Indian Economy

System of Cess In India

- 07 Oct 2020

- 12 min read

The given article is based upon ‘Cessed Out’ was published in ‘The Hindu Business Line’ on 30/09/2020. It talks about the cess system of India and how far the actual purpose of cess is fulfilled and what are the issues faced.

Cess is a tax levied for a specific purpose and ought to be used for the same only.

The process of cess levying occurs after Parliament has authorised its creation through an enabling legislation that specifies the purpose for which the funds are being raised.

However, the proceeds collected from cess levies and other charges are not being used lately for the purpose they were introduced.

The latest audit of the Union Government’s accounts tabled in Parliament has revealed that about 40% of all the cess collections in 2018-19 have been retained in the Consolidated Fund of India (CFI).

What Is A Cess?

- Different from the usual taxes and duties like excise and personal income tax, a Cess is imposed as an additional tax besides the existing tax (tax on tax) with a purpose of raising funds for a specific task.

- For example, the Swachh Bharat cess is levied by the government for cleanliness activities that it is undertaking across India.

- The Union government is empowered to raise revenue through a gamut of levies, including taxes (both direct and indirect), surcharges, fees and cess.

- A cess, generally paid by everyday public, is added to their basic tax liability paid as part of total tax paid.

- Article 270 of the Constitution allows cess to be excluded from the purview of the divisible pool of taxes that the Union government must share with the States.

Divisible Pool

- A divisible pool is a portion of Gross Tax Revenue (GTR) that is distributed between the Centre and the States.

- It consists of all taxes, except surcharges and cess levied for specific purpose, net of collection charges.

|

Difference between Cess and Tax |

|

|

Cess |

Tax |

|

|

|

|

|

|

Background

- There are 42 cesses that have been levied at various times since 1944 as listed in a report by the Vidhi Centre for Legal Policy in August 2018.

- The very first cess was levied on matches, according to this study.

- Post Independence, the cess taxes were linked initially to the development of a particular industry, including a salt cess and a tea cess in 1953.

- Subsequently, the introduction of a cess was motivated by the aim of ensuring labour welfare.

- Some cesses that exemplified this thrust were the iron ore mines labour welfare cess in 1961, the limestone and dolomite mines labour welfare cess of 1972 and the cine workers welfare cess introduced in 1981.

Types of Cesses

The introduction of the The Goods and Services tax (GST) in 2017 led to most cesses being done away with and as of August 2018, there were only seven cesses that continued to be levied.These were:

- Cess on Exports

- Cess on Crude Oil

- Health and Education Cess

- Road and Infrastructure Cess,

- Other Construction Workers Welfare Cess,

- National Calamity Contingent Duty

- Duty on Tobacco and Tobacco Products

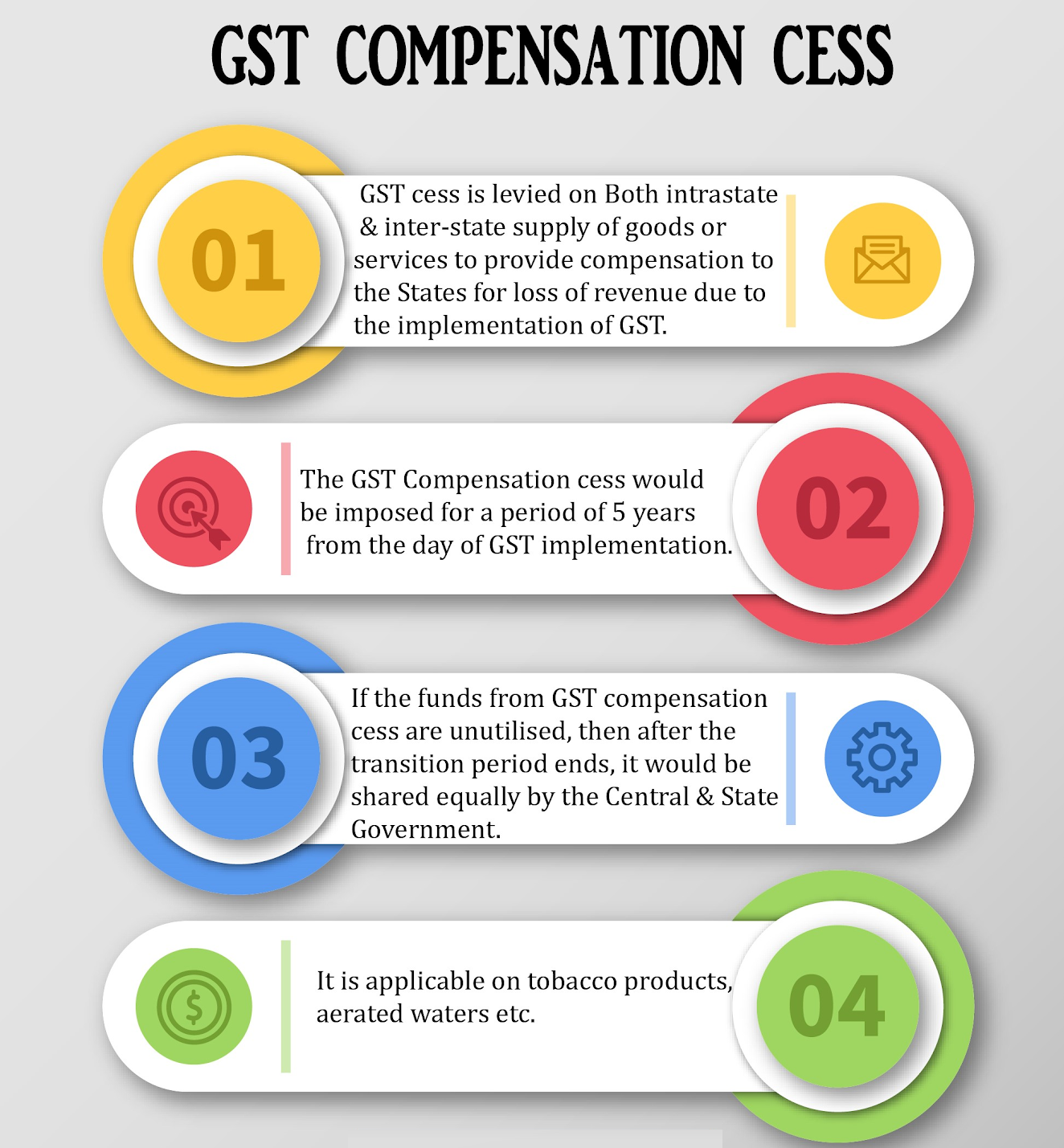

- The GST Compensation Cess.

- The Finance Minister Nirmala Sitharaman introduced a new cess — a Health Cess of 5% on imported medical devices — in the Finance Bill for 2020-2021.

Vidhi Centre For Legal Policy

- Vidhi Centre for Legal Policy is a not-for-profit company set up under Section 25 of the Companies Act, 1956 in 2013.

- It is an independent think-tank that performs legal research to make better laws and improve governance for the public good.

- The organisation has engagement with the Government of India, State governments and other public institutions to both inform policy-making and to effectively convert policy into law; and through strategic litigation petitioning courts on important law and policy issues.

Issues related to cesses

- The report by Vidhi Centre for Legal Policy, submitted to the 15th finance panel, points out that the share of cesses and surcharges (a ‘tax on tax’) in gross tax revenue (GTR) increased from 7% and 2%, respectively, in 2012-13 to 11.9% and 6.4%, respectively in 2018-19.

- In one year alone, from 2017-18 to 2018-19, the collection from cesses increased to ₹2.2 lakh crore (11.1% of GTR) to ₹2.7 lakh crore, and surcharges from ₹99,049 crore (5% of GTR) from ₹1.4 lakh crore.

- States have represented to the 15th Finance Commission that their share in gross tax revenues has fallen on account of the rising component of cesses and surcharges on which they have no rights as per the 80th Amendment to the Constitution, pertaining to Article 270.

- According to the Comptroller and Auditor General of India (CAG), while 17 cesses and other levies were subsumed into the GST, 35 levies still remained in force.

- The CAG report has also observed that for 2018-19, out of the ₹2.7 lakh crore received from such levies, only ₹1.64 lakh crore had been transferred to specific reserves and funds, the rest remaining with the Consolidated Fund of India.

- The fund of ₹1.25-lakh crore raised from the cess collected on crude oil has not been transferred to any oil industry development body, it was meant to finance.

- The new 5% Health and Education Cess on income tax was partly deployed towards education, but no fund was created for health.

Way forward

Imposition

- The government should improve efficiency in tax collection, widen the tax base and reduce reliance on such levies.

- According to Budget Estimates for 2018-19, cess collection is estimated to be 11.9% of gross tax revenue.

- This is the highest recorded percentage of cess collected as a percentage of gross tax revenue from 2002, from which time reliable data is available.

- This number may be treated as a benchmarked ceiling and no new cess should be imposed that takes the percentage beyond this ceiling.

Transparency and rationalism

- In light of evidence of diversion of funds from cesses, there must be greater transparency in cess imposition and collection.

- Budget documents and charging legislation should clearly spell out the amount that the Union Government aims to collect via the cess and how taxes simpliciter are unable to meet the required funding needs.

- Cesses must be periodically reviewed. A review will assess the amount actually collected vis-à-vis the amount utilised and compare each of these with the amount aimed to be collected.

Abolition

- Cesses garnering collections below Rs.50 crore in a financial year are economically inefficient, add to the multiplicity of taxes and fuel cascading effects.

- Hence, going forward any economically inefficient cesses should be abolished.

- Cesses shall be levied for a maximum term of 5 years which may be extended if the concerned ministry/department administering the levy is able to justify continuance and demonstrate satisfactory utilisation over the years.

Conclusion

- Not using the cess proceeds for their sole purpose amounts in short-changing the taxpayer who pays for such levies on goods, services and income in the faith that the proceeds are used for health and education, road and infrastructure, clean energy or other public goods.

- Cesses are meant for a specific purpose and period (five years in the case of GST cess), whereas they appear to be rolled over quite often, besides being allowed for use in “related purpose”.

- Given that cess does not need to be a part of the divisible pool of resources, this increasing share of cess in the Union government’s tax receipts has a direct impact on fiscal devolution.

- Absolute transparency is needed in the management of cess receipts so that Parliament and the people in order to avoid any subterfuge.

|

Drishti Mains Question Discuss the system of cess in India and how far it serves the intended purpose. |

This editorial is based on Goals and Penalties published in ‘The Indian Express’ on October 06, 2020. Now watch this on our youtube channel.