Corporates Houses & Banking | 30 Nov 2021

Why in News

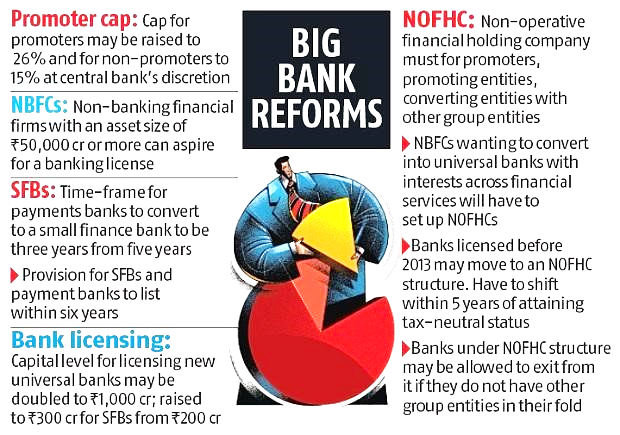

Recently, the Reserve Bank of India (RBI) has put on hold the recommendations from its Internal Working Committee (IWG), that said large corporate and industrial houses may be allowed to promote banks after amendments to the Banking Regulations Act, 1949.

- The RBI has accepted 21 out of 33 recommendations of the IWG on ownership of private banks, but kept silent on giving banking licence to big business groups.

Key Points

- About:

- Corporate Houses (CH) were active in the banking sector till five decades ago when the banks promoted by them were nationalised in the late sixties amid allegations of connected lending and misuse of depositors’ money.

- The Banking sector was opened up again for the CHs Post Liberalisation (1991) with the first round of licensing of private banks that was done in 1993.

- Since then, there were two more rounds of licensing of banks in the private sector – in 2003-04 and 2013-14 – culminating with the on-tap licensing regime of universal banks in 2016.

- However, even some prominent business houses were not considered in 2013-14.

- Pros of Allowing Corporations To Own Bank:

- Plugging Capital Gap:

- Currently, the government keeps picking money from the taxpayers pocket and funding the public sector banks.

- Hence, by allowing the big corporates into the banking sector the capital requirement can be fulfilled.

- Financial Inclusion:

- Even today a significant population do not have access to banking in the country, the corporates’ entry would mean the opening of more branches and subsequently bringing more people into the banking net.

- Improving Competition:

- Privatization of banks has been a long-proposed reform in the Indian banking industry. Allowing corporations into the banking sector will further pressurize Public sector banks to become competitive.

- Plugging Capital Gap:

- Concerns of Allowing Corporates To Own Bank:

- Connected Lending & Moral Hazard:

- There are apprehensions that it would not be easy for supervisors to prevent or detect self-dealing or connected lending as banks could hide connected party or related party lending behind complex company structures and subsidiaries or through lending to suppliers of promoters and their group companies.

- Connected lending involves the controlling owner of a bank giving loans to himself or his related parties and group companies at favourable terms and conditions.

- Big business groups already account for a major chunk of Non-Performing Assets (NPAs) in the banking system even without becoming promoters of a bank.

- In ethical terms, this will erode the bank’s role as an effective financial and create a moral hazard or conflict of interest situation.

- There are apprehensions that it would not be easy for supervisors to prevent or detect self-dealing or connected lending as banks could hide connected party or related party lending behind complex company structures and subsidiaries or through lending to suppliers of promoters and their group companies.

- Circular Lending & Difficulty In Regulation:

- Under circular lending, corporate bank X funding projects of an industry group, which owns corporate bank Y, and corporate bank Y funding projects of an industry group owning bank Z, and finally, corporate bank Z funding projects of industry group owning bank X.

- With available legal structures and the proliferation of shell companies, makes it hard to track such lending on a real-time basis.

- Inequality & Concentration of Wealth:

- Corporations owning banks will add more muscle to big industry groups, which already dominate many important sectors of the economy, including telecom, organised retail, aviation, software and e-commerce.

- This will further accelerate the concentration of wealth and increase inequalities.

- Contradicting the Previous Ruling:

- The banking sector in India has been in trouble for the last few years, keeping that in mind the RBI in 2016 had created new guidelines on the limit of lending to a single company.

- The rationale behind this ruling was that if a bank lends too much to one company only then it risks losing that money if the company sinks.

- Therefore, the recommendation of allowing the entry of industry groups in the banking sector is in contradiction with the above-said ruling in 2016.

- Connected Lending & Moral Hazard:

Way Forward

- Before granting much economic power in the hands of corporations, it is imperative to carry out the long-pending banking reforms and strengthen the functional autonomy of RBI.

- The recent failures on internal and external controls like in the case of PNB leading to an alarming fraud, the failures of bank and NBFCs like Lakshmi Vilas Bank, Yes Bank, etc. where all stakeholders lost money and credibility have given rise to the need of new regulations with a very high degree of supervisory mechanism and corporate governance which has strong Information Technology (IT) and Artificial Intelligence (AI) enabled platform.

- Where a corporate house is a promoter, strict regulations on the use of funds held with the bank and monitoring of related party transactions will be essential.

- Fit and proper criterion needs to be foolproof and the common citizens should become the beneficiaries in the process.