CBDC Pilot for Food Subsidy Distribution | 26 Feb 2026

India has launched a Central Bank Digital Currency (CBDC)-based food subsidy distribution pilot under Pradhan Mantri Garib Kalyan Anna Yojana (PMGKAY) in Puducherry, marks a significant reform in the delivery of food subsidy through the Public Distribution System (PDS) by integrating the Digital Rupee (e₹) into the Direct Benefit Transfer (DBT) framework.

- Programmable and Purpose-Bound Usage: A defining feature of this initiative is that the Subsidy is credited as programmable CBDC tokens directly into beneficiary wallets.

- They are redeemable exclusively for the purchase of entitled foodgrains at authorized Fair Price Shops (FPS), ensuring targeted usage and completely eliminating the possibility of fund diversion.

- System Efficiency and Transparency: This digital cash mechanism is instant, highly secure, and fully traceable, which significantly reduces friction, plugs leakages, and enhances accountability in the national food security ecosystem.

- The pilot is being implemented in coordination with the Government of Puducherry, Reserve Bank of India, Public Financial Management System (PFMS), and Canara Bank.

- Following its rollout in Puducherry, the initiative will be expanded in phases to other Union Territories and beneficiaries.

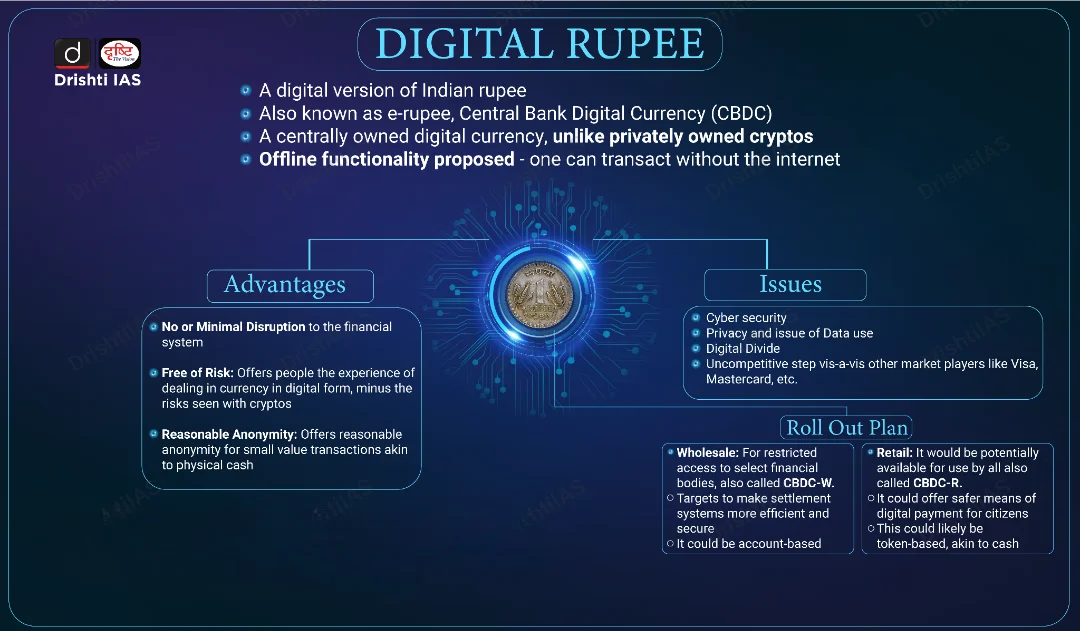

Central Bank Digital Currency

- About: It is the digital form of a country's fiat currency. Unlike the digital money in your traditional bank account (which is a liability of a commercial bank), a CBDC is issued directly by the country's central bank and represents a direct sovereign liability.

-

Digital Rupee (e₹) is India's official CBDC. It is recognized as legal tender, meaning it holds the exact same value as physical cash and can be exchanged one-to-one with paper currency.

-

-

Retail CBDC (e₹-R): Designed for the general public and everyday businesses. It operates via digital wallets provided by banks, offering a safe store of value and enabling instant peer-to-peer and peer-to-merchant transactions.

-

Because it mimics physical cash, no interest is paid on the wallet balance.

-

Wholesale CBDC (e₹-W): Restricted to financial institutions and intermediaries. It is engineered to streamline large-value transactions like secondary market trades in Government Securities and inter-bank lending by drastically reducing settlement costs and mitigating counterparty settlement risks.

-

Distinct from UPI: While Unified Payments Interface (UPI) is simply a payment interface that moves existing money between traditional bank accounts.

-

The Digital Rupee transactions settle instantaneously wallet-to-wallet without needing the commercial bank's backend ledger. However, for maximum convenience, e₹ apps are fully interoperable with existing UPI QR codes.

-

| Read more:Central Bank Digital Currency |