Indian Economy

Reforming the Global Sovereign Credit Rating System and MDBs

- 05 Jul 2025

- 11 min read

For Prelims: Foreign Direct Investment (FDI), GDP, Fiscal Deficit, Inflation, Balance of Payments (BoP), Foreign Reserves, GST, Insolvency and Bankruptcy Code (IBC), Debt-to-GDP, BRICS, G20, IMF.

For Mains: Concerns associated with the global sovereign credit rating system and MDBs and steps needed to reform them.

Why in News?

At the 4th International Conference on Financing for Development (FFD4) held in Seville, Spain, India’s Finance Minister advocated for reforming the global sovereign credit rating systems and multilateral development banks (MDBs) to promote equity, inclusivity, and sustainable development.

What are Multilateral Development Banks?Click Here to Read: Multilateral Development Banks |

What is the Sovereign Credit Rating System?

- About: A Sovereign Credit Rating is an independent evaluation of a country’s creditworthiness, providing investors with insights into the risk level of investing in its debt, including political risks.

- Beyond accessing external debt markets, countries seek such ratings to help attract Foreign Direct Investment (FDI).

- Credit Rating Agencies: The Big Three global rating agencies are Standard & Poor’s (S&P), Moody’s, and Fitch Ratings, all of which are based in the United States.

- Other notable agencies include DBRS (Canada), JCR (Japan), and Dagong (China).

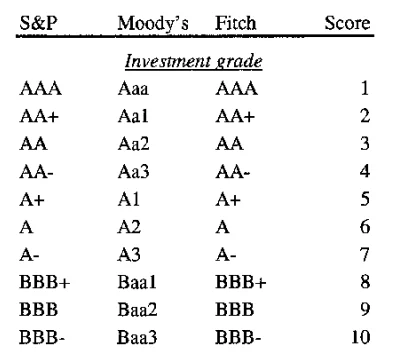

- Rating Scales: Credit ratings range from AAA (highest) to D (default).

- Ratings from AAA to BBB- (S&P/Fitch) or Aaa to Baa3 (Moody’s) are considered investment grade; anything lower is speculative or junk grade.

- Parameters Used: Sovereign credit ratings are based on key parameters such as a country’s GDP growth rate, fiscal deficit and public debt levels, inflation and monetary stability, political stability and governance, balance of payments (BoP), and foreign reserves including current account balance.

- Impact of Ratings: A higher rating lowers borrowing costs for governments and improves investor confidence.

- A downgrade raises borrowing costs and may trigger capital outflows.

- India’s Sovereign Credit Rating: India’s sovereign credit rating stands at Baa3 from Moody’s and BBB- from S&P and Fitch, all representing the lowest investment grade, though India maintains that its strong macroeconomic fundamentals warrant a higher rating.

Sovereign Credit Rating (SCR) in India

- In India, there are six credit rating agencies namely, CRISIL, ICRA, CARE, SMERA, Fitch India and Brickwork Ratings.

- Each credit rating agency uses its own methodology to assess entities like companies, governments, non-profits, and securities.

- They evaluate factors such as financial statements, debt levels, repayment history, and creditworthiness, providing investors with insights to make informed investment decisions.

- The SEBI (Credit Rating Agencies) Regulations, 1999 of the Securities and Exchange Board of India Act, 1992 govern credit rating agencies in India.

- CareEdge (parent company CARE Ratings Ltd) became the first Indian credit rating agency to enter the global scale ratings space, including sovereign ratings.

Why does India Want Reforms in the Current Sovereign Credit Rating System?

- Bias Against Developing Economies: Despite having strong macroeconomic fundamentals, India holds a BBB- rating (just above junk status), whereas countries like Italy and Spain, with weaker growth and higher debt levels, receive better credit ratings.

- For instance, Italy’s debt-to-GDP ratio is averaged 118%, yet it is rated BBB by S&P, compared to India’s BBB- (debt-to-GDP ratio is 80%).

- In December 2023, finance ministry economists had questioned the three big global rating agencies for keeping India’s rating static at the lowest investment grade for the last 15 years despite it moving up the ladder from 12th largest to become 5th largest economy.

- Flawed Debt Assessment: Despite India’s debt being largely domestic and low-risk, rating agencies assess it like foreign currency debt and often overlook India’s high growth, which makes its debt more sustainable than that of stagnant economies like Japan or the USA.

- Overemphasis on Perceptual Factors: Credit ratings often rely on subjective factors like political stability surveys, which may be biased or outdated, while India’s strong GDP growth, USD 600+ billion forex reserves, and key reforms like GST and Insolvency and Bankruptcy Code (IBC) are frequently underweighted.

- Pro-Cyclical Downgrades: During economic stress (e.g., Covid-19), agencies often downgrade countries, raising borrowing costs when funds are most needed. E.g., in 2020, Moody's downgraded India’s rating from Baa2 to Baa3 despite stimulus measures.

- Conflict of Interest: Most global rating agencies, including Moody’s, S&P, Fitch, are paid by the entities they rate, raising concerns about credibility, independence, and developed-world bias.

- There is a lack of Global South-led alternatives, limiting balanced perspectives in sovereign credit assessments.

- Failure to Predict Major Crises: Rating agencies failed to predict the 2008 financial crisis, assigning high ratings to risky assets, which damaged their credibility, yet their assessments still heavily influence global capital flows.

- They also lack transparency in sovereign rating methodologies, and the absence of a uniform global standard affects objectivity and fairness.

What are the Key Challenges Related to MDBs?Click Here to Read: Key Challenges Related to MDBs |

What Steps are Needed to Reform the Sovereign Credit Rating System?

- Greater Transparency: Rating agencies should disclose the weightage assigned to key metrics like GDP growth, debt-to-GDP, and political stability, and undergo independent audits to ensure transparency and prevent bias.

- They must also incorporate country-specific factors in their assessments, such as India’s domestic debt profile and demographic dividend.

- Increased Objectivity: Replace perception-based metrics with hard data (e.g., inflation control, forex reserves, digital infrastructure) and use AI and Big Data to integrate real-time indicators like GST collections and UPI transactions for more dynamic assessments.

- Alternative Credit Rating Agencies (CRAs): Encourage emergence of rating agencies from the Global South, including India, BRICS, or G20 nations to counter Western dominance, while also strengthening Indian agencies like CRISIL and ICRA to compete globally.

- Regulatory Oversight & Accountability: Create a global supervisory body, possibly under IMF, or G20 to audit and regulate rating practices.

- Incorporate Non-Economic Indicators: Credit ratings should include parameters like climate resilience, digital capacity, and policy reforms, broadening the focus beyond fiscal metrics to assess long-term sustainability and reform orientation.

- Promote Peer Comparability: Ratings should be updated in real time to reflect rapid macroeconomic changes, and peer comparison dashboards should be introduced to minimize perception asymmetry.

What Reforms are Necessary in MDBs?Click Here to Read: Reforms Necessary in MDBs |

Conclusion

India advocates reforming the biased sovereign credit rating system and outdated MDBs that undervalues developing economies. With strong fundamentals yet stagnant ratings and unsustainable funding, India seeks transparent, data-driven assessments and alternative agencies to counter Western dominance. Reforms must incorporate real-time indicators, climate resilience, and regulatory oversight to ensure fair global financing and reflect true economic potential.

|

Drishti Mains Question: Q. Critically analyze the limitations of the current sovereign credit rating system and suggest reforms to make it equitable for developing countries. |

UPSC Civil Services Examination, Previous Year Question (PYQ)

Prelims

Q. Consider the following statements:

- In India, credit rating agencies are regulated by the Reserve Bank of India.

- The rating agency popularly known as ICRA is a public limited company.

- Brickwork Ratings is an Indian credit rating agency.

Which of the statements given above are correct?

(a) 1 and 2 only

(b) 2 and 3 only

(c) 1 and 3 only

(d) 1, 2 and 3

Ans (b)