Indian Economy

FinTech In India

- 08 Dec 2020

- 8 min read

This article is based on “Realising India’s fintech potential: Regulation and tech must evolve” which was published in The Economic Times on 07/12/2020. It talks about the active areas, opportunities and associated challenges of Fintech in India.

Recently, India has overtaken China as Asia’s top financial technology (FinTech) market. Having emerged as the world’s second-largest fin-tech hub (trailing only the US), India is experiencing the ‘FinTech Boom’.

Fintech is used to describe new technology that seeks to improve and automate the delivery and use of financial services. The key segments within the FinTech space include Digital Payments, Digital Lending, BankTech, InsurTech and RegTech, Cryptocurrency.

FinTech now includes different sectors and industries such as education, retail banking, fundraising and nonprofit, and investment management to name a few. FinTech is amongst the most thriving sectors at present in terms of both business growth and employment generation. Apart from this, FinTech can also help in the furtherance of the goal of financial inclusion.

Active Areas of FinTech Innovation

- Cryptocurrency and digital cash.

- Blockchain technology, that maintains records on a network of computers, but has no central ledger.

- Smart contracts, which utilize computer programs (often utilizing the blockchain) to automatically execute contracts between buyers and sellers.

- Open banking, a concept that leans on the blockchain and posits that third-parties should have access to bank data to build applications that create a connected network of financial institutions and third-party providers.

- Insurtech, which seeks to use technology to simplify and streamline the insurance industry.

- Regtech, which seeks to help financial service firms meet industry compliance rules, especially those covering Anti-Money Laundering and Know Your Customer protocols which fight fraud.

- Cybersecurity, given the proliferation of cybercrime and the decentralized storage of data, cybersecurity and fintech are intertwined.

Key Growth Drivers of FinTech in India

- Widespread identity formalisation (Aadhar): 1.2 bn enrolments.

- High level of banking penetration through the Jan Dhan Yojana: 1+ bn bank accounts.

- High smartphone penetration: 1.2 bn mobile subscribers.

- India Stack: Set of APIs for businesses and startups.

- Growing disposable income of Indians.

- Key government initiatives such as UPI and Digital India.

- Wide middle-class expansion: By 2030, India will add 140 mn middle-income and 21 mn high-income households which will drive the demand and growth in the Indian FinTech space.

Opportunities Related to FinTech

- Driving Financial Inclusion in India: A significant number of people in India remain outside the purview of the formal financial system.

- Use of financial technologies can help address the gaps in financial inclusion left by the traditional models of banking and finance.

- Providing Financial Assistance to the MSMEs: Lack of capital is one of the biggest threats to their existence. According to the IFC Report, the total addressable credit gap in the MSME segment is estimated to USD 397.5 billion.

- This is where FinTech comes into the picture, and has the potential to solve the credit availability issues.

- With several FinTech start-ups offering easier and quicker access to loans, MSMEs are no longer required to go through the tedious process of documentation, paperwork and multiple visits to a bank.

- Enhancing Customer Experience and Transparency: FinTech start-ups offer convenience, personalisation, transparency, accessibility and ease of use – factors that empower customers to a great extent.

- The FinTech industry will develop unique and innovative models for assessing risks.

- Leveraging big data, machine learning, and alternative data to underwrite credit and develop credit scores for customers with a limited credit history will improve the penetration of financial services in India.

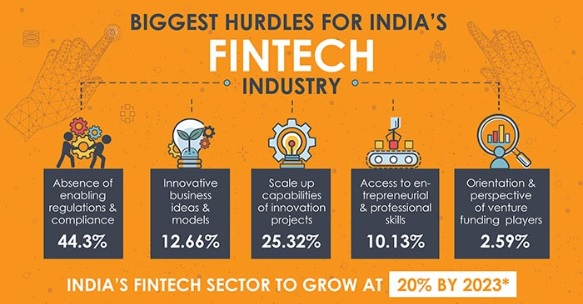

Associated Challenges

- Cyber-Attacks: Automation of processes and digitization of data makes fintech systems vulnerable to attacks from hackers.

- Recent instances of hacks at debit card companies and banks are illustrations of the ease with which hackers can gain access to systems and cause irreparable damage.

- Data Privacy Issue: The most important questions for consumers pertain to the responsibility for cyber attacks as well as misuse of personal information and important financial data.

- Difficulty in Regulation: Regulation is also a problem in the emerging world of FinTech, especially cryptocurrencies.

- In most countries, they are unregulated and have become fertile ground for scams and frauds.

- Due to the diversity of offerings in FinTech, it is difficult to formulate a single and comprehensive approach to these problems.

Way Forward

- Guarding Against Cybercriminals: Currently, India majorly relies on import of offensive as well as defensive cybersecurity capabilities. Given the growing scale of adoption of technology, it is imperative for India to attain Atma-Nirbharta (Self-Sufficiency) in this domain.

- Educating Consumers: Apart from establishing technological safeguards, educating and training customers to spread awareness about the benefits of fintech and guard against cyberattacks will also help in democratisation of FinTech.

- Data Protection Law: Established fintech sandboxes by RBI to evaluate the implications of technology in the sector is a step in the right direction.

- However, there is a requirement for a strong data protection framework in India.

- In this context, the personal data protection bill, 2019, must be passed after thorough debate and deliberation.

Conclusion

Fintech has the potential to transform other financial services like insurance, investment, remittances. However, regulation must help, not hinder its evolution.

|

Drishti Mains Question Development of financial technology (FinTech) in India can help in the furtherance of the goal of financial inclusion. Critically analyse. |

This editorial is based on “A boost for defence ties in West Asia” which was published in The Hindustan Times on December 7th, 2020. Now watch this on our Youtube channel.