Deepening the Corporate Bond Market in India | 19 Dec 2025

Why in News?

NITI Aayog has released Deepening the Corporate Bond Market in India report emphasizing that a more efficient corporate bond market is crucial for expanding market access, improving liquidity, and enhancing investor participation.

Summary

- India’s corporate bond market has expanded but remains shallow and illiquid due to regulatory overlap, restrictive investment mandates, insolvency delays, and weak risk-management infrastructure.

- NITI Aayog recommends a 6-year roadmap of regulatory simplification, product innovation, and tech integration to build a ₹100–120 trillion market by 2030.

What is the Current State of India's Corporate Bond Market?

- Significant Growth, Yet Untapped Potential: The market has expanded from Rs 17.5 trillion in FY2015 to Rs 53.6 trillion in FY2025, growing at ~12% CAGR (Compound annual growth rate).

- However, at 15-16% of GDP, it remains shallow compared to peers like South Korea (79%) and Malaysia (54%).

- Concentrated and Institutional: Fundraising through bonds is now comparable to bank credit, but the market is dominated by private placements (98% of issuances) and top-rated (AAA/AA) borrowers.

- Participation from MSMEs, retail investors (<2%), and foreign portfolio investors is minimal.

- Liquidity Challenges: The secondary market is illiquid with a low annual turnover ratio (0.3), driven by a buy-and-hold approach by institutional investors like insurance and pension funds.

- Future Potential: With continued reforms and innovation, India’s corporate bond market could exceed Rs 100–120 trillion by 2030, becoming a pillar of financial stability and growth.

Why is a Deep Corporate Bond Market Essential for India?

- Viksit Bharat 2047 Requirement: India's ambition to become a USD 30 trillion economy with USD 18,000 per capita income requires a robust financial system capable of mobilizing long-term, low-cost capital at scale.

- Financial Architecture Balance: Plays a pivotal role in achieving a balanced, resilient financial architecture by expanding funding avenues, and lowering borrowing costs by creating a competitive, liquid marketplace where diverse issuers can access long-term capital directly from a wide pool of investors.

- Capital Formation Engine: Channels institutional and household savings into productive sectors, and facilitates development of risk management instruments like credit derivatives and securitization.

- Reducing Banking Sector Risk: Diversified funding sources reduce reliance on banks, enabling them to focus on priority sectors and MSMEs while mitigating non-performing asset (NPA) buildup and credit concentration risk.

- Strengthens Monetary Policy Transmission: A deep corporate bond market strengthens monetary policy transmission by allowing interest rate changes to pass through faster and more transparently via a well-defined yield curve.

- It also provides a reliable benchmark yield curve for pricing credit risk across the economy.

What are the Key Challenges in Developing a Deep Corporate Bond Market?

- Regulatory Overlap & Complexity: Multiple regulators (SEBI, RBI, Ministry of Corporate Affairs) lead to fragmented compliance, increased costs, and delays, especially for new instruments.

- Stringent Investment Mandates: Institutional investors (insurance, pension funds) are often restricted by regulation to invest primarily in high-rated (AA and above) papers, starving lower-rated corporates of funds.

- Limited enforcement capacity of debenture trustees and gaps in bondholder protection undermine investor confidence, especially in lower-rated debt.

- Weak Insolvency Recovery & Infrastructure: Despite the Insolvency and Bankruptcy Code (IBC), resolution processes face delays (average 713 days vs. 330-day mandate) and declining recovery rates, affecting investor confidence.

- High Costs & Tax Disincentives: High issuance/listing costs, complex Tax Deduction at Source (TDS) rules on interest, and less favourable capital gains tax treatment compared to equities make bonds less attractive.

- Underdeveloped Ecosystem: Shallow markets for risk-mitigation tools (like Credit Default Swaps), securities lending, and a fragmented data infrastructure hinder growth. It also reduces price transparency, constraining efficient risk assessment and trading activity.

Reforms Taken to Strengthen the Corporate Bond Market

- RBI: Launched tri-party repos, Partial Credit Enhancement (PCE), the Retail Direct platform, and the Voluntary Retention Route (VRR) for Foreign portfolio investment (FPI).

- Government: Enacted the IBC, launched the Corporate Debt Market Development Fund (CDMDF) as a safety net, and provided incentives for municipal bonds under AMRUT 2.0.

- Parliamentary Recommendations: The Select Committee of Lok Sabha has proposed fixing a 3-month time limit for the National Company Law Appellate Tribunal (NCLAT) to decide insolvency appeals.

- It recommended including registered value within the definition of service provider under the IBC, and inserting a clear definition for registered valuer.

- Additionally, it proposed allowing multiple resolution plans for a corporate debtor during the corporate insolvency resolution process (CIRP).

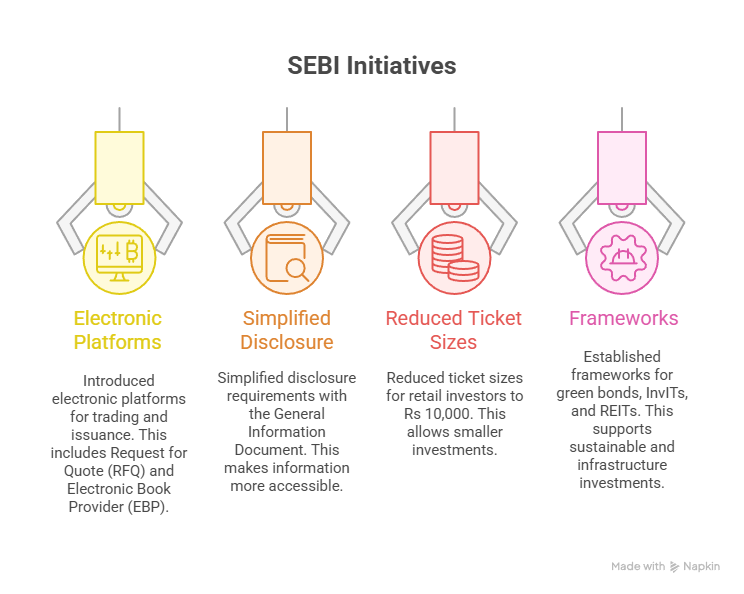

- SEBI Initiatives:

What is the Proposed Roadmap for Deepening the Corporate Bond Market as per NITI Aayog?

NITI Aayog proposes a 3-phase, 6-year reform strategy that prioritises regulatory simplification and strengthening of market infrastructure in the initial stages, before advancing toward deeper institutional reforms and global integration, thereby minimising systemic risks:

- Phase I (1-2 Years, Strengthen Foundations): Streamline regulations across SEBI, RBI, MCA. Enhance retail access via digital platforms and investor education.

- Improve insolvency timelines and strengthen debenture trustee roles.

- Pilot AI-driven credit scoring for Small and Medium Enterprises (SMEs) and encourage voluntary market-making.

- Phase II (2-4 Years, Expand & Innovate): Introduce innovative products like covered bonds (Backed by high-quality collateral like public-sector loans), targeted subsidy bonds, and fractional bond funds.

- Develop dedicated platforms for SME bonds and lower-rated debt.

- Review investment mandates for insurers/pension funds to allow more diversification.

- Phase III (4-6 Years, Integrate & Mature): Establish a unified bond market regulator or a high-powered statutory task force.

- Leverage advanced tech (Blockchain, AI) for a secure, digital bond ecosystem.

- Gradual integration with global settlement systems (e.g., Euroclear) to attract stable foreign capital and deepen market resilience.

Conclusion

India’s corporate bond market has expanded but remains shallow and fragmented, limiting its ability to mobilize long-term capital. Coordinated reforms in regulation, investor diversification, insolvency efficiency, and market infrastructure are essential to make it a Rs 100–120 trillion financing pillar for Viksit Bharat 2047.

|

Drishti Mains Question: Critically analyze the structural and regulatory challenges hindering the deepening of India’s corporate bond market. What measures have been taken, and what further reforms are needed? |

Frequently Asked Questions (FAQs)

Q. What is the size of India’s corporate bond market?

It stands at Rs 53.6 trillion (FY2025), about 15–16% of GDP, indicating significant growth but shallow depth compared to global peers.

Q. Why is secondary market liquidity low?

Dominance of buy-and-hold institutional investors like insurance and pension funds results in a turnover ratio of just 0.3.

Q. What is the projected potential size of India's corporate bond market by 2030?

With sustained reforms, the market has the potential to exceed ₹100-120 trillion by 2030.

UPSC Civil Services Examination, Previous Year Questions (PYQs)

Prelims

Q. Consider the following statements: (2018)

- Capital Adequacy Ratio (CAR) is the amount that banks have to maintain in the form of their own funds to offset any loss that banks incur if the account-holders fail to repay dues.

- CAR is decided by each individual bank.

Which of the statements given above is/are correct?

(a) 1 only

(b) 2 only

(c) Both 1 and 2

(d) Neither 1 nor 2

Ans: (a)

Q. ‘Basel III Accord’ or simply ‘Basel III’, often seen in the news, seeks to (2015)

(a) develop national strategies for the conservation and sustainable use of biological diversity

(b) improve banking sector’s ability to deal with financial and economic stress and improve risk management

(c) reduce the greenhouse gas emissions but places a heavier burden on developed countries

(d) transfer technology from developed countries to poor countries to enable them to replace the use of chlorofluorocarbons in refrigeration with harmless chemicals

Ans: (b)

Mains

Q. Do you agree with the view that steady GDP growth and low inflation have left the Indian economy in good shape? Give reasons in support of your arguments? (2019)