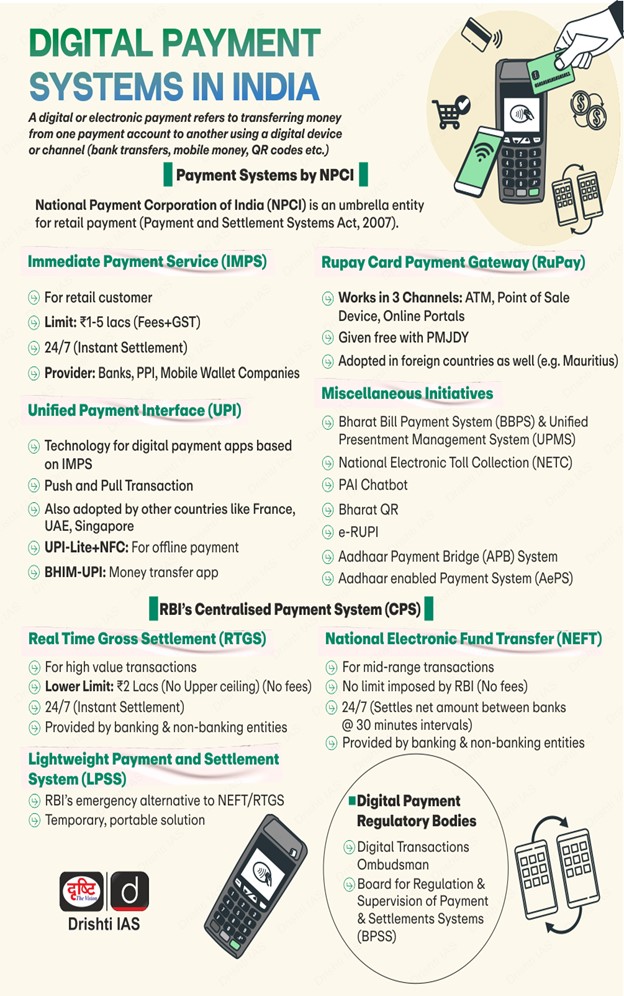

Indian Economy

Promoting Local Fintech Players

- 22 Feb 2024

- 11 min read

For Prelims: Fintech Sector, Cybersecurity, Parliament Committees, Reserve Bank of India (RBI), National Payments Corporation of India, Securities and Exchange Board of India

For Mains: India's Digital Payments Ecosystem, Capital Market

Why in News?

In a recent report presented to Parliament, the Standing Committee on Communications and Information Technology raised concerns regarding the dominance of foreign-owned fintech apps in India's digital payments ecosystem.

- Fintech is the use of digital platforms to provide financial services.

What are the Key Highlights of the Report?

- Emphasis on Effective Regulation:

- The Committee in its report emphasised that digital payment apps must be effectively regulated as the use of digital platforms to make payments in India is on the rise.

- It noted that it will be more ‘feasible’ for regulatory bodies such as the Reserve Bank of India (RBI) and the National Payments Corporation of India (NPCI) to control local apps, as compared with foreign apps, which operate in multiple jurisdictions.

- Dominance of Foreign-Owned Fintech Companies:

- Fintech companies owned by foreign entities, such as PhonePe and Google Pay, dominate the Indian fintech sector, with substantial market shares.

- Market share: PhonePe (46.91%) > Google Pay (36.39%) > BHIM UPI (0.22%) (till Oct-Nov 2023).

- Fintech companies owned by foreign entities, such as PhonePe and Google Pay, dominate the Indian fintech sector, with substantial market shares.

- NPCI's Volume Cap Regulation:

- The Committee’s recommendations are also largely in tune with the NPCI issuing a 30% volume cap on transactions facilitated using Unified Payments Interface (UPI), back in November 2020.

- The cap restricts individual third-party apps like PhonePe and Amazon Pay from exceeding 30% of total UPI transactions over three months.

- Apps exceeding the cap were given a two-year phased compliance period (Dec 2022- Dec 2024).

- The purpose of the cap is to mitigate risks and safeguard the UPI ecosystem during its expansion.

- NCPI emphasized the importance of enhancing consumer outreach by banks and non-banks to foster UPI growth and achieve market equilibrium.

- The Committee’s recommendations are also largely in tune with the NPCI issuing a 30% volume cap on transactions facilitated using Unified Payments Interface (UPI), back in November 2020.

- Fraud Concerns:

- The Committee highlights concerns about fintech platforms being exploited for money laundering, citing instances like the Abu Dhabi-based app Pyppl being administered by Chinese investment scamsters.

- The fraud-to-sales (F2S) ratio has largely remained around 0.0015% despite the rise in volume of the payment mode in the last five years.

- The percentage of users affected by UPI frauds stood at 0.0189%.

- A F2S is a volume-based percentage that measures the number of fraudulent transactions a business processes in a given month compared to their monthly sales volume.

What is Fintech?

- About:

- Fintech, or financial technology, is the use of digital platforms, software, and services to provide or facilitate financial services, such as payments, lending, insurance, wealth management, and more.

- Importance:

- Fintech is important for India because it can help in:

- Expanding the access and inclusion of financial services to the large unbanked and underbanked population in India, especially in rural and remote areas.

- Enhancing the efficiency and convenience of financial transactions, by reducing the cost, time, and friction involved in traditional methods.

- Fostering the innovation and growth of the Indian economy, by creating new opportunities and markets for entrepreneurs, startups, and consumers.

- Fintech is important for India because it can help in:

- Segments and Trends of the Fintech Sector in India:

- Major segments under Fintech include Payments, Digital Lending, InsurTech, WealthTech.

- Digital payments, which enable the transfer of money or value through online or mobile platforms, such as UPI, wallets, cards, and QR codes.

- Digital lending, which provides loans or credit to individuals or businesses through online or mobile platforms, using alternative data sources and algorithms.

- Insurtech, which applies technology to improve the distribution, delivery, and management of insurance products and services.

- Wealthtech, which offers online or mobile platforms for investment, wealth management, and financial advisory services

- India is amongst the fastest growing Fintech markets in the world. It is home to over 7,000 fintech start-ups.

- The Indian FinTech industry’s market size is USD 50 Bn in 2021 and is estimated at ~ USD 150 Bn by 2025.

- Major segments under Fintech include Payments, Digital Lending, InsurTech, WealthTech.

- Key Regulatory Bodies for Fintech in India:

- Reserve Bank of India (RBI):

- Regulates banks, NBFCs, PSPs, and credit bureaus.

- Responsible for regulating India’s money market and foreign exchange market.

- Oversees fintech sectors like Digital Payments, Digital Lending, and Digital or neo-banks.

- Securities and Exchange Board of India (SEBI):

- Regulates securities markets and intermediaries such as stockbrokers and investment advisors.

- Services like stockbroking and investment advisory fall under its jurisdiction.

- Insurance Regulatory and Development Authority of India (IRDAI):

- Regulates insurers, corporate agents, web aggregators for insurance, and third-party agents for insurance.

- Ensures compliance and integrity in the insurance sector.

- Reserve Bank of India (RBI):

What are the Challenges Faced by Local Fintech Players?

- Fierce Competition:

- The Indian fintech space is highly competitive, with numerous local and foreign players vying for market share. This intense competition can make it difficult for local players to stand out and acquire a significant user base.

- Local players often face competition from established global fintech giants with vast resources and experience. These giants can leverage their brand recognition and technological prowess to attract customers and gain a competitive edge.

- The Indian fintech space is highly competitive, with numerous local and foreign players vying for market share. This intense competition can make it difficult for local players to stand out and acquire a significant user base.

- Regulatory Hurdles:

- The Indian regulatory landscape for fintech is constantly evolving, making it challenging for local players to keep up with compliance requirements.

- Navigating these complexities can be time-consuming and resource-intensive, especially for smaller startups.

- Growing concerns around data privacy and security pose challenges for local players. They need to invest in robust data security measures and ensure compliance with data privacy regulations like the Personal Data Protection to gain user trust.

- The Indian regulatory landscape for fintech is constantly evolving, making it challenging for local players to keep up with compliance requirements.

- Financial Constraints:

- Compared to their foreign counterparts, local players often have limited access to funding, hindering their ability to invest in new technologies, expand their reach, and compete effectively.

- While instant payments like UPI have revolutionised the Indian market, their minimal transaction fees can limit revenue generation for local players, especially those solely relying on this segment.

- McKinsey's report (2023) suggests that instant payments in India may contribute less than 10% of future revenue growth.

- This projection is due to the absence of fees charged for transactions made through the UPI, while UPI imposes minimal transaction fees, it still generates more revenue compared to fee-less cash transactions.

- Paperless transactions enhance security and accessibility to digital commerce, compared to costly cash management.

- This projection is due to the absence of fees charged for transactions made through the UPI, while UPI imposes minimal transaction fees, it still generates more revenue compared to fee-less cash transactions.

- Compared to their foreign counterparts, local players often have limited access to funding, hindering their ability to invest in new technologies, expand their reach, and compete effectively.

- Technological Limitations:

- Rapid technological advancements in the global fintech landscape can be challenging for local players to keep pace with. They need to continuously invest in research and development to stay competitive and offer innovative solutions.

- Lack of access to advanced technological infrastructure, such as robust internet connectivity in rural areas, can hinder the reach and inclusivity of local fintech solutions.

- Rapid technological advancements in the global fintech landscape can be challenging for local players to keep pace with. They need to continuously invest in research and development to stay competitive and offer innovative solutions.

- Customer Trust and Behaviour:

- Establishing trust with users, especially in rural areas, can be challenging due to concerns about digital literacy, data security, and potential scams. Local players need to invest in user education and build trust through transparent practices.

Way Forward

- Local and Foreign Fintech Players:

- A balanced mix of Local and Foreign Fintech Players is essential to serve diverse areas like payments, lending, wealth management, and insurance.

- The optimal mix should balance the interests and needs of the Indian ecosystem, which includes the customers, the providers, the regulators, and the society.

- A balanced mix of Local and Foreign Fintech Players is essential to serve diverse areas like payments, lending, wealth management, and insurance.

- Enhanced Regulatory Engagement:

- Local fintech players should actively engage with regulatory bodies to understand evolving compliance requirements and ensure adherence to regulations.

- Collaboration with regulators can help streamline accountability and compliance processes and foster a conducive regulatory environment for innovation and growth.

- User Experience:

- Design user-friendly interfaces and functionalities that are accessible and cater to varying levels of digital literacy, especially in rural areas.

- Access to funding:

- Explore initiatives to facilitate easier access to funding for local players, such as venture capital investments or government grants, which can help them compete effectively.

- Customer Trust:

- Focus on education, transparent communication, and robust security measures to build trust.

UPSC Civil Services Examination, Previous Year Questions (PYQs)

Q. With reference to India, consider the following: (2010)

- Nationalisation of Banks

- Formation of Regional Rural Banks

- Adoption of village by Bank Branches

Which of the above can be considered as steps taken to achieve the “financial inclusion” in India?

(a) 1 and 2 only

(b) 2 and 3 only

(c) 3 only

(d) 1, 2 and 3

Ans: (d)