16th Finance Commission Report | 04 Feb 2026

For Prelims: Finance Commission, Tax Devolution, Cess, Surcharge, Total Fertility Rate, Fiscal deficit

For Mains: Recommendations of the 16th Finance Commission, Tax Devolution its significance and its Constitutional Mandates, Evolution and role of Finance Commissions in Indian federalism

Why in News?

The 16th Finance Commission (16th FC), chaired by Arvind Panagariya, has submitted its report for the award period 2026-31. The recommendations, tabled in Parliament alongside the Union Budget 2026-27, signal a significant shift from "entitlement-based" transfers to "compliance-driven" fiscal federalism.

Summary

- The 16th FC retains states’ tax share at 41% and shifts fiscal transfers toward performance- and compliance-based criteria, including a new weight for contribution to GDP.

- It emphasises fiscal discipline by capping state deficits at 3% of GSDP, ending off-budget borrowings, rationalising subsidies, and warning against unchecked unconditional cash transfers.

- While strengthening efficiency and transparency, the recommendations raise concerns over shrinking untied funds, equity in horizontal devolution, and state fiscal autonomy, especially for southern and poorer states.

What are the Key Recommendations of the 16th Finance Commission (2026–31)?

Tax Devolution:

- Vertical Devolution: This is the percentage of the Central Government's Divisible Pool of taxes that is given to the States.

- Under 16th FC, states’ share in the divisible pool of central taxes was retained at 41%, unchanged from the 15th Finance Commission.

- The divisible pool excludes cesses, surcharges, and cost of collection from gross central tax revenue.

- Horizontal Devolution: This is the formula used to decide exactly how many rupees each state gets from that 41% pot.

- The 16th FC has introduced a major shift toward rewarding economic performance.

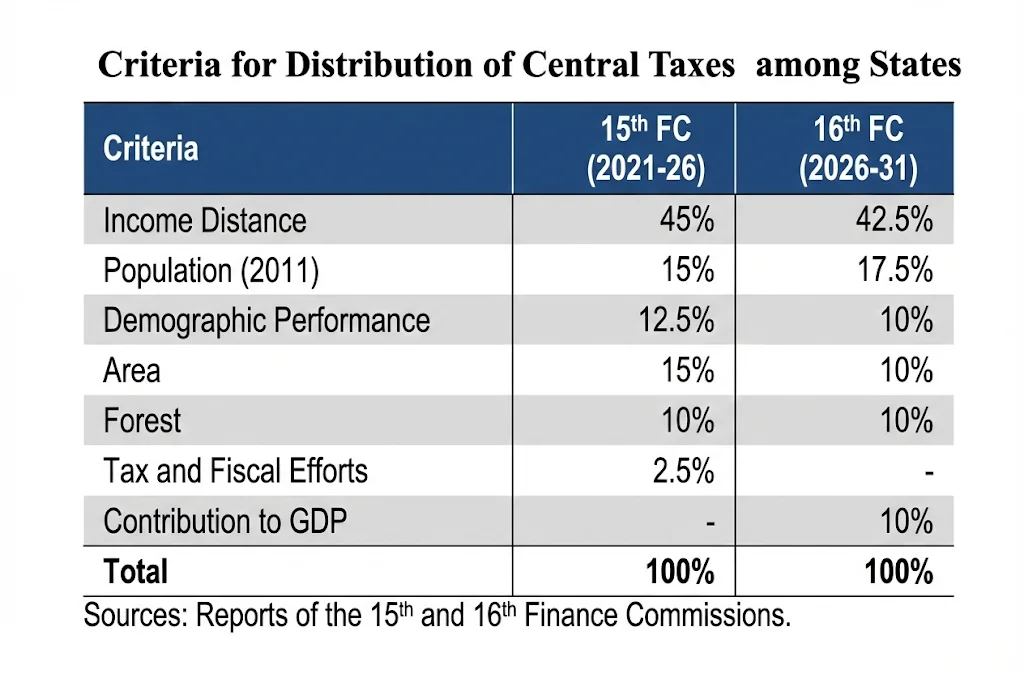

- Distribution among states is based on a revised devolution formula with weights for income distance (42.5%), population as per the 2011 Census (17.5%), demographic performance (10%), area (10%), forest & ecology (10%), and a new 10% weight for contribution to GDP, while excluding the tax and fiscal effort parameter used by the 15th FC.

16th FC Criteria for Devolution

- Per Capita GSDP Distance (Income Distance): Defined as the gap between a state’s per capita GSDP and the average per capita GSDP of the top three large states with the highest income levels.

- States with lower per capita GSDP receive a higher share, ensuring inter-state equity.

- Population (2011 Census): Devolution is based on each state’s share in India’s population as per the 2011 Census, reflecting expenditure needs arising from population size.

- Demographic Performance: Measures population growth between 1971 and 2011, instead of changes in Total Fertility Rate (TFR).

- States with lower population growth during this period receive a higher share, rewarding effective population control.

- Forest: Weightage is assigned based on a state’s share in total forest area and its contribution to the increase in forest cover between 2015 and 2023. Unlike the 15th FC, open forests are also included, not just dense and moderately dense forests.

- Contribution to GDP: A new criterion recognising a state’s economic contribution to national GDP, replacing the earlier tax and fiscal effort parameter.

- It rewards states contributing more to national economic output.

Grants-in-Aid

- The 16th FC has recommended grants worth Rs 9.47 lakh crore over the five-year period. These comprise grants for urban and rural local bodies, and disaster management.

- Revenue deficit grants, sector-specific grants, and state-specific grants recommended by the 15th Finance Commission have been discontinued.

- Grants for Local Bodies: Grants to local bodies amount to Rs 8 lakh crore, with Rs 4.4 lakh crore allocated to rural local bodies and Rs 3.6 lakh crore to urban local bodies.

- All local body grants are subject to three entry conditions: constitution of local bodies as per the Constitution, public disclosure of provisional and audited accounts, and timely constitution of State Finance Commissions.

- Local body grants are split into basic grants (80%) and performance-based grants (20%). This structure aims to ensure predictable transfers while incentivising fiscal and administrative performance.

- 50% of the basic grant will be untied and the rest 50% will be tied to sanitation and solid waste management, and/or water management.

- Performance grants will be further divided between local body-level outcomes and state-level reforms.

- Urbanisation premium grants of Rs 10,000 crore are proposed as one-time transfers to states. These are meant to support the merger of peri-urban villages into ULBs and the formulation of a Rural-to-Urban Transition Policy.

- Special infrastructure grants of Rs 56,100 crore have been recommended for developing comprehensive wastewater management systems in cities with populations between ten and forty lakh, as per the 2011 Census.

- Disaster Management Grants: Rs 2,04,401 crore for State Disaster Relief and Management Funds (SDRF and SDMF).

- Cost sharing is 90:10 for north-eastern and Himalayan states and 75:25 for other states. Centre’s share is Rs 1,55,916 crore.

Other Recommendations

- Fiscal roadmap: Recommended the centre to reduce fiscal deficit to 3.5% of GDP by 2030–31. It recommended the annual fiscal deficit limit for states to be 3% of GSDP.

- It recommended ending Off-budget borrowings and including all such liabilities in fiscal deficit and debt. Combined Centre–state debt is projected to decline from 77.3% of GDP in 2026–27 to 73.1% in 2030–31.

- Power Sector Reforms: States encouraged to privatise DISCOMs. Legacy debt to be parked in a special purpose vehicle, with repayment allowed through the Special Assistance Scheme for Capital Investment, usable only after privatisation.

- Subsidy Expenditure: It recommended states to rationalise subsidies, especially unconditional cash transfers, introduce clear exclusion criteria, stop off-budget financing, and adopt uniform accounting and disclosure of subsidies and transfers.

- Across 21 states, these schemes now account for 20.2% of total subsidy spending in 2025–26, up from just 3% in 2018–19.

- By 2025–26, large-group cash transfer schemes alone account for 47.4%, overtaking traditional social security spending. The Commission links this shift partly to the success of the JAM trinity, which has made mass cash transfers administratively easy and politically attractive.

- Public Sector Enterprise Reforms: Recommended closure of 308 inactive SPSEs recommended.

- Loss-making PSEs for 3 out of 4 consecutive years to be placed before the Cabinet for a decision on closure, privatisation, or continuation based on strategic importance.

- Data on Net Tax Proceeds :The Commission recommended that the Union government annually disclose Comptroller and Auditor General (CAG)-certified data on net tax proceeds under Article 279, to enhance transparency in the size of the divisible pool and ensure greater clarity on actual tax devolution to states.

What are the Concerns Regarding the 16th Finance Commission?

- Stagnation in Vertical Devolution: 16th FC has retained states’ share in central taxes at 41%, despite states demanding an increase to 50%.

- This is seen as inadequate given expanding state responsibilities in health, education, and welfare, especially after the Goods and Services Tax (GST) reduced their revenue autonomy.

- The continued heavy use of cesses and surcharges, which lie outside the divisible pool, further shrinks states’ untied fiscal space and worsens vertical fiscal imbalance.

- Changes in Horizontal Devolution Formula: Reduced weight for income distance weakens equity, while higher weight for population (2011) and a new 10% weight for contribution to GDP favours populous and industrialised states.

- Southern states contend that fiscal devolution now disadvantages them despite successful population control, while poorer states fear tighter transfers will hinder development.

- Tamil Nadu saw only a minimal rise in share from 4.079% to 4.097%, reflecting reduced weightage for area, demographic performance, and per-capita GSDP.

- Phasing Out of Demographic Performance Incentives: 16th FC flags the risk of “aging before becoming rich” and gradually reduces rewards for population control.

- This has raised concerns among southern states that early investments in fertility reduction are no longer adequately recognised, undermining the principle of cooperative federalism.

- Discontinuation of Revenue Deficit Grants: The complete scrapping of Revenue Deficit grants is controversial.

- Hill and special category states argue that their structural and geographical constraints make revenue deficits unavoidable, and removal of such support ignores asymmetric federal realities.

- Off-budget Borrowing Restrictions: The insistence on a 3% GSDP fiscal deficit cap for states and a complete end to off-budget borrowings is seen as fiscally prudent but potentially contractionary.

- States fear an investment squeeze in infrastructure and welfare, especially when combined with pressure to rationalise subsidies.

- Over-centralisation: An increasing share of tied grants limits states’ flexibility to address local priorities.

- This fuels concerns that states are being reduced to implementing agencies for centrally defined priorities, undermining fiscal autonomy.

What Measures can Strengthen fiscal federalism?

- Elasticity-Linked Transfers: A portion of the devolution could be linked to the "Revenue Buoyancy" of a state. This would reward states that are improving their tax systems even if their absolute GDP is currently low.

- Phased Implementation: The 16th FC has already signaled a "gradual" shift, but states recommend a "Floor Guarantee" - ensuring no state’s absolute share in nominal terms drops below their 15th FC levels during the transition.

- SFC Empowerment: The Union could provide a "Matching Grant" to states that successfully implement their own State Finance Commission (SFC) recommendations, turning a penalty-based system into a reward-based one.

- Capping Surcharges: Legislation could be introduced to cap cesses/surcharges at a specific percentage (e.g., 10%) of the Gross Tax Revenue (GTR), ensuring they remain "temporary" as originally intended by the Constitution.

- Inter-State Council Reactivation: Frequent meetings of the Inter-State Council (Article 263) specifically on fiscal matters would allow for "Real -time Federalism," where concerns about grant delays (the 10-day rule) can be resolved without litigation.

Conclusion

The 16th FC transitions India toward a compliance-driven fiscal model, prioritizing economic contribution and forest ecology. It enforces strict fiscal discipline at the expense of state-level autonomy. Ultimately, its success depends on balancing rewards for performing states with the essential support required for ecologically and structurally vulnerable regions.

|

Drishti Mains Question: The 16th Finance Commission marks a shift from entitlement-based to compliance-driven fiscal federalism. Critically examine the implications of this shift for Centre–state relations. |

Frequently Asked Questions (FAQs)

1. What is vertical devolution under the 16th Finance Commission?

It refers to sharing 41% of the divisible pool of central taxes with states for 2026–31, unchanged from the 15th Finance Commission.

2. What major change has been made in horizontal devolution?

A new 10% weight for contribution to GDP has been introduced, while the tax and fiscal effort criterion has been removed.

3. Why has the 16th FC warned against unconditional cash transfers?

Such schemes now form 20.2% of total subsidy spending, risk fiscal instability, and crowd out capital and social sector expenditure.

4. What are the key conditions attached to local body grants?

Constitution of local bodies, public disclosure of audited accounts, and timely State Finance Commission formation.

5. How does the 16th FC address fiscal discipline?

It caps state fiscal deficits at 3% of GSDP, ends off-budget borrowings, and targets a decline in combined debt to 73.1% of GDP by 2030–31.

UPSC Civil Services Examination, Previous Year Questions (PYQs)

Prelims

Q. Consider the following:

- Demographic performance

- Forest and ecology

- Governance reforms

- Stable government

- Tax and fiscal efforts

For the horizontal tax devolution, the Fifteenth Finance Commission used how many of the above as criteria other than population area and income distance (2023)

A. Only two

B. Only three

C. Only four

D. All five

Ans: B

Q. With reference to the Fourteenth Finance Commission, which of the following statements is/ are correct? (2015)

- It has increased the share of States in the central divisible pool from 32 percent to 42 percent.

- It has made recommendations concerning sector-specific grants.

Select the correct answer using the code given below.

(a) 1 only

(b) 2 only

(c) Both 1 and 2

(d) Neither 1 nor 2

Ans: (a)

Mains

Q. How have the recommendations of the 14thFinance Commission of India enabled the states to improve their fiscal position?(2021).

Q. How is the Finance Commission of India constituted? What do you about the terms of reference of the recently constituted Finance Commission? Discuss.(2018)

Q. Discuss the recommendations of the 13th Finance Commission which have been a departure from the previous commissions for strengthening the local government finances.(2013)