Union Budget 2026–27 | 02 Feb 2026

For Prelims: Union Budget, Biosimilars, Electronics Components Manufacturing Scheme, Rare Earth Permanent Magnets, Carbon Capture, Utilization, and Storage, Orange Economy, Securities Transaction Tax (STT)

For Mains: Role of Budget in Economic Growth and Fiscal Consolidation, Manufacturing-led Growth and Atmanirbhar Bharat, Capex-led Growth vs Employment Generation, Critical Minerals and Strategic Autonomy

Why in News?

The Union Minister of Finance and Corporate Affairs presented the Union Budget 2026–27 in Parliament, marking the first Budget prepared in the newly inaugurated Kartavya Bhawan.

- The budget framed as a Yuva Shakti-driven Budget, is anchored in the vision of Viksit Bharat and reflects the guiding principles of Action over Ambivalence, Reform over Rhetoric, and People over Populism.

- The Budget is guided by three Kartavyas (duties) aimed at accelerating economic growth, building people’s capacities, and ensuring inclusive development.

The Three Kartavyas

- Sustain Economic Growth: To enhance productivity, competitiveness, and build resilience against volatile global dynamics.

- Fulfill Aspirations: To build the capacity of the youth and citizens, making them strong partners in India’s prosperity.

- Sabka Saath, Sabka Vikas: To ensure every family, community, region, and sector has access to resources and opportunities, focusing on the "Last Mile."

What are the Key Highlights of the Union Budget 2026-27?

First Kartavya: Accelerate & Sustain Economic Growth

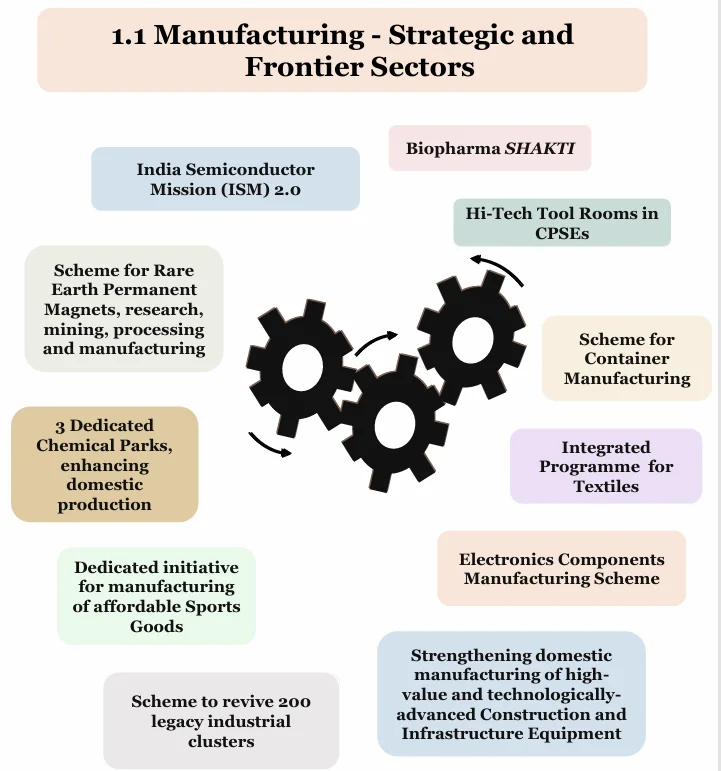

- Manufacturing & Industry (Strategic Sectors): To position India as a global manufacturing hub, the budget focuses on 7 Strategic and Frontier Sectors:

- Biopharma SHAKTI: To position India as a global hub, the Government proposed the "Biopharma SHAKTI" (Strategy for Healthcare Advancement through Knowledge, Technology and Innovation) mission with an outlay of Rs 10,000 crore over five years to develop India as a global biopharma manufacturing centre.

- It focuses on biologics and biosimilars, supported by 3 new National Institutes of Pharmaceutical Education and Research (NIPERs), upgradation of 7 existing institutes, and strengthening of CDSCO to global standards.

- India Semiconductor Mission 2.0: Building on ISM 1.0, the Union Budget 2026–27 announces India Semiconductor Mission (ISM) 2.0 to advance technological sovereignty.

- It focuses on manufacturing semiconductor equipment and materials and strengthening resilient supply chains, with industry-led R&D and training centres to create a skilled workforce critical for economic and national security.

- Electronics Components Manufacturing: The Electronics Components Manufacturing Scheme outlay is increased from Rs 22,919 crore to Rs 40,000 crore to deepen domestic value chains and boost electronics manufacturing.

- Rare Earth Corridors & Chemical Parks: The Budget proposes Rare Earth Corridors in Odisha, Kerala, Andhra Pradesh, and Tamil Nadu for mining, processing, and manufacturing of Rare Earth Permanent Magnets (REPM), along with three Chemical Parks under a cluster-based, plug-and-play model to reduce import dependence.

- Capital Goods & Container Manufacturing: The Budget announces Hi-Tech Tool Rooms by Central Public Sector Enterprises (CPSEs), a Construction and Infrastructure Equipment (CIE) Scheme, and a Rs 10,000 crore Container Manufacturing Scheme to strengthen domestic capital goods and logistics manufacturing.

- Textile Sector Push: An Integrated Textile Programme comprising the National Fibre Scheme, Samarth 2.0, Tex-Eco Initiative, and cluster modernisation is launched, along with Mega Textile Parks to promote technical textiles and value addition.

- Gram Swaraj & Sports Goods: The Mahatma Gandhi Gram Swaraj initiative aims to strengthen khadi, handloom, and handicrafts, while a sports goods manufacturing initiative seeks to position India as a global hub for affordable, high-quality sports equipment.

- Biopharma SHAKTI: To position India as a global hub, the Government proposed the "Biopharma SHAKTI" (Strategy for Healthcare Advancement through Knowledge, Technology and Innovation) mission with an outlay of Rs 10,000 crore over five years to develop India as a global biopharma manufacturing centre.

- Rejuvenating Legacy Industrial Sectors: A Scheme to revive 200 legacy industrial clusters announced, to improve their cost competitiveness and efficiency through infrastructure and technology upgradation.

- Champion MSMEs: A dedicated Rs 10,000 crore "SME Growth Fund" will be launched to incentivize high-potential firms and create "Champion MSMEs" that can compete globally.

- The Self-Reliant India Fund will get an additional Rs 2,000 crore to continue supporting micro enterprises and ensure steady access to risk capital, with ‘Corporate Mitras’ envisioned as key enablers to mentor, guide, and integrate these enterprises into larger value chains.

- Infrastructure as "Growth Connectors":

- High-Speed Rail: 7 High-Speed Rail corridors between cities - Mumbai-Pune, Pune-Hyderabad, Hyderabad-Bengaluru, Hyderabad-Chennai, Chennai-Bengaluru, Delhi-Varanasi, Varanasi- Siliguri will be developed as "Growth Connectors" to spur economic activity.

- Sustainable Movement of Cargo: To promote environmentally sustainable cargo movement, new Dedicated Freight Corridors will connect Dankuni to Surat, alongside the operationalisation of 20 National Waterways over the next five years.

- A Coastal Cargo Promotion Scheme will incentivise a shift from road and rail to waterways and coastal shipping to raise their share from 6% to 12% by 2047.

- The Seaplane VGF Scheme will support indigenised seaplane manufacturing and operations to improve last-mile connectivity and promote tourism.

- Infrastructure Risk Guarantee Fund: The Budget proposed an Infrastructure Risk Guarantee Fund to offer prudently calibrated partial credit guarantees to lenders during the infrastructure development and construction phase.

- City Economic Regions (CER): The Government proposed "City Economic Regions" (CERs), a new initiative to map cities based on specific growth drivers.

- An allocation of Rs 5,000 crore per CER over 5 years is proposed to be implemented via a "challenge mode."

- Carbon Capture (CCUS): A scheme for Carbon Capture, Utilization, and Storage launched to decarbonize hard-to-abate sectors (Steel, Cement).

Second Kartavya: Fulfill Aspirations & Build Capacity

- AVGC Content Creator Labs: Recognizing the potential of the "Orange Economy", the Government will support the Indian Institute of Creative Technologies, Mumbai, in setting up "Animation, Visual Effects, Gaming and Comics (AVGC) Content Creator Labs in 15,000 secondary schools and 500 colleges.

- National Institute of Hospitality: A proposal was made to set up this institute by upgrading the existing National Council for Hotel Management and Catering Technology, bridging the gap between academia and the tourism industry.

- Khelo India Mission: Building on the Khelo India programme, the Budget launches a Khelo India Mission to transform the sports sector through integrated talent development, coach capacity building, sports science integration, competitive leagues, and expanded sports infrastructure.

- Medical Value Tourism: The Government proposed establishing five Regional Medical Hubs in partnership with the private sector to boost India’s status as a wellness and medical tourism destination, with integrated facilities including AYUSH Centres, diagnostics, post-care, and rehabilitation services.

- Women in STEM: To support girl students in STEM, one girls’ hostel will be established in every district through Viability Gap Funding (VGF) or capital support.

Third Kartavya: Sabka Saath, Sabka Vikas

- Bharat-VISTAAR: To revolutionize agriculture, the "Bharat-VISTAAR" (Virtually Integrated System to Access Agricultural Resources) tool will be launched.

- SHE Marts: Building on the success of the "Lakhpati Didis", community-owned retail outlets named "SHE Marts" (Self-Help Entrepreneur Marts) will be set up within cluster federations.

- Mental Health Infrastructure: Reaffirming its commitment, the Government announced the setting up of "NIMHANS-2" and proposed upgrading institutes in Ranchi and Tezpur to "Regional Apex Institutions".

- Purvodaya & North-East:

- Buddhist Circuits: A specific scheme will be launched to develop "Buddhist Circuits" in the North East Region (e.g., Arunachal Pradesh, Sikkim, Assam, Manipur, Mizoram and Tripura).

- East Coast Industrial Corridor: Proposed the development of an East Coast Industrial Corridor with a well-connected node at Durgapur (West Bengal), creation of five tourism destinations in five Purvodaya States.

- Divyangjan Support: Targeted efforts will be made to empower the differently-abled through schemes like "Divyang Sahara Yojana" (implied in welfare focus).

What are the Key Highlights of the Tax Reforms under Union Budget 2026-27?

- New Income Tax Act, 2025: The government replaces the existing Income Tax Act, 1961 with a new, simplified Income Tax Act, 2025, effective from 1st April 2026.

- Tax Rates: No changes to the tax slabs for FY 2026-27; stability maintained.

- TCS Rationalization: Tax Collected at Source (TCS) on overseas tour packages and remittances for education/medical purposes under LRS is reduced to a uniform 2% (without any threshold).

- Rationalization of TDS: To remove ambiguity, Tax Deduction at Source (TDS) on the supply of manpower services is fixed at 1% (for Individuals/HUF) or 2% (for others).

- Non-production of books of accounts and failure to pay TDS (where payment is made in kind) will be decriminalized.

- Customs Duty Rationalization: The tariff rate on goods imported for personal use is reduced from 20% to 10%.

- Customs duty is fully exempted on 17 cancer drugs and medicines/foods for 7 rare diseases.

- Securities Transaction Tax (STT): Marginally increased (from 0.1% to 0.15% in certain segments) to curb excessive speculation in equity markets.

- Minimum Alternate Tax (MAT): The Union budget also proposes to provide exemption from Minimum Alternate Tax (MAT) to all non-residents who pay tax on presumptive basis.

- Tax Administration: The Budget proposes a Joint Committee of Ministry of Corporate Affairs and Central Board of Direct Taxes for incorporating the requirements of Income Computation and Disclosure Standards (ICDS) in the Indian Accounting Standards (IndAS), eliminating separate ICDS-based accounting from tax year 2027–28, and rationalising the definition of accountant under the Safe Harbour Rules to simplify compliance.

- Immunity from Prosecution: Non-disclosure of foreign assets worth less than Rs 20 lakh will be granted immunity from prosecution (retrospective effect from 1st October 2024).

- Buyback Tax Shift: Share buybacks will now be taxed as Capital Gains in the hands of the shareholder (shifting the burden from the company to the recipient).

- Strategic Incentives for Investment & Industry:

- Data Centers Tax Holiday: Foreign companies providing global cloud services via Indian data centers will receive a tax holiday until 2047.

- IFSC (GIFT City): Tax holiday extended from 10 to 20 years for Offshore Banking Units.

- Critical Minerals: Customs duty exemptions granted on capital goods required for the processing of critical minerals (Lithium, Cobalt, etc.) and manufacturing of Lithium-ion cells.

- IT Sector Safe Harbour: The threshold for availing "Safe Harbour" rules for IT services is enhanced to Rs 2,000 crore, with a unified category for software development and KPO services.

- Customs Modernization & Export Promotion

- Sectoral Relief: Duty-free import limits for inputs in Marine, Leather, and Textile sectors have been increased to boost export competitiveness.

- Aviation & Defence: Duty exemptions provided for parts/components used in the manufacture and MRO (Maintenance, Repair, Overhaul) of aircraft.

- Ease of Doing Business: The Budget streamlines trade through a single digital window for cargo clearance, instant customs clearance for non-compliant goods, rollout of the Customs Integrated System (CIS), and expanded AI-based container scanning.

- It makes Exclusive Economic Zone (EEZ) or on the High Seas fish catch duty-free, revises duty-free baggage allowances, and allows dispute settlement for honest taxpayers with a reduced penalty.

Macroeconomic Fundamentals Highlighted in Union Budget 2026-27

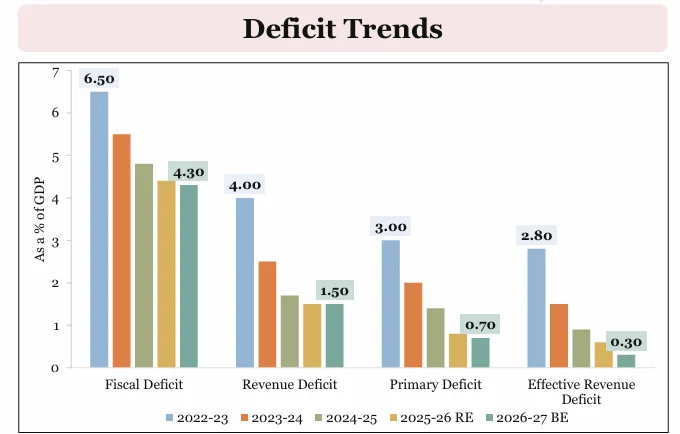

- Fiscal Deficit: The target for Budget Estimate (BE) 2026-27 is set at 4.3% of GDP, adhering to the glide path of reducing it below 4.5%. It has improved from 4.4% in the Revised Estimates (RE) of 2025-26.

- Debt-to-GDP Ratio: Estimated to decline to 55.6% in BE 2026-27 (from 56.1% in RE 2025-26).

- The government aims to bring this ratio down to 50% by 2030-31 to free up resources for development.

- Capital Expenditure (Capex): The government continues to use public investment as the primary driver of economic growth.

- Capex Allocation has been increased to Rs 12.2 Lakh Crore for FY 2026-27 (approx. 3.1% of GDP) (up from Rs 11.2 Lakh Crore).

- When grants-in-aid to states for capital assets are included, the Effective Capital Expenditure stands at Rs 17.1 Lakh Crore (approx. 4.4% of GDP).

- GDP Growth: The Budget assumes a Nominal GDP growth of 10.5% for FY 2026-27, with Real GDP growth projected at around 7%.

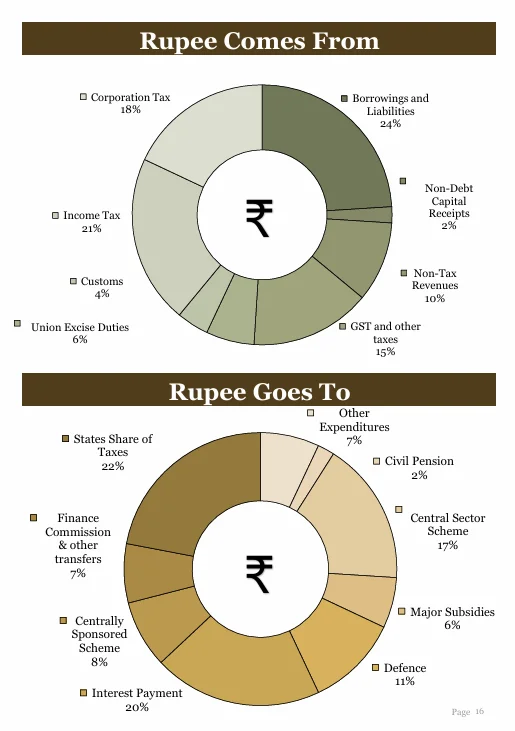

- Revised Estimates 2025–26: Non-debt receipts are estimated at Rs 34 lakh crore, while total expenditure is pegged at Rs 49.6 lakh crore, with capital expenditure of about Rs 11 lakh crore.

- Budget Estimates 2026–27: Non-debt receipts are estimated at Rs 36.5 lakh crore, with net tax receipts of Rs 28.7 lakh crore, while total expenditure is projected at Rs 53.5 lakh crore.

- To finance the fiscal deficit, net market borrowings are estimated at Rs 11.7 lakh crore, with gross borrowings of Rs 17.2 lakh crore, and the remainder to be met through small savings and other sources.

What are the Concerns Regarding the Union Budget 2026–27?

- Global Headwinds: The Budget assumes 10.0 % nominal GDP growth (First Advance Estimates of FY 2025-26), which may be tested by global economic slowdown, geopolitical conflicts, and trade disruptions.

- Revenue Buoyancy: Large shortfalls in income tax and GST collections sharply reduced fiscal space, triggering across-the-board expenditure cuts, including in capital spending and key social sectors.

- The Budget bets heavily on Supply-Side Economics (building roads, factories, and railways) to drive growth. However, Private Consumption (which forms ~60% of GDP) has been limited, especially in rural areas.

- Implementation Lag: High-technology schemes such as Bharat-VISTAAR and Biopharma SHAKTI require advanced institutional capacity and often face bureaucratic and execution bottlenecks, while other infrastructure projects also continue to struggle with land acquisition challenges.

- Job Creation Gap: A capex-heavy strategy focused on semiconductors and biopharma risks jobless or K-shaped growth, given limited labour absorption amid a widening education–employment skill mismatch.

- Green Transition and Resource Constraints: The shift to green technologies increases demand for water, energy, and critical minerals, raising import dependence and risks of greenflation that may elevate costs for MSMEs and manufacturing.

- Uncertain Capital Flows: Persistent Foreign Portfolio Investors (FPIs) outflows and an unclear Foreign Direct Investment (FDI) outlook raise concerns over external financing stability and investor confidence.

- External Aid Prioritisation Challenge: The Union Budget 2026–27 allocates grants-in-aid to foreign countries, with Bhutan as the largest beneficiary, while no funds for the strategically important Chabahar Port project in Iran raise concerns over India’s regional connectivity and strategic outreach.

What Measures can Strengthen India’s Economy Beyond Budget 2026–27?

- Reviving the Twin Engines of Demand: India’s growth needs both investment and consumption to fire together. Faster rollout of SHE Marts and Bharat-VISTAAR can raise rural incomes and boost demand due to higher marginal propensity to consume.

- Securing Strategic Autonomy in Critical Resources: As critical minerals become the “new oil” of the green economy, India must combine domestic initiatives like Rare Earth Corridors with overseas mineral security partnerships.

- Simultaneously, boosting R&D spending beyond the current low share of GDP is essential to support semiconductors and biopharma ecosystems.

- Skilling for New Sectors: The AVGC and Semiconductor push must be matched with aggressive skill development (Skill India 2.0) to prevent a talent crunch.

- Quality of Expenditure: Move from "Outlays" to "Outcomes." Every Rupee spent on schemes like Mahatma Gandhi Gram Swaraj must be audited for tangible asset creation and income generation, not just fund utilization.

- Correcting "Inverted Duty Structures": In sectors like textiles and electronics, inverted duty structures (where raw materials are taxed higher than finished imports) hurt domestic manufacturing.

- A sector-wise duty correction is needed to ensure “Made in India” is cheaper than imported goods at the tax level.

Conclusion

The Union Budget 2026-27 strategically balances fiscal prudence with an aggressive push for high-tech industrialization and inclusive welfare, laying a robust foundation for a "Viksit Bharat." However, its ultimate success will depend on the effective implementation of schemes to bridge the "Jobless Growth" gap and the revival of private consumption to ensure economic momentum reaches the "Last Mile."

|

Drishti Mains Question: The Union Budget 2026-27 attempts to balance the twin objectives of global competitiveness in frontier sectors and inclusive growth for the 'Last Mile'." Discuss this statement with reference to the 'Three Kartavyas' outlined in the Budget. |

Frequently Asked Questions (FAQs)

1. What are the Three Kartavyas outlined in Union Budget 2026–27?

They focus on sustaining economic growth, building people’s capacities, and ensuring Sabka Saath, Sabka Vikas through last-mile inclusion.

2. What is Biopharma SHAKTI and why is it important?

Biopharma SHAKTI is a ₹10,000 crore mission to make India a global hub for biologics and biosimilars, supported by NIPERs and regulatory strengthening.

3. What are City Economic Regions (CERs)?

CERs are city-cluster based growth regions with ₹5,000 crore funding per region to leverage agglomeration economies through challenge-mode implementation.

4. Why is the Budget criticised for jobless growth?

The focus on capital-intensive sectors like semiconductors and biopharma may limit mass employment amid a widening education–employment skill gap.

5. What are the key fiscal targets in Budget 2026–27?

The fiscal deficit is targeted at 4.3% of GDP, debt-to-GDP at 55.6%, and capex raised to ₹12.2 lakh crore to drive growth.

UPSC Civil Services Examination, Previous Year Question (PYQ)

Prelims:

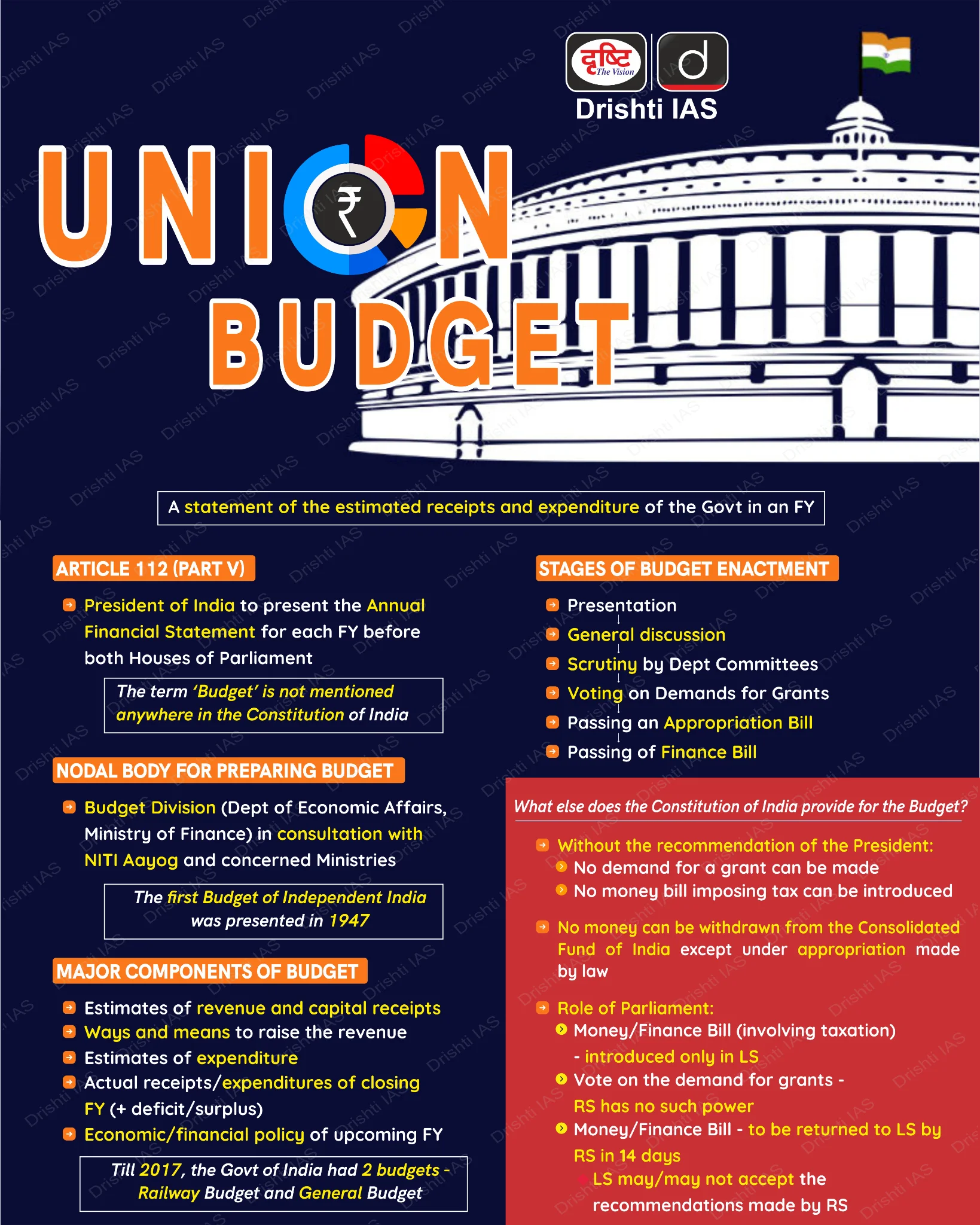

Q1. What is the difference between “vote-on-account” and “Interim Budget”? (2011)

- The provision of a “vote-on-account” is used by a regular Government while an “interim budget” is a provision used by a caretaker Government.

- A “vote-on-account” only deals with the expenditure in Government’s budget, while an “interim budget” includes both expenditures and receipts.

Which of the statements given above is/are correct?

(a) 1 only

(b) 2 only

(c) Both 1 and 2

(d) Neither 1 nor 2

Ans: (b)

Q2. Along with the Budget, the Finance Minister also places other documents before the Parliament which include ‘The Macro Economic Framework Statement’. The aforesaid document is presented because this is mandated by (2020)

(a) Long standing parliamentary convention

(b) Article 112 and Article 110(1) of the Constitution of India

(c) Article 113 of the Constitution of India

(d) Provisions of the Fiscal Responsibility and Budget Management Act, 2003

Ans: (d)

Mains:

Q1. Distinguish between Capital Budget and Revenue Budget. Explain the components of both these Budgets. (2021)

Q2. The public expenditure management is a challenge to the Government of India in the context of budget-making during the post-liberalization period. (2019)