Indian Economy

Privatisation of Banks

- 11 Feb 2021

- 7 min read

Why in News

The Union Budget 2021 has announced the privatisation of two public sector banks and one general insurance company in the upcoming fiscal 2021-22.

- The move, coming after 51 years of nationalisation of government-owned banks in 1969, will give the private sector a key role in the banking sector.

- Presently, India has 22 private banks and 10 small finance banks.

Key Points

- Background:

- The government decided to nationalise the 14 largest private banks in 1969. The idea was to align the banking sector with the socialistic approach of the then government.

- State Bank of India (SBI) had been nationalised in 1955 itself, and the insurance sector in 1956.

- Various governments in the last 20 years were for and against privatisation of Public Sector Undertaking (PSU) banks. In 2015, the government had suggested privatisation but the then Reserve Bank of India (RBI) Governor did not favour the idea.

- The current steps of privatisation, along with setting up an Asset Reconstruction Company (Bad Bank) entirely owned by banks, underline an approach of finding market-led solutions to challenges in the financial sector.

- The government decided to nationalise the 14 largest private banks in 1969. The idea was to align the banking sector with the socialistic approach of the then government.

- Reason for Privatisation:

- Degrading Financial Position of Public Sector Banks:

- Years of capital injections and governance reforms have not been able to improve the financial position of public sector banks significantly.

- Many of them have higher levels of stressed assets than private banks, and also lag the latter on profitability, market capitalisation and dividend payment record.

- Part of a Long-Term Project:

- Privatisation of two public sector banks will set the ball rolling for a long-term project that envisages only a handful of state-owned banks, with the rest either consolidated with strong banks or privatised.

- The initial plan of the government was to privatise four. Depending on the success with the first two, the government is likely to go for divestment in another two or three banks in the next financial year.

- This will free up the government, the majority owner, from continuing to provide equity support to the banks year after year.

- Through a series of moves over the last few years, the government is now left with 12 state-owned banks, from 28 earlier.

- Privatisation of two public sector banks will set the ball rolling for a long-term project that envisages only a handful of state-owned banks, with the rest either consolidated with strong banks or privatised.

- Strengthening Banks:

- The government is trying to strengthen the strong banks and also minimise their numbers through privatisation to reduce its burden of support.

- Recommendations of Different Committees:

- Many committees had proposed bringing down the government stake in public banks below 51%:

- The Narasimham Committee proposed 33%.

- The P J Nayak Committee suggested below 50%.

- An RBI Working Group recently suggested the entry of business houses into the banking sector.

- Many committees had proposed bringing down the government stake in public banks below 51%:

- Degrading Financial Position of Public Sector Banks:

- Selection of Banks:

- The two banks that will be privatised will be selected through a process in which NITI Aayog will make recommendations, which will be considered by a core group of secretaries on disinvestment and then the Alternative Mechanism (or Group of Ministers).

- Issues with PSU Banks:

- High Non-Performing Assets (NPAs):

- After a series of mergers and equity injections by the government, the performance of public sector banks has shown improvement over the last couple of years. However, compared with private banks, they continue to have high NPAs and stressed assets although this has started declining.

- Impact of Covid:

- After the Covid-related regulatory relaxations are lifted, banks are expected to report higher NPAs and loan losses.

- As per the RBI’s recent Financial Stability Report, gross NPA ratio of all commercial banks may increase from 7.5% in September 2020 to 13.5% by September 2021.

- This would mean the government would again need to inject equity into weak public sector banks.

- After the Covid-related regulatory relaxations are lifted, banks are expected to report higher NPAs and loan losses.

- High Non-Performing Assets (NPAs):

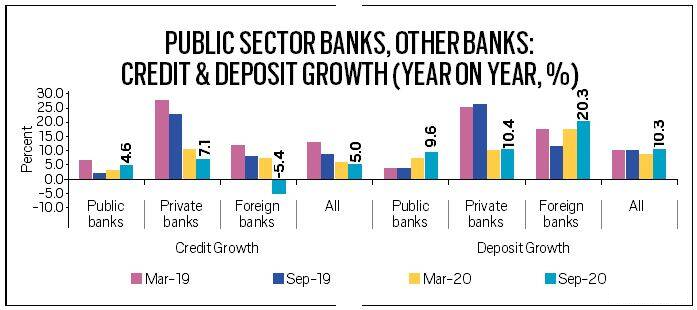

- Performance of Private Banks:

- Rising Market Share:

- Private banks’ market share in loans has risen to 36% in 2020 from 21.26% in 2015, while public sector banks’ share has fallen to 59.8% from 74.28%.

- Better Products and Services:

- Competition heated up after the RBI allowed more private banks since the 1990s. They have expanded the market share through new products, technology, and better services, and also attracted better valuations in stock markets.

- HDFC Bank (set up in 1994) has a market capitalisation of Rs. 8.80 lakh crore while SBI commands just Rs. 3.50 lakh crore.

- Competition heated up after the RBI allowed more private banks since the 1990s. They have expanded the market share through new products, technology, and better services, and also attracted better valuations in stock markets.

- Rising Market Share:

- Issues with Private Banks:

- Governance Issues:

- Industrial Credit and Investment Corporation of India (ICICI) Bank MD and CEO was sacked for allegedly extending dubious loans.

- Yes Bank CEO was not given extension by the RBI and now faces investigations by various agencies.

- Lakshmi Vilas Bank faced operational issues and was recently merged with DBS Bank of Singapore.

- Under-reported NPAs:

- When the RBI ordered an asset quality review of banks in 2015, many private sector banks, including Yes Bank, were found under-reporting NPAs.

- Governance Issues:

Way Forward

- In order to improve the governance and management of PSBs, there is a need to implement the recommendations of the PJ Nayak committee.

- Rather than blind privatisation, PSBs can be made into a corporation like Life Insurance Corporation (LIC). While maintaining government ownership, this will give more autonomy to PSBs.