Rising Household Debt in India | 05 Nov 2025

For Prelims: Reserve Bank of India, Mutual funds, International Monetary Fund, Systematic Investment Plan

For Mains: Macroeconomic stability, Drivers of unsecured consumption credit and its spillover risks to secured portfolios

Why in News?

The Reserve Bank of India (RBI) notes that since 2019-20, Indian households have been taking on financial debt far more quickly than they are building financial assets.

- The trend reflects evolving savings behavior, especially with mutual funds gaining traction, and raises concerns about household financial health and macroeconomic stability.

What are the Trends in India’s Household Financial Health?

- Debt Outpacing Asset Creation: Household financial liabilities grew 102% between 2019-20 and 2024-25, compared with a 48% rise in assets.

- Borrowing is expanding almost twice as fast as saving, reflecting higher credit dependence.

- Weaker Savings Relative to GDP: Fresh financial assets fell from 12% of GDP (2019-20) to 10.8% (2024-25).

- Liabilities as a share of GDP increased from 3.9% to 4.7%, peaking at 6.2% in 2023-24 before easing.

- The divergence highlights weaker household balance sheets and reduced capacity to absorb shocks.

- Deposits Remain Dominant: Deposits in commercial banks made up 32% of total household financial assets added in 2019-20, which grew marginally to 33.3% by 2024-25.

- This shows households are adding other investment options like mutual funds while still keeping bank deposits as their main choice.

- Other avenues like life insurance, provident and pension funds, equity, and small savings kept a largely stable share between 2019-20 and 2024-25.

- Rise of Mutual Fund Investment: Mutual funds jumped from 2.6% in 2019-20 to 13.1% by 2024-25.

- This shift reflects growing risk appetite, better access, and a search for higher returns as financial literacy improves.

- Shift away from Cash: Currency share in new assets dropped from 11.7% in 2019-20 to 5.9% in 2024-25.

- It suggests a broader move toward financial instruments and greater digital adoption.

What are the Implications of Rising Household Debt?

- Economic Implications: Rising household debt boosts growth in the short run but drags the growth 3–5 years later.

- An International Monetary Fund (IMF) study found that a 5% point increase in the ratio of household debt to GDP over a three-year period is associated with a 1.25% point decline in real GDP growth three years later with higher unemployment.

- High share of consumption borrowing limits long-term wealth creation and productive capital formation.

- Financial Sector Implications: According to the SBI report, the debt level stands at about 42% of GDP, lower than the 49.1% average among emerging market economies (EMEs).

- This is supported by healthier credit behaviour, with nearly two-thirds of household loans rated prime or above-prime, indicating contained credit risk. However, rising unsecured consumption loans raise vulnerability.

- According to the IMF, a 1-percentage-point rise in household debt-to-GDP increases the probability of a future banking crisis by around 1 percentage point.

- Household-Level Implications: According to the Financial Stability Report (FSR) 2024 by the RBI, rising debt alongside falling household assets suggests more borrowing is being used for consumption rather than asset creation, a worrying shift.

- Increasing consumption-driven borrowing, especially among low-income groups, reduces the income multiplier effect since more income goes to debt repayment instead of spending.

- A high share of unsecured loans among poorer households pushes them toward financial marginalisation and long-term instability.

- Macroeconomic Stability Implications: High indebtedness increases sensitivity to inflation and interest-rate shocks.

- In downturns, indebted households may sharply cut spending, amplifying macroeconomic volatility..

- If defaults increase, housing loans and other secured assets may slip into Non-Performing Assets (NPAs) transmitting stress to the banking system.

What are the Challenges in Household Asset Creation in India?

- Low and Unstable Incomes: Slow wage growth and income insecurity, especially in the informal sector (80–85% of workers are employed informally), limit regular saving.

- High Cost of Living: Rising expenses on essentials, healthcare, and education reduce money available for long-term investments.

- High dependence on Borrowing: Increasing use of loans for consumption leaves less room to build assets.

- Weak financial Literacy: Limited understanding of savings products, risk, and long-term planning restricts participation in financial markets.

- Behavioural factors: Aspirational spending and low willingness to take calculated investment risks hinder steady asset creation.

- Rural–Urban Disparity: Periodic Labour Force Survey (PLFS) data shows rural households spend a larger share of income on essentials, leaving less for investment compared to urban families, widening asset inequality.

What Steps can be Taken to Strengthen Household Asset Creation and Manage Debt Risks?

- Expand Financial Literacy Access: Expand financial literacy through National Centre for Financial Education (NCFE) under the National Strategy for Financial Education, RBI, and Securities and Exchange Board of India (SEBI), integrate basic financial planning into education and skilling.

- Promote low-cost fintech advisory and simplified savings products to help small households build diversified portfolios.

- Strengthen Social Security Coverage: Broaden social security for informal workers through schemes like Pradhan Mantri Shram Yogi Maan-dhan (PM-SYM) and PM-SVANidhi, and promote automatic enrolment in pension and insurance plans to strengthen safety nets and cut emergency borrowing.

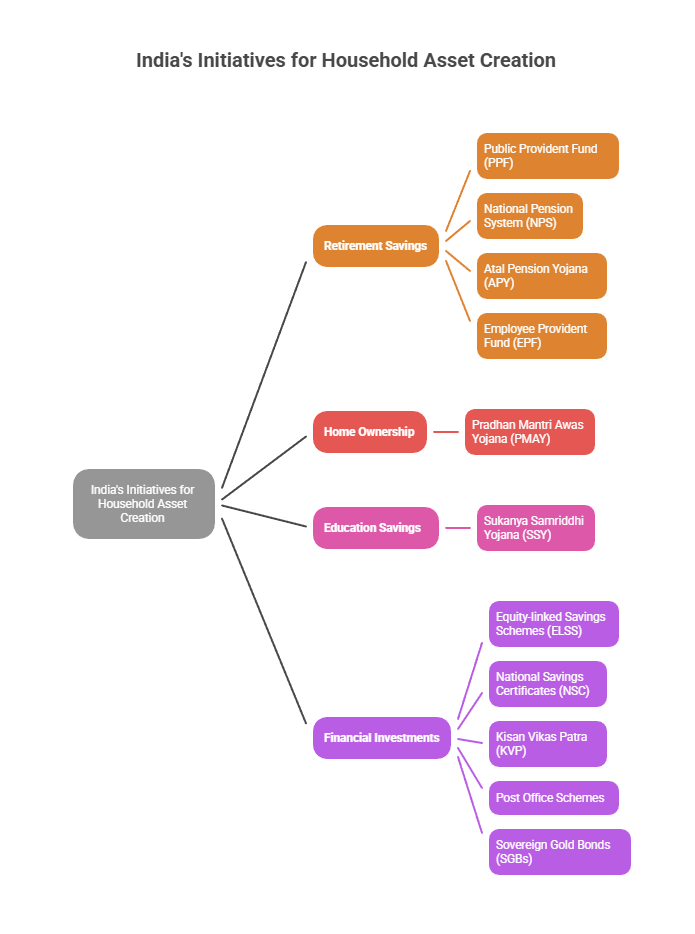

- Promote long-term savings instruments: Promote wider use of Sovereign Gold Bonds (SGB), and Equity-Linked Savings Scheme (ELSS), and systematic investment plan (SIPs) to build long-term wealth.

- Borrowing for Asset Creation: Incentivise credit for housing, education, and small business over unsecured consumption loans. Expand credit guarantee frameworks to reduce informal borrowing.

- Macroprudential Monitoring: RBI should closely monitor household leverage trends for signs of systemic risk. Create early warning systems for excessive credit accumulation.

- Enhance Income Stability: Support labour-intensive sectors, MSMEs, and skilling initiatives to boost steady earnings and improve saving capacity.

Conclusion

Household debt is rising much faster than asset creation, with more borrowing going toward consumption than wealth building. Strengthening savings habits, social security, and productive credit use will be key to maintaining household and economic stability.

|

Drishti Mains Question: Discuss the impact of consumption-led borrowing on the income multiplier and inclusive growth. What targeted reforms can raise asset creation among low-income households? |

Frequently Asked Questions (FAQs)

1. What are mutual funds?

A mutual fund pools money from many investors and invests it in stocks, bonds, or other securities to earn returns; they are professionally managed and market-linked.

2. What is the household debt-to-GDP ratio?

It measures household debt as a share of the country’s GDP; for India, it is about 42–43%, lower than the 49% average for emerging market economies.

3. What is the main trend in Indian household finance?

Debt is rising much faster than asset creation, with household liabilities growing about 102% compared to a 48% rise in assets between 2019-20 and 2024-25.

4. Why is rising unsecured borrowing a concern?

Many borrowers with personal/credit-card loans also have home/vehicle loans; default in one loan can turn all exposure into NPAs, increasing financial stress.

UPSC Civil Services Examination, Previous Year Question

Prelims

Q. In a given year in India, official poverty lines are higher in some States than in others because (2019)

(a) poverty rates vary from State to State

(b) price levels vary from State to State

(c) Gross State Product varies from State to State

(d) quality of public distribution varies from State to State

Ans: (b)

Q. As per the NSSO 70th Round “Situation Assessment Survey of Agricultural Households”, consider the following statements: (2018)

- Rajasthan has the highest percentage share of agricultural households among its rural households.

- Out of the total agricultural households in the country, a little over 60 percent belong to OBCs.

- In Kerala, a little over 60 percent of agricultural households reported to have received maximum income from sources other than agricultural activities.

Which of the statements given above is/are correct?

(a) 2 and 3 only

(b) 2 only

(c) 1 and 3 only

(d) 1, 2 and 3

Ans: (c)

Mains

Q. Among several factors for India’s potential growth, the savings rate is the most effective one. Do you agree? What are the other factors available for growth potential? (2017)