Indian Economy

Sabka Bima, Sabki Raksha Bill, 2025

- 19 Dec 2025

- 15 min read

For Prelims: Insurance, Insurance Regulatory and Development Authority of India (IRDAI), Foreign Direct Investment, Pradhan Mantri Jan Dhan Yojana, Atal Pension Yojana, Suraksha Bima Yojana

For Mains: Liberalisation of the insurance sector and its impact on financial inclusion, Role of FDI in strengthening India’s financial sector

Why in News?

The Lok Sabha has passed the Sabka Bima, Sabki Raksha (Amendment of Insurance Laws) Bill, 2025, proposing to raise the Foreign Direct Investment (FDI) limit in the insurance sector from 74% to 100%.

- The move is positioned as a key reform to deepen insurance coverage and advance the goal of “Insurance for All by 2047.”

Summary

- The Sabka Bima, Sabki Raksha Bill, 2025 allows 100% FDI in insurance, strengthens IRDAI’s regulatory powers, liberalises reinsurance, and aims to accelerate insurance penetration under the vision of “Insurance for All by 2047.”

- While the reform can attract global capital, technology, and innovation to India’s growing insurance market, concerns remain over foreign dominance, rural neglect, and the need to balance investor interests with policyholder protection.

What are the Key Provisions of the Sabka Bima, Sabki Raksha (Amendment of Insurance Laws) Bill, 2025?

- 100% FDI in Insurance: The Bill raises the foreign direct investment limit in insurance companies from 74% to 100%, allowing full foreign ownership to attract long-term capital, advanced technology, and global best practices.

- Amendments to Insurance Laws: It updates the Insurance Act, 1938, LIC Act, 1956, and Insurance Regulatory and Development Authority (IRDA) Act, 1999 to reflect sectoral reforms and regulatory strengthening.

- Reinsurance Liberalisation: The Net Owned Fund requirement of Foreign Reinsurance Branches is reduced from Rs 5,000 crore to Rs 1,000 crore, this aims to deepen the reinsurance market and promote India as a regional hub.

- Net Own Funds (NOF) refers to the minimum capital that a reinsurance entity must maintain as a financial buffer to ensure solvency and meet claim obligations.

- Policyholders’ Education and Protection Fund: It will be set up to promote insurance awareness and safeguard consumer interests, while policyholders’ data must be collected and protected in line with the Digital Personal Data Protection (DPDP) Act, 2023.

- Stronger Powers for IRDAI: The Bill significantly enhances IRDAI’s enforcement authority, enabling it to investigate violations, curb illegal commissions and rebates, and ensure stricter compliance by insurers and intermediaries.

- The IRDAI Chairperson can order searches, inspections, and seizures where records are withheld or tampered with.

- IRDAI can deploy officers to scrutinise returns, statements, and disclosures submitted by insurers, improving transparency and regulatory vigilance.

- Greater Autonomy for LIC: LIC is granted operational freedom to open new zonal offices without prior government approval, enabling quicker expansion and better regional management.

- Eased Compliance Regime: Procedural and compliance requirements are simplified to improve ease of doing business while maintaining consumer protection.

Limitations of Sabka Bima, Sabki Raksha (Amendment of Insurance Laws) Bill, 2025

- Critics argue that allowing 100% foreign ownership places citizens’ long-term savings in the hands of foreign corporations, raising concerns about national control over household financial security.

- There are worries that foreign insurers could prioritise profit repatriation and urban markets, neglecting rural and social sector needs.

- Critics also point to a trust deficit, as insurance relies heavily on public confidence in state-backed institutions.

- Also, the reform is perceived as a recalibration of the state’s role in social risk protection, with greater emphasis on shared responsibility rather than direct state provision.

Key Government Initiatives to Promote Insurance Penetration in India

- Pradhan Mantri Jan Arogya Yojana (PM-JAY): The largest health assurance scheme in the world, it provides health insurance cover of Rs 5 lakh per family per year for secondary and tertiary care to vulnerable households.

- Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY): It is a life insurance scheme providing coverage for death due to any cause. The eligible age to join the scheme is 18 to 50 years.

- Pradhan Mantri Suraksha Bima Yojana (PMSBY): An Accident Insurance Scheme offering accidental death and disability cover for death or disability on account of an accident.

- Jan Dhan–Aadhaar–Mobile (JAM) Trinity: Enables easy enrolment, premium payment, and direct benefit transfers, expanding insurance access.

What is the State of the Indian Insurance Sector?

- Market Size and Global Position: India is currently the 10th largest insurance market globally and the 2nd largest among emerging markets, with a market share of about 1.9%.

- As per Swiss Re, India is expected to become the 6th largest insurance market by 2032, overtaking major developed economies.

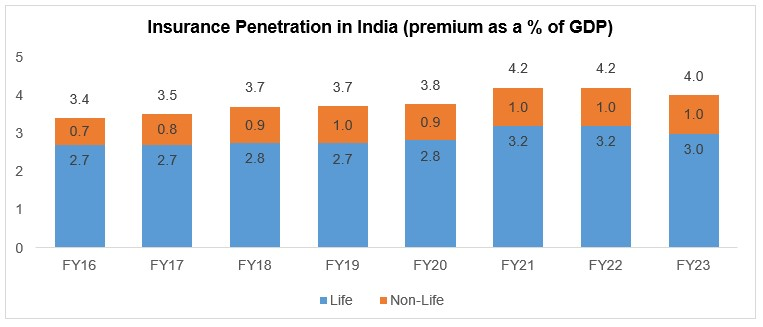

- Penetration and Density: Insurance penetration in India has been in a growing momentum from 3.4% in FY16 to 4.0% in FY23.

- The general insurance density (the per capita premium) rose from USD 9 in 2019 to USD 25 in FY23.

- The number of insurers rose from 53 in 2014–15 to 74 in 2024–25, reflecting deeper market participation.

- Total insurance premiums nearly tripled from Rs 4.15 lakh crore to Rs 11.93 lakh crore over the same period.

- Life Insurance Segment: India is the 5th largest life insurance market globally, growing at 32-34% annually.

- LIC remains as the largest player with around 60% market share, but private insurers are steadily gaining ground.

- Non-Life (General) Insurance Segment: India is currently the 4th largest general insurance market in Asia and the 14th-largest globally.

What are the Key Challenges in India’s Insurance Sector?

- Low Insurance Penetration: General insurance penetration in India remains relatively low at 1% of GDP, compared to a global average of 4.2% in 2023.

- Limited Rural and Informal Coverage: Urban and salaried segments dominate coverage, while rural areas, MSMEs, gig workers, and the unorganised workers remain largely uninsured.

- Product Mismatch: Insurance products are often complex and poorly tailored to the needs of low-income households and small businesses.

- Many products remain generic and poorly aligned with emerging risks like climate events, cyber risks, and pandemic-related losses.

- Mis-selling and Trust Deficit: Product complexity, opaque terms, delayed claim settlements, mis-selling by intermediaries, and complex policy terms weaken consumer confidence and lead to high grievance volumes.

- Limited Awareness: Large sections of the population still view insurance as an expense rather than a risk-management tool.

What Measures Needed to Strengthen India’s Insurance Sector?

- Leverage Technology and Digital Public Infrastructure: Encourage adoption of RegTech and SupTech tools for real-time compliance monitoring and risk assessment.

- Enhance the integration of insurance with India Stack (Aadhaar, e-KYC, DigiLocker, UPI) for faster onboarding, premium collection, and claim settlement.

- Use AI and data analytics for fraud detection, underwriting, and personalised products.

- Encourage Product Innovation and Risk Coverage: Promote insurance products for emerging risks such as cyber security, climate disasters, health pandemics, and supply-chain disruptions.

- Encourage usage-based and on-demand insurance, especially in motor and health segments.

- Align insurance growth with India’s goals of financial inclusion, climate resilience, and infrastructure financing.

- Deepen Insurance Penetration and Inclusion: Scale up social insurance schemes such as PMJJBY, PMSBY, PMFBY, and Ayushman Bharat to cover informal workers, gig economy participants, and MSMEs.

- Promote micro-insurance and parametric insurance for farmers, coastal communities, and climate-vulnerable regions.

- Use Self-Help Groups, PACS, CSCs, and post offices as last-mile insurance distributors.

- Policy Imperative: As India opens the insurance sector to foreign participation, the Insurance Amendment Bill must be backed by tighter regulation and vigilant oversight to safeguard policyholders and ensure market stability.

Conclusion

Allowing 100% FDI in insurance marks a bold and mature step in India’s financial sector reforms. It addresses the supply-side challenge of capital and expertise. The reform’s success will depend on strong regulation and the ability to balance investor interests with the protection of Indian policyholders.

|

Drishti Mains Question: “Raising FDI in insurance to 100% addresses supply-side constraints but not demand-side barriers.” Examine in the context of India’s insurance sector. |

Frequently Asked Questions (FAQs)

Q. What is the Sabka Bima, Sabki Raksha (Amendment of Insurance Laws) Bill, 2025?

It amends key insurance laws to allow 100% FDI, strengthen IRDAI’s powers, liberalise reinsurance, and improve consumer protection.

Q. Why is the 100% FDI provision significant for India’s insurance sector?

It enables full foreign ownership, attracting long-term capital, global best practices, and advanced risk management expertise.

Q. How does the Bill strengthen IRDAI?

It grants IRDAI enhanced enforcement powers, including inspections, investigations, and action against illegal commissions and violations.

UPSC Civil Services Examination Previous Year Questions (PYQ)

Prelims

Q. In India, under cyber insurance for individuals, which of the following benefits are generally covered, in addition to payment for the loss of funds and other benefits? (2020)

- Cost of restoration of the computer system in case of malware disrupting access to one’s computer

- Cost of a new computer if some miscreant wilfully damages it, if proved so

- Cost of hiring a specialized consultant to minimize the loss in case of cyber extortion

- Cost of defence in the Court of Law if any third party files a suit

Select the correct answer using the code given below:

(a) 1, 2 and 4 only

(b) 1, 3 and 4 only

(c) 2 and 3 only

(d) 1, 2, 3 and 4

Ans: (b)

Q. Consider the following statements: (2020)

- Aadhaar metadata cannot be stored for more than three months.

- State cannot enter into any contract with private corporations for sharing of Aadhaar data.

- Aadhaar is mandatory for obtaining insurance products.

- Aadhaar is mandatory for getting benefits funded out of the Consolidated Fund of India.

Which of the statements given above is/are correct?

(a) 1 and 4 only

(b) 2 and 4 only

(c) 3 only

(d) 1, 2 and 3 only

Ans: (b)

Mains

Q. Public health system has limitations in providing universal health coverage. Do you think that private sector could help in bridging the gap? What other viable alternatives would you suggest? (2015)

Q. The product diversification of financial institutions and insurance companies,resulting in overlapping of products and services strengthens the case for the merger of the two regulatory agencies, namely SEBI and IRDA. Justify. (2013)