India’s Aviation Sector | 12 Feb 2026

For Prelims: Directorate General of Civil Aviation, UDAN Scheme, Aviation Turbine Fuel

For Mains: Structural challenges in India aviation sector, Regulatory capacity and safety oversight, Infrastructure and skill bottlenecks

Why in News?

India's civil aviation sector has witnessed repeated operational disruptions and safety concerns in 2025, alongside declining profitability of major airlines. With new regional players entering the market, questions have arisen about systemic vulnerabilities in the sector.

Summary

- India's aviation sector is large but structurally overstretched, with demand growth outpacing institutional capacity.

- A duopoly controlling nearly 90 percent of the market increases systemic risk and limits resilience.

- Pilot shortages, regulatory gaps and fuel volatility are core structural constraints.

- Without coordinated reform, rapid expansion may convert growth into recurring operational crises.

What is the Status of India’s Aviation Sector?

- Global Ranking: India is the 3rd-largest domestic aviation market after the US and China. It accounts for about 4.2% of global air traffic. The Indian fleet accounts for around 2.4% of the total global fleet. Fleet size has grown rapidly due to airline expansion and new aircraft orders.

- Passenger Traffic Growth: By 2030, domestic passenger demand is expected to reach around 715 million. By 2040, the passenger traffic is expected to grow six-fold to around 1.1 billion.

- Airport Infrastructure Expansion: The number of operational airports increased from 74 in 2014 to 163 in 2025. By 2047, India aims to expand to 350–400 airports, with a strong emphasis on greenfield projects and PPP-based development.

- Economic Contribution: As of 2025, aviation supports over 7.7 million jobs and contributes 1.5% of India’s GDP.

- Indian Civil Aviation Regulation:

- Air Corporations Act, 1953: Nationalised nine airline companies. Government-owned airlines dominated the sector till the mid-1990s.

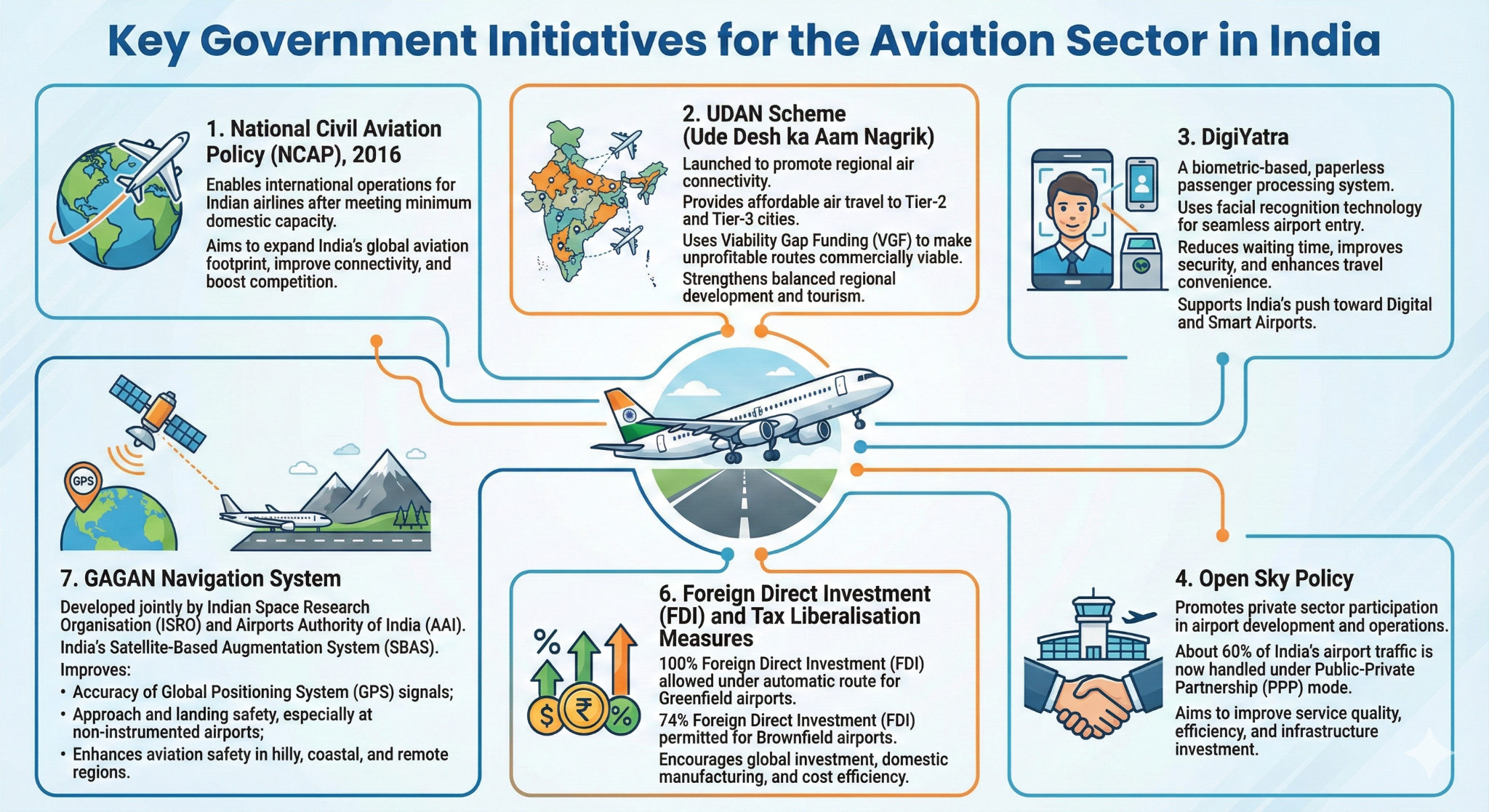

- Open Sky Policy (1990–94): Allowed private air taxi operators. Ended the monopoly of Indian Airlines (IA) and Air India (AI).

- The Bharatiya Vayuyan Adhiniyam, 2024: Replaces the colonial-era Aircraft Act, 1934 and aligns India’s aviation laws with ICAO standards and the Chicago Convention.

- It promotes Make in India and Atmanirbhar Bharat in aviation manufacturing, introduces simplified licensing and regulatory processes, provides a structured appeals mechanism, and modernises India’s overall aviation governance framework.

What are the Key Challenges in India’s Aviation Sector?

- Training and Skill Bottlenecks: Simulator shortages, limited trainer availability, high training costs, and type-rating constraints have made pilot supply relatively inelastic. Around 236 temporary foreign pilot approvals were issued in 2025, indicating reliance on expensive stopgap solutions.

- High Market Concentration and Systemic Risk: IndiGo (63–65%) and the Air India group (27–28%) together control nearly 90% of domestic passenger traffic. IndiGo operates as the sole carrier on about 60% of routes, meaning disruptions result in outright loss of connectivity rather than passenger redistribution.

- Low Shock Absorption Capacity: Globally, airlines maintain 20–25% spare crew capacity to absorb operational shocks, whereas Indian carriers operate at near-total utilisation, allowing minor disruptions to cascade into network-wide failures.

- Weak Regulatory Capacity: Nearly half of the Directorate General of Civil Aviation’s sanctioned technical posts remain vacant. Disruptions have often been managed through schedule exemptions rather than strict enforcement, reflecting ad hoc crisis management.

- High Operating Costs and Fuel Volatility: Airlines face financial pressure due to volatile Aviation Turbine Fuel (ATF) prices linked to global crude oil markets and the U.S. dollar, increasing cost instability.

- Recurring Airline Failures: The sector has witnessed multiple airline collapses including Kingfisher Airlines (2012), Jet Airways (2019), Go First (2023), and others, highlighting persistent financial and structural vulnerabilities.

- Aviation Safety Risks: Rising traffic, repeated operational disruptions, and 19 safety violation notices issued by the Directorate General of Civil Aviation (DGCA) in 2025 indicate growing concerns over safety compliance and systemic resilience.

New Regional Airlines and Connectivity Initiatives

- Entry of New Regional Carriers: In December 2025, the Ministry of Civil Aviation granted No Objection Certificates to Shankh Air, Al Hind Air and FlyExpress to expand regional air connectivity and reduce market concentration.

- Focus on Tier 2 and Tier 3 Cities: These airlines aim to operate from emerging hubs such as Noida International Airport, Kochi and Telangana, targeting underserved regional routes and improving last-mile air access.

- Strengthening Regional Connectivity through UDAN: Under the UDAN scheme, 625 routes and 85 airports have been operationalised by 2025, including over 100 routes in the Northeast, promoting inclusive air travel.

What Measures can Strengthen India’s Aviation Sector?

- Shift from Crisis Management to Structural Reform: Replace ad hoc schedule exemptions with long-term institutional strengthening to ensure system resilience as passenger demand rises sharply toward 715 million by 2030.

- Strengthen Regulatory Oversight Capacity: Fill vacant technical posts in the Directorate General of Civil Aviation and adopt rule-based, risk-based supervision mechanisms to improve safety compliance and enforcement credibility.

- Expand Pilot Training Ecosystem: Increase simulator capacity, expand domestic training institutions, streamline licensing processes, and address type-rating bottlenecks to meet projected pilot demand and reduce dependence on temporary foreign approvals.

- Institutionalise Reserve Capacity Norms: Establish minimum spare crew thresholds closer to global standards (20–25%) to prevent cascading disruptions during peak travel seasons and operational shocks.

- Support Viable Regional Carriers: Move beyond merely granting NOCs by ensuring effective implementation of UDAN subsidies, preferential slot allocation at congested airports, and coordinated development of Tier-2 and Tier-3 airport infrastructure to reduce overdependence on dominant carriers.

- Rationalise Fuel Policy: Consider tax rationalisation on Aviation Turbine Fuel (ATF) and explore fuel hedging mechanisms to reduce exposure to global price volatility and dollar-linked fluctuations.

Conclusion

India's aviation sector has achieved impressive scale but remains structurally fragile. Pilot shortages, regulatory gaps, high market concentration, and cost volatility threaten long-term sustainability. Structural reform, rather than reactive crisis management, is essential to ensure safe, competitive, and resilient aviation growth.

|

Drishti Mains Question Examine the challenges facing India’s aviation sector and suggest measures to ensure sustainable and resilient growth. |

Frequently Asked Questions (FAQs)

1. What is the role of DGCA in India?

DGCA is India’s apex civil aviation regulator under the Ministry of Civil Aviation, responsible for air safety, licensing, airworthiness, flight regulation, and ICAO coordination.

2. What is India’s current global position in civil aviation?

India is the 3rd-largest domestic aviation market after the USA and China and supports over 7.7 million jobs.

3. Why is India’s aviation sector structurally vulnerable?

Rapid growth, pilot shortages, weak regulatory capacity, and high market concentration make it prone to systemic disruptions.

4. How does UDAN strengthen the aviation sector?

UDAN boosts regional connectivity by expanding access to underserved routes and airports.

UPSC Civil Services Examination, Previous Year Questions (PYQs)

Mains

Q. Examine the development of Airports in India through joint ventures under Public–Private Partnership (PPP) model. What are the challenges faced by the authorities in this regard? (2017)