Essar Insolvency Case | 16 Nov 2019

Why in News

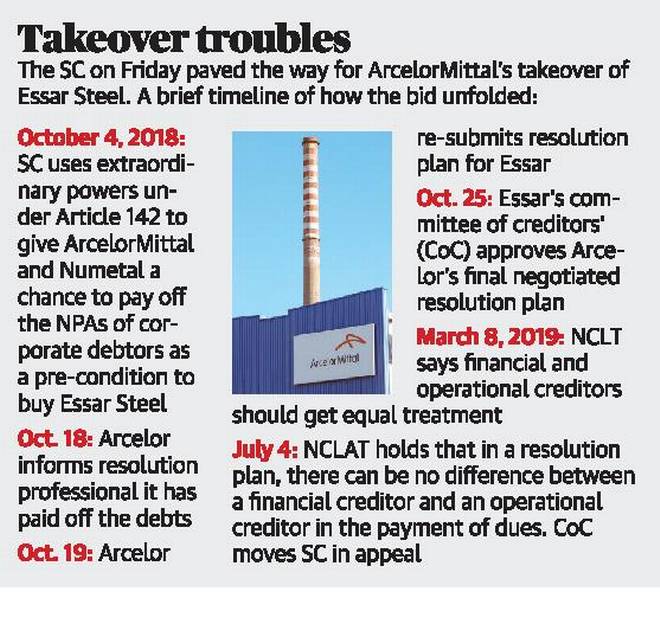

The Supreme Court has recently given its judgement in the Essar Insolvency case. The Judgement has paved the way for ArcelorMittal and Nippon Steel to take over debt-laden Essar Steel.

Background

- In March 2019, National Company Law Tribunal (NCLT) approved global steel-giant ArcelorMittal’s bid for Essar Steel.

- The Committee of Creditors (CoC) approved the resolution plan offered by the ArcelorMittal. Under the resolution plan, ArcelorMittal offered an advance cash payment of about ₹42,000 crore to the financial creditors and capital infusion of ₹8,000 in the next few years. However, the offer did not have much for operational creditors to Essar Steel.

- In 2019, the National Company Law Appellate Tribunal (NCLAT) cleared the CoC’s plan but changed the financial distribution plan by ordering an equal recovery plan for all creditors, including financial and operational creditors.

Highlights of the Judgement

- Wisdom of CoC: It is the commercial wisdom of the requisite majority (66%) of the CoC under the Insolvency and Bankruptcy Code (IBC) to negotiate and accept a resolution plan, which may involve differential payment to different classes of creditors.

- Principle of Equality: The Court held that the equality principle cannot be stretched to treating unequals equally. This will destroy the very objective of the IBC to resolve stressed assets. Equitable treatment is to be accorded to each creditor depending upon the class to which it belongs: secured or unsecured, financial or operational.

- Restriction on Tribunals: Tribunals have no “residual equity jurisdiction” to interfere in the merits of a business decision taken by the CoC. This implies that the NCLT and NCLAT cannot interfere with the commercial decisions taken by the CoC.

- Financial vs Operational Creditors: The Court upheld the primacy of financial creditors over operational creditors in the distribution of funds received under the corporate insolvency scheme.

- The Court explained that financial creditors are capital-providers for companies, i.e. help companies to purchase assets and run business operations.

- Operational creditors, in a way, are beneficiaries of amounts lent by financial creditors.

- Relaxation of Resolution Deadline: The Supreme Court has done away with the 330-day mandatory deadline for the resolution of insolvency and bankruptcy cases after which liquidation is invoked. The bench allowed a bit of flexibility by allowing exceptions where the resolution plan is on the verge of being finalised.

- The 330-day mark is violation of Article 14 (right to equal treatment ) of the Constitution and Article 19(1)(g) ( Right to carry any business) of the Constitution.

Likely Impact of the Judgement

- Impact on Banks: Banks will recover Rs. 42,000 crore against admitted debts of Rs. 49,473 crore- a recovery of about 85% compared to the average recovery of 53% in other resolution cases. This would help banks in boosting their capital adequacy.

- Speedy Resolution: The verdict is likely to reduce legal wrangling between financial and operational creditors and accelerate resolution process.

- Foreign Investment: It will attract investors who were getting wary of the nation’s bankruptcy process.

- India is trying to attract foreign capital to its bad loan cleanup, as it battles the worst nonperforming loan ratio among the world’s major economies.

- Upheld the Spirit of IBC: The removal of mandatory 330-day deadline will facilitate resolution, the ultimate objective of the IBC.

Insolvency Resolution Process in India

- Eligibility: Under IBC, companies (both private and public limited company) and Limited Liability Partnerships (LLP) can be considered as defaulting corporate debtors.

- A corporate debtor is any corporate organization which owes a debt to any person.

- Default Amount: The Insolvency and Bankruptcy Code can be triggered if there is a minimum default of Rs 1 lakh. This process can be triggered by way of filing an application before the National Company Law Tribunal (NCLT).

- Resolution Initiation: The process can be initiated by two classes of creditors which would include financial creditors and operational creditors.

- Creditors: A Creditor means any person to whom a debt is owed and includes a financial creditor, an operational creditor, etc.

- Financial Creditors: The financial creditor in simple terms is the institution that provided money to the corporate entity in the form of loans, bonds etc. E.g. banks.

- Operational Creditors: An operational creditor is the entity who has a claim for providing any of the four categories to the defaulted corporate- goods, services, employment and Government dues (central govt, state or local bodies).

- Appointment of Interim Resolution Professional: As soon as the matter is admitted by the NCLT, the NCLT proceeds with the appointment of an Interim Resolution Professional (IRP) who takes over the management of the defaulting debtor.

- Committee of Creditors (CoC): A committee consisting only of the financial creditors i.e. the CoC is formed by the IRP.

- Only operational creditors having aggregate dues of at least 10% of the total debt are invited into the meeting of CoC (Operational creditors are not a member of CoC). The operational creditors don’t have any voting power.

- Corporate Insolvency Resolution Process (CIRP): It includes necessary steps to revive the company such as raising fresh funds for operation, looking for new buyer to sell the company as going concern, etc.

- The CoC takes a decision regarding the future of the outstanding debt owed to it. The resolution plan can be implemented only if it has been approved by 66% of the creditors in the CoC

- Liquidation Proceedings: In the event a resolution plan is not submitted or not approved by the committee of creditors (COC), the CIRP process is deemed to have failed. In such a situation the liquidation proceedings commences subject to the order of the tribunal.