Strategic Disinvestment | 02 Jan 2020

Why in News

The government's plans to sell Bharat Petroleum Corporation (BPCL), Container Corporation of India (Concorp) and Air India are unlikely to conclude by March 2020. It might result in missing the disinvestment target of Rs 1.05 trillion for 2019-2020 by a wide margin.

Disinvestment

- Disinvestment means sale or liquidation of assets by the government, usually Central and state public sector enterprises, projects, or other fixed assets.

- The government undertakes disinvestment to reduce the fiscal burden on the exchequer, or to raise money for meeting specific needs, such as to bridge the revenue shortfall from other regular sources.

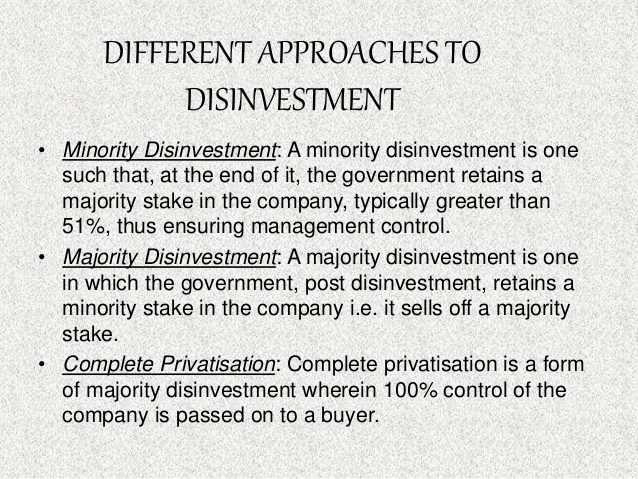

- Strategic disinvestment is the transfer of the ownership and control of a public sector entity to some other entity (mostly to a private sector entity).

- Unlike the simple disinvestment, strategic sale implies a kind of privatization.

- The disinvestment commission defines strategic sale as the sale of a substantial portion of the Government shareholding of a central public sector enterprises (CPSE) of upto 50%, or such higher percentage as the competent authority may determine, along with transfer of management control.

- Strategic disinvestment in India has been guided by the basic economic principle that the government should not be in the business to engage itself in manufacturing/producing goods and services in sectors where competitive markets have come of age.

- The economic potential of such entities may be better discovered in the hands of the strategic investors due to various factors, e.g. infusion of capital, technology up-gradation and efficient management practices etc.

Disinvestments- A Historical Perspective

- For the first four decades after Independence, India pursued a path of development in which the public sector was expected to be the engine of growth.

- However, the public sector overgrew itself and its shortcomings started manifesting in low capacity utilisation and low efficiency due to over manning, low work ethics, over capitalisation due to substantial time and cost overruns, inability to innovate, take quick and timely decisions, large interference in decision making process etc. Hence, a decision was taken in 1991 to follow the path of Disinvestment.

- The change process in India began in the year 1991-92, when 31 selected PSUs were disinvested for Rs.3,038 crore.

- In August 1996, the Disinvestment Commission, chaired by G V Ramakrishna was set up to advise, supervise, monitor and publicize gradual disinvestment of Indian PSUs. However, the Disinvestment Commission ceased to exist in May 2004.

- The Department of Disinvestment was set up as a separate department in December, 1999 and was later renamed as Ministry of Disinvestment in September, 2001. From 27th May, 2004, the Department of Disinvestment was brought under the Ministry of Finance.

- The Department of Disinvestment has been renamed as Department of Investment and Public Asset Management (DIPAM) from 14th April, 2016 which has been made the nodal department for the strategic stake sale in the Public Sector Undertakings (PSUs).

- National Investment Fund (NIF) was constituted in November, 2005, into which the proceeds from disinvestment of Central Public Sector Enterprises were to be channelized.

Recent Developments

- In 2015, the Government reinitiated the policy of strategic disinvestment in order to open up sectors for private enterprise to bring efficiency in management that would contribute to general economic development

- The Government had set a disinvestment target of 1.05 lakh crore rupees for the financial year 2019-20.

- Recently cabinet has cleared the plan to sell 53.3% of its stake in BPCL, 63.8% of SCI and 30.8% of CONCOR to strategic buyers. 74.2% of its stake with THDCIL and 100% of NEEPCO is to be sold to NTPC.

Main objectives of Disinvestment in India

- To meet the budgetary needs

- To reduce fiscal deficit

- To improve public finances and overall economic efficiency

- To diversify the ownership of PSU for enhancing efficiency of individual enterprise

- To raise funds for technological upgradation, modernization and expansion of PSUs

- To raise funds for golden handshake (VRS)

- To introduce, competition and market discipline

- To fund growth and development programmes

- To encourage wider share of ownership

- To depoliticise non-essential services

- Transfer of Commercial Risks

Importance of Disinvestment

- In the short run, it is helpful in financing the increasing fiscal deficit.

- Disinvestment funds can be utilised for long-terms goals such as:

- Financing large-scale infrastructure development.

- Investing in the economy to encourage spending

- Expansion and Diversification of the firm.

- Repayment of Government Debts: Almost 40-45% of the Centre’s revenue receipts go towards repaying public debt/interest

- Investing in social programs like health and education

- It can help in generating a better environment for investment.

- Disinvestment also assumes significance due to the prevalence of an increasingly competitive environment, which makes it difficult for many PSUs to operate profitably. This leads to a rapid erosion of the value of the public assets making it critical to disinvest early to realize a high value.

- It is expected that the strategic buyer/acquirer may bring in new management/technology/investment for the growth of these companies and may use innovative methods for their development.

- While government presence may be a necessary evil in strategic sectors such as defence or oil exploration, there’s really no call for it to be running fuel retailing outlets, building ships or running container freight operations. Government presence in such non-strategic sectors not only distorts competitive dynamics for private players, it also results in consumers and taxpayers bearing the brunt of inefficient PSU operations.

- In other words, ‘government has no business being in business’

- While strategic sale deals in the past have seen a few mis-steps, they’ve also yielded convincing success stories like Hindustan Zinc’s, which has seen a hundred-fold increase in its profits on the back of a six-fold expansion in capacities, since its takeover by Vedanta in 2002.

Challenges of Disinvestments

- Sale of profit-making and dividend paying PSUs would result in the loss of regular income to the Government

- There would be chances of “Asset Striping” by the strategic partner. Most of the PSUs have valuable assets in the plant and machinery, land and buildings, etc.

- Strategic and National Security Concerns: Strategic Disinvestment of Oil PSUs is seen by some experts as a threat to National Security since Oil is a strategic natural resource and possible ownership in the foriegn hand is not consistent with our strategic goals.

- Disinvestment affects labour forces' social security.

- It also raises concerns about cronyism.

- The depressed state of the markets and the paucity of reasonable buyers would land in a bad deal.

- Using funds from disinvestment to bridge the fiscal deficit is an unhealthy and a short term practice. It is said that it is the equivalent of selling 'family silver' to meet short term monetary requirements.

- Complete Privatisation may result in public monopolies becoming private monopolies, which would then exploit their position to increase costs of various services and earn higher profits

- A majority stake sale done to another CPSE results in no real change in ownership, and is thus just hogwash.

Conclusion

- It needs to be ensured that Privatisation (Strategic Disinvestment ) leads to greater competition in all cases.

- It should be ensured that the proceeds of such strategic sales aren’t frittered away in interest or salary payouts but are reinvested prudently in long-term infrastructure assets that can yield enduring returns to the economy.

- To allay concerns of cronyism, the strategic sale process needs to be fair and transparent with a minimum reserve price that does justice to the valuable assets being auctioned off. A third-party valuation of every PSU’s assets and a minimum number of bidders, should be necessary pre-conditions to going ahead with each sale.