Monetary Policy Report: RBI | 07 Aug 2020

Why in News

The Reserve Bank of India (RBI) has released the Monetary Policy Report for the month of August 2020.

- The Monetary Policy Report is published by the Monetary Policy Committee (MPC) of RBI.

- The MPC is a statutory and institutionalized framework under the RBI Act, 1934, for maintaining price stability, while keeping in mind the objective of growth.

- The MPC determines the policy interest rate (repo rate) required to achieve the inflation target (4%).

- The Governor of RBI is ex-officio Chairman of the MPC.

Key Points

- Policy Rates Unchanged:

- Repo rate remains at 4% and the reverse repo rate at 3.35%.

- Repo rate is the rate at which RBI lends money to commercial banks.

- Reverse repo rate is the rate at which the RBI borrows money from commercial banks within the country.

- RBI has kept the policy rates unchanged because of rising retail inflation levels.

- Retail inflation (measured by the Consumer Price Index - CPI) rose to 6.09% in June 2020 from 5.84% in March, breaching the central bank’s medium-term target of 4±2%.

- This inflation range (4% within a band of +/- 2%) was recommended by the committee headed by Urjit Patel in 2014.

- Repo rate remains at 4% and the reverse repo rate at 3.35%.

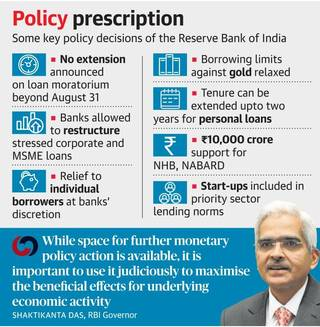

- Loan Restructuring:

- RBI has allowed banks to restructure loans to reduce the rising stress on incomes and balance sheets of large corporates, Micro, Small and Medium Enterprises (MSMEs) as well as individuals.

- A large number of firms that otherwise maintain a good track record are facing the challenge as their debt burden is becoming disproportionate, relative to their cash flow generation abilities.

- This can potentially impact their long-term viability and pose significant financial stability risks if it becomes widespread. It may also lead to an increase in Non-Performing Assets.

- However, only those borrowers will be eligible for restructuring whose accounts were classified as standard and not in default for more than 30 days with any lending institution as on 1st March, 2020.

- All other accounts will be considered for restructuring under the Prudential Framework issued by the RBI in 2019, or the relevant instructions as applicable to specific categories of lending institutions where the prudential framework is not applicable.

- The restructuring efforts may or may not include a moratorium on instalment repayments. RBI has left the decision of moratorium on banks, with an eye on averting such loans from slipping into non-performing assets.

- The loan restructuring scheme will be worked out by a committee headed by KV Kamath (former ICICI Bank Chairman).

- RBI has allowed banks to restructure loans to reduce the rising stress on incomes and balance sheets of large corporates, Micro, Small and Medium Enterprises (MSMEs) as well as individuals.

- Liquidity Support:

- An additional special liquidity facility of Rs.10,000 crore, equally to be split between National Bank for Agriculture and Rural Development (NABARD) and the National Housing Bank (NHB) to help small financiers and home loan companies amid Covid-19 difficulties.

- It can be noted that higher share of moratoriums are being availed by the retail borrowers which has created the need for such liquidity support to lenders.

- The liquidity facility to both NABARD and NHB will be offered at the policy repo rate.

- An additional special liquidity facility of Rs.10,000 crore, equally to be split between National Bank for Agriculture and Rural Development (NABARD) and the National Housing Bank (NHB) to help small financiers and home loan companies amid Covid-19 difficulties.

- Growth Projection:

- Economic activity had started to recover from the lows of April-May 2020 following the uneven reopening of some parts of the country in June 2020.

- However, fresh Covid-19 infections have forced renewed lockdowns in several cities and states, and economic indicators have levelled off.

- The recovery in the rural economy is expected to be robust, buoyed by the progress in kharif sowing.

- Manufacturing firms responding to the RBI’s industrial outlook survey expect domestic demand to recover gradually from the second quarter of 2020-21 and sustain through the first quarter of 2021-22.

- For 2020-21 as a whole, real Gross Domestic Product (GDP) growth is expected to be negative. Early containment of the pandemic may improve the outlook.

Link between Growth, Inflation and Interest rates

- In a fast-growing economy, incomes go up quickly and more and more people have the money to buy the existing bunch of goods.

- As more and more money chases the existing set of goods, prices of such goods rise. In other words, inflation (which is nothing but the rate of increase in prices) increases.

- To contain inflation, a country’s central bank typically increases the interest rates in the economy. By doing so, it incentivises people to spend less and save more because saving becomes more profitable as interest rates go up.

- However, when growth contracts, people’s incomes hit. As a result, less and less money is chasing the same quantity of goods. This results in either the inflation rate decelerating or it actually contracts (also called deflation).

- In such situations, a central bank decreases interest rates so as to incentivise spending and by that route boost economic activity in the economy.

- In the current Monetary Policy, RBI has not raised the interest rates even when retail inflation is high because RBI is facing an odd situation at present: GDP is contracting even as inflation is rising.

- This is happening because the pandemic has reduced demand, on the one hand, and disrupted supply on the other. As a result falling growth and rising inflation are happening at the same time.