GST 2.0 introduces a two-slab system, reducing compliance costs.

- Cost Compression & Value Chains: Goods like packaging, textiles, leather, wood, and logistics essentials attract only 5% GST, lowering manufacturing costs and boosting exports.

- MSMEs & Export-Oriented Industries: Rationalized rates and faster refunds in textiles, handicrafts, food processing, toys, leather support working capital and scale-up.

- Logistics Efficiency: GST cuts on trucks and delivery vans (from 28% to 18%) improve supply chain efficiency for freight-intensive sectors.

- Auto & Ancillary Acceleration: Reduced GST on vehicles, auto parts, tractors increases affordability, driving demand and production.

- Make in India: Launched in 2014, aims to raise manufacturing’s share in GDP from 17% to 25%, focusing on electronics, automotive, defense, and textiles.

- Production Linked Incentive (PLI) Scheme:Launched in 2020, covering 14 key sectors including mobile phones, electronics, pharmaceuticals, textiles, drones.

- Provides financial incentives linked to incremental production and sales, driving scale and competitiveness.

- Total outlay of ₹1.97 lakh crore ensures economies of scale and global competitiveness.

- National Logistics Policy (NLP): Launched September 2022, aims to reduce logistics costs, enhance efficiency, and drive digital integration.

- Targets top 25 ranking in World Bank Logistics Performance Index by 2030.

- Comprehensive Logistics Action Plan (CLAP) focuses on digital systems, standardization, HR development, state coordination, and logistics parks, enabling seamless multi-modal connectivity.

- Startup India-Driving Innovation and Jobs: Launched in January 2016 to support entrepreneurship and job creation.

- India hosts the third-largest startup ecosystem with 1.91 lakh DPIIT-recognized startups as of 9 September 2025.

- Startups have generated over 17.69 lakh direct jobs (as of 31 January 2025), fostering innovation and economic development.

- Industrialization and Urbanization: The National Industrial Corridor Development Programme creates integrated industrial cities as Smart Cities.

- Promotes robust multi-modal connectivity to support manufacturing and systematic urbanization.

- 12 new projects approved last year with an estimated ₹28,602 crore investment, enhancing India’s attractiveness for manufacturing and investment.

- In alignment with this, the Development of Enterprises and Strategic Hubs (DESH) Bill aims to streamline approvals, enhance infrastructure, and provide incentives for enterprises in these corridors.

What are the Main Challenges Facing India’s Manufacturing Sector?

- Infrastructure Deficiencies: India’s logistics costs have fallen to 7.97% of GDP, showing notable efficiency gains.

- Yet, gaps in multimodal connectivity continue to hinder seamless integration of road, rail, and ports.

- Frequent power outages, inadequate water supply, and poor transport networks disrupt manufacturing efficiency.

- Weak port and warehousing infrastructure delays supply chains.

- Regulatory and Policy Bottlenecks: Complex regulations and multiple clearances increase transaction costs.

- Slow land acquisition processes discourage large-scale manufacturing projects. MSMEs face disproportionate compliance burdens due to limited resources.

- India’s manufacturing MSMEs face over 1,450 regulatory obligations annually across labour, environment, taxation, and corporate laws, making compliance complex and time-consuming.

- The average compliance cost for a typical manufacturing MSME ranges between ₹13 lakh to ₹17 lakh per year, significantly impacting their profitability and growth potential.

- Skill Gap: Only 4.7% of India’s workforce has formal skill training versus 96% in South Korea.

- Lack of trained manpower restricts productivity, quality control, and adoption of advanced technologies.

- Industry often faces a mismatch between academic training and practical industrial needs.

- Access to Finance: MSMEs struggle with limited access to affordable credit and face working capital shortages.

- Dependence on informal finance leads to higher borrowing costs, constraining expansion and modernization.

- As of March 2025, the total commercial credit exposure to MSMEs in India reached ₹35.2 lakh crore (USD 4.3 trillion), growing by 13% year-on-year. Yet, a significant credit gap remains, limiting many MSMEs’ growth and modernization.

- Global Competition and Innovation Deficit: Indian manufacturers face stiff competition from low-cost producers like China and Vietnam.

- Limited investment in R&D, weak design capabilities, and dependence on imported technology reduce competitiveness.

- Failure to move up the value chain restricts integration into global supply networks.

- Environmental and Sustainability Pressures: Manufacturing is resource-intensive, straining water, land, and energy.

- Pressure to decarbonize and meet net-zero 2070 targets adds compliance costs.

- Ethanol blending in automotive fuels has emerged as a key sustainability measure, with India targeting 20% blending by 2025-26 to curb fossil fuel dependence and reduce emissions.

- However,challenges include feedstock supply constraints, pricing issues, and potential impacts on food security, affecting ethanol availability and industry uptake.

- Global buyers increasingly demand green supply chains, requiring Indian firms to invest in clean-tech.

- The European Union’s Carbon Border Adjustment Mechanism (CBAM) will further impact Indian manufacturing exports, especially in carbon-intensive sectors like steel, cement, and aluminum, making sustainability compliance a competitiveness issue as well.

- Trade & Market Access Barriers: Non-tariff barriers in developed countries limit exports.

- Developed countries impose NTBs such as stringent product standards, carbon taxes, deforestation regulations, and certification requirements that restrict Indian exports.

- For example, the European Union’s carbon border adjustment tax and forestry regulations have become hurdles for Indian goods.

- India’s cautious approach to free trade agreements (FTAs) reduces integration into global value chains.

- Export competitiveness weakened by currency volatility and rising input costs.

- Also, recently tariff barriers have emerged as a significant challenge for Indian exports.

- Tariff barriers like the United States imposed a steep 50% tariff on many Indian goods effective August 27, 2025, doubling the previous 25% tariff implemented earlier that year.

- This affects textiles, gems and jewellery, leather, marine products, chemicals, and auto components, putting 55% of India’s US-bound exports, worth $87 billion, at risk.

- Developed countries impose NTBs such as stringent product standards, carbon taxes, deforestation regulations, and certification requirements that restrict Indian exports.

- Slow Technological Adoption:India’s Industry 4.0 market size was valued at around USD 5.5 billion in 2024 and is projected to grow to nearly USD 27 billion by 2033, at a CAGR of 19.2%.

- Despite this rapid growth, adoption remains uneven and comparatively slow among MSMEs and traditional manufacturers.

- Approximately 57% of firms perceive a risk of job displacement from automation in the absence of adequate reskilling programs.

- Dependence on foreign technologies for advanced manufacturing.(US or China)

What Can India Learn from International Best Practices in Manufacturing ?

|

What Measures Should Be Adopted to Strengthen Manufacturing Momentum in India?

- Simplify Regulatory Frameworks: Fast-track land acquisition, rationalize taxes, and improve contract enforcement, per Parliamentary Standing Committee on Industry recommendations.

- The Amaravati example shows that cluster-based land pooling holds great potential, but addressing local concerns remains crucial

- Augment R&D Investment: Allocate more funds for innovation and promote industry-academia collaboration in emerging sectors, following Korean and German innovation clusters.

- A portion of future PLI disbursements could be tied to in-house R&D spending thresholds, beginning with critical sectors such as electronics, semiconductors, and pharmaceuticals.

- Expand Credit to MSMEs: Implement specialized financing schemes and Credit Guarantee Funds for MSMEs and startups.

- Offer tax incentives to large corporations that promptly pay their MSME suppliers and onboard them onto TReDS (Trade Receivables Discounting System) platforms. This unlocks working capital for MSMEs tied up in invoices.

- Accelerate Infrastructure Build-Out: Ensure reliable power, transport, water, and digital connectivity by completing pending industrial corridor projects and expanding dedicated freight corridors.

- Implement a GIS-tagged, real-time dashboard, similar to the PM GatiShakti National Master Plan, to monitor all infrastructure projects. This platform should be used to identify and resolve inter-departmental bottlenecks in real-time, ensuring accountability and timely completion.

- Promote Export Competitiveness: Lower logistics costs, negotiate trade agreements for better market access, and incentivize standards certification for global markets.

- Implement "Districts as Export Hubs" Initiative swiftly by actively identifying products with export potential in each district and provide targeted support including design, packaging, marketing, and certification assistance to local producers.

- Integrate Sustainability: Launch Green Manufacturing Missions to align with SDGs and global requirements, and incentivize energy-efficient technologies.

- Also, there is a need to go beyond energy efficiency and encourage industries to adopt a circular economy model focusing on waste reduction, reuse of materials, and recycling.

- This not only reduces environmental impact but also cuts down on raw material import dependency and creates new business opportunities.

Conclusion

India’s manufacturing sector is set for robust expansion, driven by policy pushes, global demand shifts, and technology adoption. To fully realize its demographic dividend and global hub ambitions, India must address persistent infrastructure, regulatory, skill, and innovation gaps, drawing lessons from global best practices and committee recommendations. Achieving a 25% GDP share and global leadership in manufacturing requires visionary reforms, sustained investment, and collaborative efforts across stakeholders and sectors.

|

Drishti Mains Question: Examine the strategic role of manufacturing in achieving long-term economic resilience and export competitiveness. What institutional and policy measures are needed to fully realise India’s potential as a global manufacturing hub? |

UPSC Civil Services Examination, Previous Year Questions (PYQs)

Prelims

Q. In the ‘Index of Eight Core Industries’, which one of the following is given the highest weight? (2015)

(a) Coal production

(b) Electricity generation

(c) Fertilizer production

(d) Steel production

Ans: (b)

Mains

Q.1. “Industrial growth rate has lagged behind in the overall growth of Gross-Domestic-Product(GDP) in the post-reform period” Give reasons. How far are the recent changes in Industrial Policy capable of increasing the industrial growth rate? (2017)

Q.2. Normally countries shift from agriculture to industry and then later to services, but India shifted directly from agriculture to services. What are the reasons for the huge growth of services vis-a-vis the industry in the country? Can India become a developed country without a strong industrial base? (2014)