11 Years of Pradhan Mantri MUDRA Yojana | 10 Apr 2026

For Prelims: Pradhan Mantri Mudra Yojana (PMMY), Small Industries Development Bank of India (SIDBI), Credit Guarantee Fund for Micro Units (CGFMU), Account Aggregator.

For Mains: Significance of PMMY in promoting financial inclusion and entrepreneurship, achievements, and associated challenges.

Why in News?

The Prime Minister of India commended the success of the Pradhan Mantri Mudra Yojana (PMMY) on its 11th anniversary.

Summary

- PMMY has expanded financial inclusion by providing collateral-free loans to micro and small enterprises, boosting entrepreneurship, women's participation, and formalization of the economy.

- Challenges remain in scaling and impact, with issues like dominance of small loans, NPAs, and low value-addition; strengthening through a ‘credit-plus’ approach and Tarun Plus can enable sustainable growth.

What is the Pradhan Mantri MUDRA Yojana (PMMY)?

- About: Launched on 8th April 2015, PMMY is a flagship scheme of the Government of India aimed at providing collateral-free institutional credit to non-corporate, non-farm micro and small enterprises (MSEs).

- Objective: It focuses on promoting self-employment and bringing grassroots entrepreneurs into the formal financial system.

- The scheme acts as a cornerstone for India's financial inclusion program, which is built on three pillars: Banking the Unbanked, Securing the Unsecured, and Funding the Unfunded.

- Implementing Agency: It operates under the Department of Financial Services, Ministry of Finance.

- Funding Provision: Loans are extended by Member Lending Institutions (MLIs) such as Scheduled Commercial Banks (SCBs), Regional Rural Banks (RRBs), Non-Banking Financial Companies (NBFCs), and Micro Finance Institutions (MFIs).

- MUDRA (Micro Units Development & Refinance Agency Ltd.), a subsidiary of SIDBI, provides refinance support to these lending institutions but does not lend directly to borrowers.

- Credit Guarantee: The Credit Guarantee Fund for Micro Units (CGFMU) provides guarantee coverage for PMMY loans, mitigating the risk for lending institutions.

- Eligible Beneficiaries: Include individuals, proprietary concerns, partnership firms, private and public limited companies, and other legal entities.

- MUDRA Card: It provides a flexible, hassle-free credit facility to meet the working capital needs of small entrepreneurs.

- It functions as a RuPay debit card with an overdraft feature, allowing easy withdrawals, payments, and cost-effective credit usage.

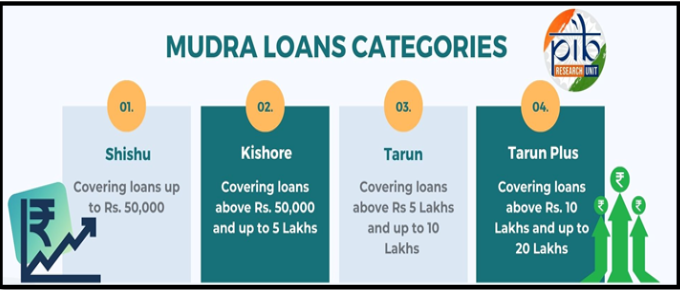

- Loan Categories under PMMY:

|

Category |

Loan Amount Range |

Share in Total Loans |

Purpose |

|

Shishu |

Up to Rs 50,000 |

74% |

Starting a business (very small scale, basic setup) |

|

Kishor |

Rs 50,000 – Rs 5 lakh |

24% |

Expanding early-stage business (buying tools, inventory) |

|

Tarun |

Rs 5 lakh – Rs 10 lakh |

2% |

Scaling established business (increase production, hire workers) |

|

Tarun Plus |

Rs 10 lakh – Rs 20 lakh |

0.004% |

Announced in the Union Budget 2024–25 it strengthens the objective of “Funding the Unfunded” by enabling further expansion of successful businesses that have already repaid their Tarun loans. |

What are the Key Achievements of PMMY?

- Massive Credit Outreach: Over the past decade, the scheme has sanctioned over 57 crore loans amounting to more than Rs. 40.07 lakh crore.

- Promoting Women Entrepreneurship: The scheme has been a major driver of Nari Shakti; women account for 67% (two-thirds) of all loan beneficiaries.

- Empowering Marginalized Communities: PMMY promotes social equity, with over 51% of the beneficiaries belonging to Scheduled Castes (SC), Scheduled Tribes (ST), and Other Backward Classes (OBC).

- Transition to Formal Economy: Over 12 crore accounts belong to first-time entrepreneurs, successfully pulling them out of the informal credit networks of local moneylenders and integrating them into the formal banking system.

- Unprecedented Scale: Since its inception in the 2015-16 financial year, the scheme has grown consistently, peaking at 6.67 crore loans sanctioned in 2023-24 ( Rs 5.41 lakh crore) and maintaining strong numbers with Rs 5.65 lakh crore sanctioned by March 2026.

- Vision for 2047: The continued financial security and confidence instilled by these 57.79 crore loans align directly with the government's goal of achieving inclusive growth and transitioning India into a developed nation (Viksit Bharat) by 2047.

What are the Challenges Associated with the PMMY?

- Structural Asymmetry: Historically, over 70% of the loan volume has remained clustered in the 'Shishu' category.

- This indicates a failure to graduate micro-units into sustainable small and medium enterprises, perpetuating a "missing middle" in India's industrial landscape and stalling upward economic mobility.

- Credit-Absorption Capacity Deficit: The scheme heavily prioritizes capital infusion but overlooks the borrower's credit-absorption capacity.

- Without concurrent capacity building (financial literacy, business acumen, market access), borrowers often fail to deploy funds productively, leading to high micro-enterprise mortality rates.

- Sectoral Skewness and Low Value-Addition: MUDRA loans are predominantly concentrated in the trading and services sectors, with negligible penetration in manufacturing.

- This structural bias limits the employment multiplier effect and contributes minimally to Gross Fixed Capital Formation (GFCF).

- Rising Non-Performing Assets (NPAs): Due to the collateral-free nature of the loans and occasionally inadequate creditworthiness checks, NPAs and loan defaults remain a concern for public sector banks.

- Debt-Substitution vs. Asset Creation: A significant portion of the credit disbursed is utilized by beneficiaries to refinance existing, high-cost debt from informal moneylenders rather than for capital expenditure or creating new productive assets, thereby dampening the scheme's intended economic impact.

What Measures can Strengthen PMMY?

- Transition to Cash-Flow Based Lending: Banks must leverage India’s Digital Public Infrastructure (DPI), specifically the Account Aggregator (AA) framework and GST Network (GSTN), to shift from traditional, collateral-focused lending to dynamic, cash-flow-based credit assessment.

- This allows for real-time monitoring of business health and mitigates NPA risks.

- Adopting a 'Credit-Plus' Approach: Policy must pivot from mere "credit dispensation" to holistic "enterprise development."

- This requires institutional convergence between PMMY and platforms like ONDC (Open Network for Digital Commerce) and the Skill India Mission to provide borrowers with end-to-end handholding, from skill upgradation to market linkages.

- Granular End-Use Monitoring: Lending institutions should deploy data analytics and AI-driven Early Warning Signals (EWS) to track the end-use of disbursed funds.

- This will prevent the diversion of business loans toward personal consumption and identify financial stress before accounts turn into NPAs.

- Incentivizing Micro-Manufacturing: To align MUDRA with the broader goals of 'Make in India' and demographic dividend utilization, specialized incentives (such as enhanced interest subventions or priority guarantee coverage) should be introduced explicitly for micro-manufacturing units.

- Deepening NBFC and MFI Integration: Traditional commercial banks often lack the underwriting models for the informal sector.

- The scheme must further empower Non-Banking Financial Companies (NBFCs) and Micro Finance Institutions (MFIs), which possess superior "last-mile" connectivity and specialized expertise in grassroots credit appraisal.

Conclusion

PM MUDRA Yojana has expanded access to the unfunded sector, promoting enterprise, earning, and empowerment (3Es). Through a credit-plus approach and initiatives like Tarun Plus, it enables small units to grow and create jobs. Overall, it strengthens financial inclusion, inclusive growth, and the vision of Atmanirbhar Bharat.

|

Drishti Mains Question: Discuss the significance of the Pradhan Mantri MUDRA Yojana (PMMY) in driving financial inclusion and women empowerment in India. |

Frequently Asked Questions (FAQs).

1. What is Pradhan Mantri MUDRA Yojana (PMMY)?

It is a flagship scheme (2015) providing collateral-free loans to non-corporate, non-farm micro and small enterprises.

2. What are the loan categories under PMMY?

Shishu (up to ₹50,000), Kishor (₹50,000–₹5 lakh), Tarun (₹5–10 lakh), and Tarun Plus (₹10–20 lakh).

3. What is the role of MUDRA Ltd.?

It provides refinance support to lending institutions but does not lend directly to borrowers.

4. What is the significance of PMMY?

It promotes financial inclusion, women entrepreneurship (67% beneficiaries), and formalization of the informal sector.

5. What are the major challenges of PMMY?

Dominance of small loans, rising NPAs, low manufacturing share, and weak credit absorption capacity.

UPSC Civil Services Examination, Previous Year Question (PYQ)

Prelims

Q. Pradhan Mantri MUDRA Yojana is aimed at (2016)

(a) bringing the small entrepreneurs into formal financial system.

(b) providing loans to poor farmers for cultivating particular crops.

(c) providing pensions to old and destitute persons.

(d) funding the voluntary organizations involved in the promotion of skill development and employment generation.

Ans: (a)