Indian Economy

External Benchmark Rates

- 05 Sep 2019

- 6 min read

The Reserve Bank of India has made it mandatory for all banks to link all new floating rate loans (i.e. personal/retail loans, loans to MSMEs) to an external benchmark with effect from 1st October 2019. The move is aimed at faster transmission of monetary policy rates.

- Banks can choose from one of the four external benchmarks — repo rate, three-month treasury bill yield, six-month treasury bill yield or any other benchmark interest rate published by Financial Benchmarks India Private Ltd.

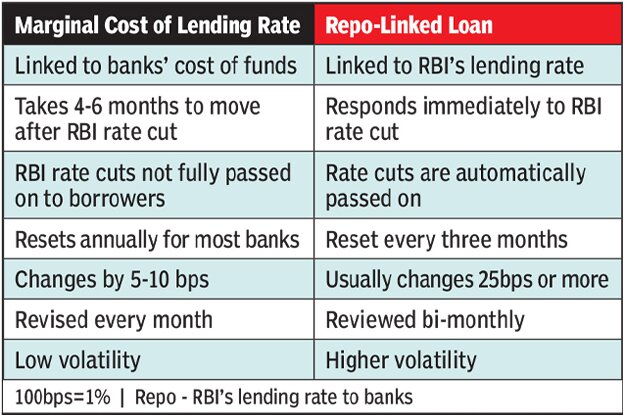

- At present, interest rates on loans are linked to a bank’s marginal cost of fund-based interest rate, known as the Marginal Cost of Lending Rate (MCLR).

- Existing loans and credit limits linked to the MCLR, base rate or Benchmark Prime Lending Rate, would continue till repayment or renewal.

- Those customers wanting to switch to the repo-linked rate can do so on mutually acceptable terms.

- Adoption of multiple benchmarks by the same bank is not allowed within a loan category.

- The interest rate under the external benchmark shall be reset at least once every three months.

Fixed vs Floating Interest Rate

- The fixed interest rate on loan means repayment of loans in fixed equal instalments over the entire period of the loan. In this case, the interest rate doesn't change with market fluctuations.

- Floating interest rate by name implies that the rate of interest varies with market conditions. The drawback with floating interest rates is the uneven nature of monthly instalments.

Financial Benchmarks India Private Ltd

- It was incorporated on 9th December 2014 under the Companies Act 2013.

- It was recognised by the Reserve bank of India as an independent Benchmark administrator on 2nd July 2015.

- The main objective of the company is to act as the administrators of the Indian interest rate and foreign exchange benchmarks and to introduce and implement policies and procedures to handle the benchmarks.

- It is located in Mumbai.

Background

- The transmission of policy rate changes to the lending rate of banks under the current MCLR framework has not been satisfactory.

- RBI in its August Policy, 2019 pointed out that although it had brought down the repo rate by 75 basis points, the weighted average MCLR of banks had come down by only 29 basis points.

- Banks argue that the MCLR formula is calculated based on the cost of funds and thus it comes down only gradually after a repo rate cut.

- There is a strong likelihood that RBI will cut rates further to spur demand.

- The external benchmark was first proposed by the former governor Urjit Patel in 2018. The norms for external benchmark linking of interest rates was scheduled to be operational from April 1, but owing to protest by the banks, the same was deferred.

Key Terms

- Marginal Cost of Lending Rate: It came into effect in April 2016.

- It is a benchmark lending rate for floating-rate loans.

- This is the minimum interest rate at which commercial banks can lend.

- This rate is based on four components—the marginal cost of funds, negative carry on account of cash reserve ratio, operating costs and tenor premium.

- MCLR is linked to the actual deposit rates. Hence, when deposit rates rise, it indicates the banks are likely to hike MCLR and lending rates are set to go up.

- Base Rate: Banks stopped lending on base rate from April 2016.

- Loans taken between June 2010 and April 2016 from banks were on base rate.

- During the period, base rate was the minimum interest rate at which commercial banks could lend to customers.

- Base rate is calculated on three parameters — the cost of fund, unallocated cost of resources and return on net worth. Hence, the rate depended on individual banks and they changed it whenever their cost of funds and other parameters changed.

- Benchmark Prime Lending Rate: BPLR was used as benchmark rate by banks for lending till June 2010.

- Under it, bank loans were priced on the actual cost of funds.

- However, the BPLR was subverted, resulting in an opaque system. The bulk of wholesale credit (loans to corporate customers) was contracted at sub-BPL rates and it comprised nearly 70% of all bank credit.

- Under this system, banks were subsidising corporate loans by charging high interest rates from retail and small and medium enterprise customers.