Capex Spending of Private Sector | 13 May 2025

For Prelims: E-commerce, Unified Payments Interface (UPI), Digital Public Infrastructure, production-linked incentive (PLI) schemes, NSSO (National Sample Survey Office), Fiscal deficit, National Infrastructure Pipeline.

For Mains: Role of Private Sector in Indian Economic Growth, Key Drivers Shaping India's Economic Growth Outlook, Major Challenges Hindering India’s Sustained Economic Growth.

Why in News?

The National Statistics Office (NSO), under the Ministry of Statistics and Programme Implementation (MoSPI), released its inaugural 'Forward-Looking Survey on Private Sector Capex Investment Intentions' survey.

- The survey was conducted under the Collection of Statistics Act, 2008, it aims to estimate trends in private corporate capital expenditure (capex) over five financial years, from 2021–22 to 2025–26.

What are the Trends in Private Sector CAPEX Investment?

- Overall Growth in Capex: Private sector capital expenditure (capex) rose by 66.3% over four years between FY 2021-22 and FY 2024-25. However, it is projected to decline by 25.5% in FY 2025-26, reflecting cautious planning by firms following a strong capex cycle in FY 2024-25.

- This decline is driven by factors such as high borrowing costs, weak demand, and geopolitical uncertainties.

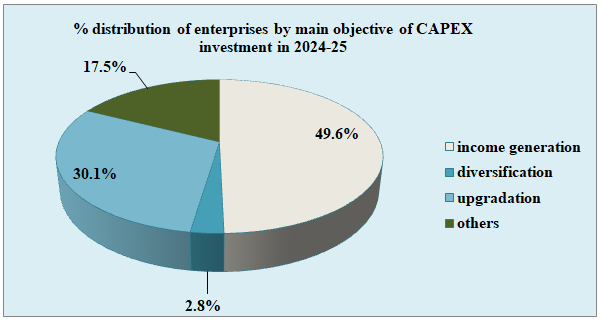

- Purpose and Nature of Investments: In FY25, 49.6% of enterprises invested for income generation, 30.1% for upgradation, and 2.8% for diversification.

- The estimated capex per enterprise for new asset purchases in FY25 was Rs 172.2 crore.

- Sectoral Distribution of Capex: Manufacturing received the highest share at 43.8%, followed by Information & Communication (15.6%) and Transportation & Storage (14%).

- Asset-wise, 53.1% of total capex was directed towards machinery & equipment, 22% to capital work-in-progress, and 9.7% to buildings and structures.

- Growth in Gross Fixed Assets (GFA): The average GFA per enterprise in the private corporate sector saw a growth of 27.5% from Rs 3,279.4 crore in 2022–23 to Rs 4,183.3 crore in 2023–24.

- The highest GFA was seen in the Electricity, Gas, Steam, and Air Conditioning Supply sector followed by Manufacturing.

- Gross Fixed Assets (GFA) refer to the total value of physical assets owned by an enterprise, such as machinery, buildings, and equipment, after accounting for depreciation.

What is Capex?

- About: Capex (Capital Expenditure) refers to funds spent on acquiring, upgrading, or maintaining physical assets like property, equipment, or technology. It’s a long-term investment recorded as an asset and depreciates over time. Examples include machinery purchases and facility upgrades.

- Unlike Operating expenses (Opex), which are the day-to-day costs of running a business, Capex involves substantial investments intended to generate long-term benefits.

- Capex Data: The Indian government allocates capex through its annual budget, presented by the Finance Minister.

- Capex Expenditure of Rs 11.21 lakh crore (3.1% of GDP) earmarked in FY2025-26.

- Significance: Capex plays a vital role in economic growth due to its high multiplier effect. It boosts ancillary industries, creates jobs, and enhances labour productivity.

- As a countercyclical fiscal tool, Capex stabilizes the economy and supports long-term revenue generation through asset creation.

- It also helps reduce liabilities via loan repayments and catalyses private investment, making it crucial for sustained economic development.

What are the Challenges Hindering Private Sector Capex?

- Geopolitical Uncertainty and Global Trade Disruptions: Heightened tensions (e.g., US-China tariffs, global sanctions) create unpredictability in trade and input costs.

- Industries reliant on imported materials are especially cautious due to supply chain vulnerabilities.

- High Borrowing Costs: Elevated interest rates increase the cost of financing large-scale projects, due to this companies prefer to use internal accruals rather than borrow from banks.

- Weak Consumer Demand: Low private consumption affects business confidence to invest in expanding capacity.

- Despite some recovery in demand post-Covid-19, it hasn't been robust enough to justify major greenfield investments.

- Lack of Greenfield Projects; Most current investments are brownfield (expansion of existing units), funded through internal funds.

- Greenfield investments (new units) that typically require bank funding are lacking, reducing overall capex visibility.

- Structural Bottlenecks: Delays in land acquisition and lack of labour reforms persist as major obstacles.

- Scarcity of skilled workers, exemplified by L&T's struggle to hire 40,000 workers, hampers project execution.

- Caution Due to IBC Experiences: Past bankruptcies (e.g., Jet Airways, Essar) under the Insolvency and Bankruptcy Code, 2016 have made firms more risk-averse. Fear of asset seizure leads to conservative financial planning.

- Low Capacity Utilisation Although some sectors (steel, cement, auto) report 75–80% utilisation, overall rates have dropped to 74.7% (Q3 FY24) from a peak of 76.3% in Q4 FY23. Without strong capacity use, firms see little incentive to expand further.

- Overconcentration of Investment: New private investments are mostly limited to a few large corporations like Reliance, Tata. A broader participation by India is essential for sustained economic growth.

What Can be Done to Enhance the Private Sector Capex?

- Strengthen Institutional Mechanisms and Credit Support: Strengthen the existing Revamp Project Monitoring Group (PMG) under the Cabinet Secretariat to ensure faster clearances of large private investment projects.

- Expanding the Emergency Credit Line Guarantee Scheme (ECLGS) for MSMEs and extending similar support to mid-sized manufacturing firms could significantly boost capex

- Utilize the Credit Guarantee Scheme for Startups (CGSS) to promote early-stage industrial and technological investments, encouraging innovation and growth in emerging sectors.

- Broaden Production Linked Incentive (PLI) Schemes: Introduce PLI for sectors like defence manufacturing, and precision engineering. Improve transparency and timeliness in PLI disbursements to build investor confidence.

- Improve Tax and Regulatory Framework: Reintroduce or enhance accelerated depreciation benefits for machinery and plant investment.

- Fastrack the National Logistics Policy (2022) which aims to reduce the cost of logistics from 13–14% of Gross Domestic Product (GDP) to 8–9%, improving the competitiveness of private manufacturers.

- De-risking Private Sector Investments: To de-risk private sector investments, promote the use of Infrastructure Investment Trusts (InvITs) and Real Estate Investment Trusts (REITs) in sectors such as roads, power, and railways.

- This approach will help attract private capital while distributing risks, thereby fostering investment in these critical sectors.

Conclusion

While private sector capex witnessed significant growth in the last few years, the projected decline in FY26 indicates a cautious investment sentiment amid uncertainties like high borrowing costs and global tensions. Nevertheless, the focus on upgradation and sectoral diversification reflects an evolving investment strategy aligned with economic stability.

|

Drishti Mains Question: What are the key challenges faced by the private sector in increasing capital expenditure in India? |

UPSC Civil Services Examination, Previous Year Questions (PYQs)

Prelims

Q. In the ‘Index of Eight Core Industries’, which one of the following is given the highest weight? (2015)

(a) Coal production

(b) Electricity generation

(c) Fertilizer production

(d) Steel production

Ans: (b)

Q. Increase in absolute and per capita real GNP do not connote a higher level of economic development, if: (2018)

(a) Industrial output fails to keep pace with agricultural output.

(b) Agricultural output fails to keep pace with industrial output

(c) Poverty and unemployment increase.

(d) Imports grow faster than exports.

Ans: (c)

Q. In a given year in India, official poverty lines are higher in some States than in others because: (2019)

(a) Poverty rates vary from State to State

(b) Price levels vary from State to State

(c) Gross State Product varies from State to State

(d) Quality of public distribution varies from State to State

Ans: (b)

Mains

Q.1 “Industrial growth rate has lagged behind in the overall growth of Gross-Domestic-Product(GDP) in the post-reform period” Give reasons. How far the recent changes in Industrial Policy capable of increasing the industrial growth rate? (2017)

Q.2 Normally countries shift from agriculture to industry and then later to services, but India shifted directly from agriculture to services. What are the reasons for the huge growth of services vis-a-vis the industry in the country? Can India become a developed country without a strong industrial base? (2014)