Strengthening MSMEs for Economic Resilience | 27 Nov 2025

For Prelims: MSMEs, Priority Sector Lending, Mudra, Non-performing Assets (NPA), Trade Receivables Discounting System), Samadhaan Portal, Khadi and Village Industries Commission (KVIC), NITI Aayog, Intellectual Property Rights (IPR), Cloud Computing.

For Mains: MSME sector's contribution to GDP, employment, and exports, alongside challenges like credit gaps, delayed payments, and needed policy interventions.

Why in News?

The Delayed Payments Report 3.0, “MSME’s Access to Finance and Timely Payments” highlights that many MSMEs face challenging conditions that limit their growth and contribution to the Indian economy, underscoring the need to strengthen innovation, and competitiveness in the sector.

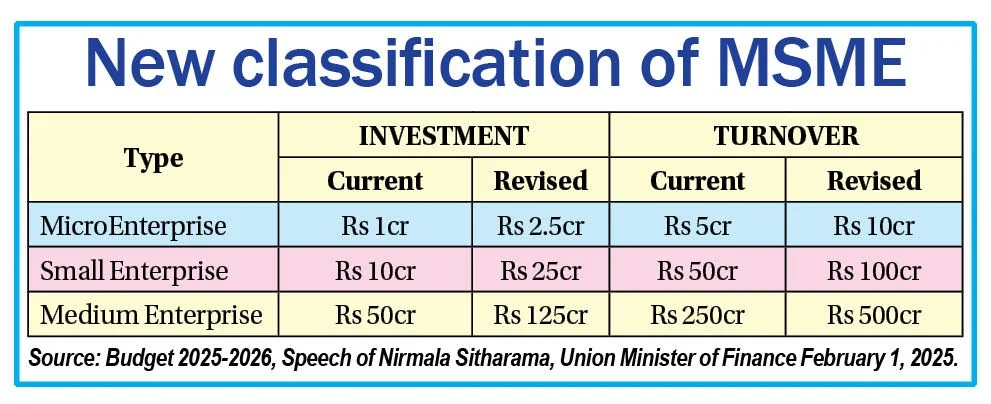

What are Micro, Small, and Medium Enterprises (MSMEs)?

- About: Micro, Small, and Medium Enterprises (MSMEs) are businesses classified according to their investment in plant & machinery or equipment and annual turnover.

- They are vital to India's economy, fostering entrepreneurship, creating employment, and driving industrialization in rural and semi-urban areas.

- Classification of MSMEs:

- MSME Regulation in India: The Micro, Small, and Medium Enterprises Development Act, 2006 addresses MSME issues, establishes a National Board, defines enterprise, and empowers the Central Government to boost MSME competitiveness.

- In 2007, the Ministry of Micro, Small, and Medium Enterprises was formed which develops policies, facilitates programs, and monitors implementation to support MSMEs.

What Role do MSMEs Play in Driving the Growth of the Indian Economy?

- Engine of Economic Growth & Employment: MSMEs contribute around 29% to India’s Gross Domestic Product (GDP) and around 36% to manufacturing output.

- It employs over 120 million people. For example, the textile industry employs millions in spinning, weaving, and apparel manufacturing.

- Driving Exports & Global Trade: MSMEs account for nearly 45% of India’s total exports, boosting India’s position in global trade. The handicraft sector, dominated by small enterprises, contributes about 40% of global handmade carpet exports.

- Rural Development & Inclusivity: MSMEs drive rural industrialization and inclusive growth, aligning with Dr. APJ Abdul Kalam’s PURA (Providing Urban Amenities in Rural Areas) vision. Institutions like Khadi and Village Industries Commission (KVIC), mainly small-scale units, aid in balanced regional development.

- Catalyzing Innovation: India’s startup ecosystem—the third-largest globally—is predominantly MSME-driven, with innovations in e-commerce, fintech, and other emerging industries.

- Women Empowerment: According to the Udyam Registration Portal, over 20% of MSMEs are women-owned, reflecting growing female participation in entrepreneurship.

What are the Key Challenges Hindering MSME Growth in India?

Financial Hindrance (as per the Report)

- Delayed Payments: The value of delayed payments remains cripplingly high at Rs. 8.14 lakh crore. This ties up essential working capital, preventing businesses from investing in raw materials, new machinery, or even paying their employees on time.

- Unmet Credit Needs: The report estimates the unmet credit need is around Rs. 25 lakh crore.

- While bank loans have grown to Rs. 12.99 lakh crore, this still leaves a huge gap, forcing MSMEs to rely on expensive informal credit or forgo growth opportunities.

- Rigid Banking Practices: Credit policies like Priority Sector Lending and Mudra loans have widened coverage but fall short due to:

- Information asymmetry (banks lack the data to accurately assess the creditworthiness of small businesses).

- Punitive Non-performing Assets (NPA) classification norms, which make banks hesitant to lend to what they perceive as risky MSMEs, fearing the loans will be classified as stressed assets.

Other Hindrances

- Formalization Barrier: Fear of tax and regulatory scrutiny keeps small owners informal, limiting access to formal credit and government schemes; over 90% of MSMEs in India remain informal, according to NITI Aayog.

- Inadequate Access to Specialized Knowledge: MSMEs often lack affordable advisory services for exports, Intellectual Property Rights (IPR) filing, and quality certifications (ISO), keeping them out of high-value markets. They also miss mentorship networks to guide scaling and crisis management.

- Vulnerability to Global Supply Chain Shocks: Many MSMEs rely on imported raw materials, making them vulnerable to pandemics, geopolitical conflicts, or shipping crises, which disrupt supply chains and raise input costs.

- E.g., India's exports contracted by 9.3% in August 2024 due to Red Sea disruptions.

- Limited Market Access: MSMEs face limited marketing and digital reach, reduced competitiveness from high tariffs (e.g., US 50% tariffs), and higher per-unit costs due to small size, constraining exports and profitability.

- A constant struggle for survival due to the working capital crisis leaves little capital for investment in research and development (R&D), new technologies, or upgrading machinery.

Key Committees on Strengthening MSMEs

- Standing Committee on Finance Report on MSME Credit (April 2022):

- Cash-flow Based Lending: Shift from asset-backed to real-time cash-flow based loans, linking GSTIN to account aggregator frameworks for better credit assessment.

- Accelerating MSME Formalisation: Encourage GST registration by linking credit access to GST invoices, increasing formal credit use and reducing reliance on informal high-cost sources.

- Targeted Credit Guarantees: Provide guarantees to vulnerable sectors and regions (e.g., salons, tour agencies, rural MSMEs) to ensure financial support during crises.

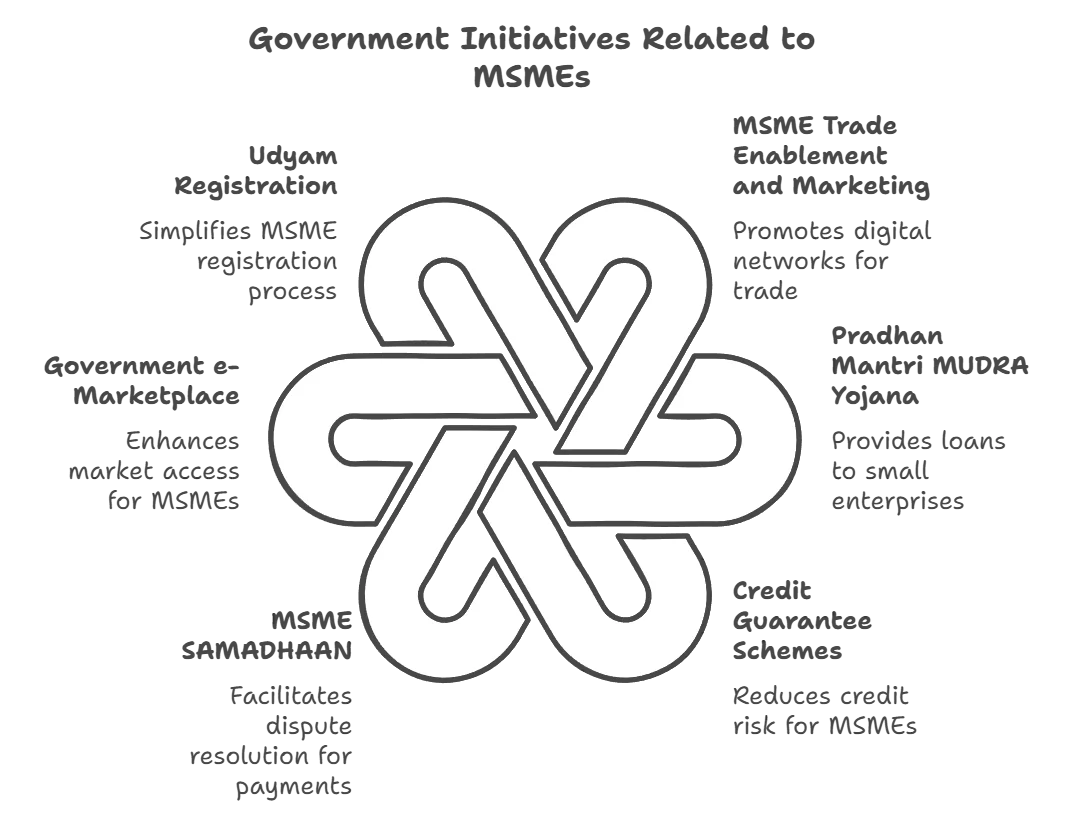

- Strengthening SIDBI’s Role: Inject Rs 5,000–10,000 crore into SIDBI to finance NBFCs and lower borrowing costs (e.g., Udyam Assist Platform for registration and financial linkages).

- UK Sinha Committee (2019): It recommended a Rs 5,000 crore stressed asset fund for MSMEs affected by demonetisation, GST, and liquidity crises, and doubling collateral-free loan limits from Rs 10 lakh to Rs 20 lakh for Mudra borrowers, SHGs, and MSMEs.

- Abid Hussain Committee (1997): It recommended that future policy should focus on promotion over protection, provide training and marketing support, and develop infrastructure in enterprise clusters.

- Nayak Committee (1992): Banks must provide at least 20% of a business’s turnover as finance, with the business contributing 5% as margin.

What Key Strategies can Help Transform India’s MSME sector?

- Promote Alternative Financing: Promote Invoice Discounting, Peer-to-Peer (P2P) lending, and venture debt for high-growth MSMEs. Create a public credit registry using GST, utility bills, and Udyam data to enable cash-flow-based lending over collateral-based lending.

- Market Access: Collaborate with e-commerce platforms to create low-fee, MSME-only storefronts with support for onboarding, cataloging, and digital marketing.

- Support export consortia through grants and logistics, helping MSME clusters meet large orders and international standards.

- Technology Adoption: Provide financial grants for MSMEs to adopt cloud computing, and automated machinery to boost productivity, and set up sector-specific tech clinics offering affordable consultancy for technical upgrades.

- Strengthen the MSME Samadhaan Portal: Enforce automated penalties on large corporations that delay MSME payments beyond 45 days, and implement a One-Time Settlement Scheme to clear statutory dues for micro-enterprises, reducing legal burdens.

- Fostering Resilience: Promote cluster-based development with common facility centers (for testing, design, R&D) and shared infrastructure (effluent treatment, warehousing) to reduce costs, and incentivize green practices through tax benefits, faster loans, and ESG certifications.

Conclusion

The MSME sector is crucial for India’s economic growth, employment, and exports, but its potential is limited by a credit gap, delayed payments, and technological obsolescence. A transformative strategy emphasizing formalization, digital financing, market access, and resilient infrastructure is essential to unlock its full impact.

|

Drishti Mains Question "The MSME sector is the backbone of the Indian economy, yet it remains its Achilles' heel." Critically analyze this statement in the context of the financial and structural challenges faced by MSMEs. |

Frequently Asked Questions (FAQs)

Q. What are MSMEs in India?

Micro, Small, and Medium Enterprises are businesses classified by investment in plant, machinery, and turnover, crucial for employment, exports, and rural industrialization.

Q. How do MSMEs contribute to India’s economy?

They contribute 29% of GDP, 36% of manufacturing output, nearly 45% of exports, and provide employment to over 120 million people.

Q. How do delayed payments impact the growth of MSMEs?

Delayed payments, valued at over ₹8.14 lakh crore, tie up essential working capital, crippling the ability of MSMEs to invest in raw materials, new machinery, and innovation.

UPSC Civil Services Examination, Previous Year Question:(PYQ)

Prelims

Q.1 What is/are the recent policy initiative(s)of Government of India to promote the growth of the manufacturing sector? (2012)

- Setting up of National Investment and Manufacturing Zones

- Providing the benefit of ‘single window clearance’

- Establishing the Technology Acquisition and Development Fund

Select the correct answer using the codes given below:

(a) 1 only

(b) 2 and 3 only

(c) 1 and 3 only

(d) 1, 2 and 3

Ans: (d)

Q2. Which of the following can aid in furthering the Government’s objective of inclusive growth? (2011)

- Promoting Self-Help Groups

- Promoting Micro, Small and Medium Enterprises

- Implementing the Right to Education Act

Select the correct answer using the codes given below:

(a) 1 only

(b) 1 and 2 only

(c) 2 and 3 only

(d) 1, 2 and 3

Ans: (d)

Q3. Consider the following statements with reference to India : (2023)

- According to the Micro, Small and Medium Enterprises Development (MSMED) Act, 2006, the ‘medium enterprises’ are those with investments in plant and machinery between `15 crore and `25 crore.

- All bank loans to the Micro, Small and Medium Enterprises qualify under the priority sector.

Which of the statements given above is/are correct?

(a) 1 only

(b) 2 only

(c) Both 1 and 2

(d) Neither 1 nor 2

Ans: (b)

Mains

Q.1 “Industrial growth rate has lagged behind in the overall growth of Gross-Domestic-Product(GDP) in the post-reform period” Give reasons. How far are the recent changes in Industrial Policy capable of increasing the industrial growth rate? (2017)

Q.2 Normally countries shift from agriculture to industry and then later to services, but India shifted directly from agriculture to services. What are the reasons for the huge growth of services vis-a-vis the industry in the country? Can India become a developed country without a strong industrial base? (2014)